India is now the fifth most digitalised country in the world

FinTech BizNews Service

Mumbai, 8 June 2026: Indian Council for Research on International Economic Relations (ICRIER) and ICRIER-Prosus Centre for Internet and Digital Economy (IPCIDE) has come out with very useful research report titled “State of India’s Digital Economy”, authored by Deepak Mishra, Aarti Reddy, Shailly Gupta, and Agrima Khanduri:

Global benchmarking has become a weapon in the AI race

As digitalisation and AI become strategically important, cross-country benchmarking of the digital economy is no longer a purely academic exercise. It is increasingly becoming a tool in the global AI race, where rankings are closely watched, fiercely debated, and frequently challenged. This is why we launched the State of India’s Digital Economy (SIDE) report— an annual publication since 2023—to bring greater clarity, transparency, and methodological rigour to the digital benchmarking landscape.

This edition of SIDE introduces two major improvements. First, it embeds AI-related indicators into the CHIPS—Connect, Harness, Innovate, Protect, and Sustain—framework, thereby updating it for the AI era. Second, we expand the country coverage from 32 to 71 countries, accounting for 96 percent of global GDP, 86 percent of the world’s internet users, and 83 percent of the global population.

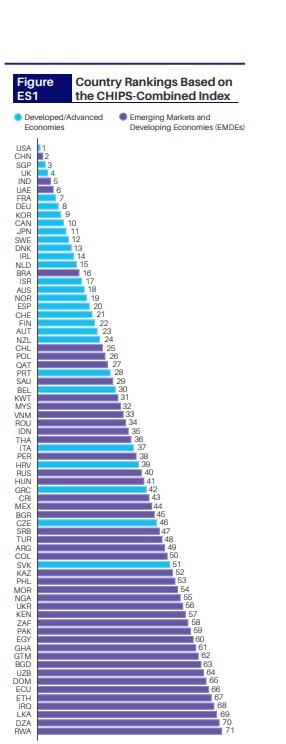

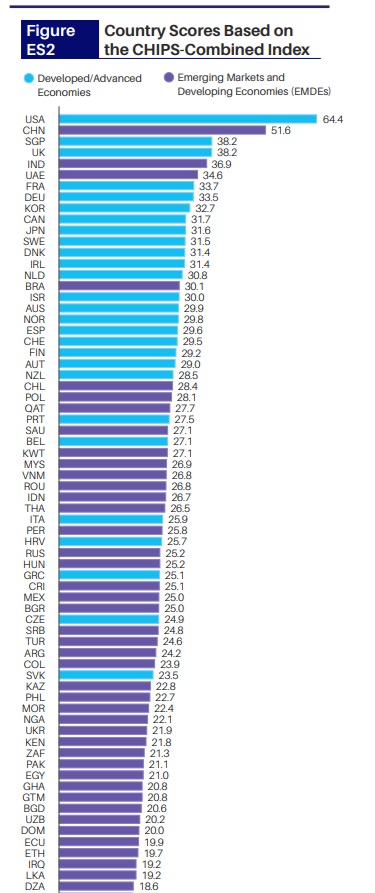

India is now the fifth most digitalised country in the world

The global digital map is becoming more distributed and tripolar. Digital leadership was historically concentrated in North America and Western Europe, with Japan as the Asian outpost. That order is changing. The rise of the digital economy in China, India, Singapore, South Korea, and other Asian economies is shifting the centre of gravity toward the Indo-Pacific. Among the top five digitalised countries, three—China, Singapore, and India—are from the Indo-Pacific, while the U.S. and the U.K. represent the North Atlantic. Continental Europe remains relevant, with France and Germany in the top 10, but its relative influence appears to be declining. The U.S. remains the clear digital frontrunner. With a score of 64.4, it is well ahead of China, which ranks second with 51.6. China is now the most connected country in the world and performs strongly on the Harness and Innovate pillars. India’s rank has improved from eighth place in 2025 to fifth place in 2026. This reflects both real gains—especially improved connectivity, greater harnessing of digital technologies, and a strong AI talent pool—and some methodological changes, including the expanded sample and the exclusion of some indicators where India performed less well. Even with these caveats, it is clear that India belongs in the top decile of global digital rankings. At the same time, digital convergence remains limited. While most countries are making progress, the U.S. continues to push the frontier further ahead. The gap between the frontier and many other G20 economies has widened, and country rankings have become more entrenched. Regional spillovers also appear weak. Countries in the same region often show very different levels of digitalisation, suggesting that digital transformation is driven less by geographical proximity—unlike manufacturing—and more by domestic capabilities, institutions, policies, and private sector dynamism. While digitalisation is spreading rapidly, the production of digital goods and services is becoming increasingly concentrated. Access to digital technologies is spreading much faster than income. Users of internet, smartphone, e-commerce, and AI are distributed far more broadly than GDP. Developing countries now account for the majority of users across most digital technologies. Yet frontier technology production— advanced chips, cloud infrastructure, large language models, AI compute, and digital platforms—remains concentrated in a handful of countries and firms.

Developing countries are doing better on AI diffusion than on traditional digitalisation

Generative AI is now the fastest-diffusing digital technology in history. It reached mass adoption far faster than the internet, smartphones, e-commerce, or digital payments. Unlike earlier technology waves, AI has become a developing-country phenomenon almost immediately. Developing countries account for 72 percent of global AI users, with China and India alone accounting for nearly two-fifths of global users. This creates a major opportunity for developing countries to shape AI adoption and use cases. India performs especially well on AI. In the standalone AI index, India ranks fourth, behind only the United States, China, and Singapore, and ahead of Germany, France, Japan, Canada, and Korea. We find that developing countries are, on average, doing better on AI adoption than on traditional digitalisation. However, this finding should be treated with caution, as many AI indicators capture inputs and intermediate capabilities—such as publications, patents, skills, GitHub activity, model development, and startup funding—rather than economy-wide outcomes such as productivity, exports, investment, or growth. India’s AI opportunity lies not in replicating the capital-heavy strategies of the U.S. or China, but in building a talent-led, application-driven AI ecosystem. India has the second-largest concentration of AI talent after the U.S., but lacks comparable levels of patient capital and compute capacity. The next wave of AI—driven by applications, agents, and widespread use—should play to India’s strengths. But talent alone will not be enough. India will need more risk capital, affordable compute, stronger links between universities and startups, shared datasets, testing sandboxes and clearer pathways for commercialisation.

The hidden costs of digitalisation are large and largely ignored

Digital progress has brought growth, jobs, and better service delivery, but it has also created risks: global imbalances in digital trade, rising digital crime, and growing e-waste. Most digital consumers now live in Emerging Markets and Developing Economies (EMDEs), but digitally delivered trade remains dominated by advanced economies. India is a major exception. With around USD 328 billion in digitally delivered trade, it has become a globally significant exporter of digital services despite being a lower-middle-income country. Cyber risks are rising with digital scale. The U.S. accounts for almost as many reported enterprise ransomware victims as the rest of the world combined. High-income and highly connected economies are especially exposed to ransomware and email leaks. Developing countries are learning that rapid digitalisation without adequate cybersecurity can be costly. India is already among the larger cybersecurity markets, but its spending remains modest relative to the size of its digital economy and user base. Finally, digitalisation has come with considerable sustainability costs. E-waste per person is rising with income, though India’s per capita e-waste remains low. The policy lesson that emerges is that developing countries should not follow the environmentally damaging path taken by advanced economies. They should build e-waste systems early, strengthen producer responsibility, integrate informal recyclers, promote repair and reuse, and recover critical minerals from discarded electronics.