Gold loans are a small portion of overall loans

FinTech BizNews Service

Mumbai, March 23, 2026: Kotak Institutional Equities has scome out with the latest Strategy Note on Gold, authored by Sanjeev Prasad, MD & Co-Head.

India’s ‘Midas’ touch

The steep increase in the value of stock of gold with Indian households on the back of a sharp increase in prices of gold should theoretically hold several positives for India—(1) higher household wealth, (2) stronger household sentiment and (3) potential higher spending. However, this ‘Midas’ touch comes with several downsides, which are underappreciated by the market.

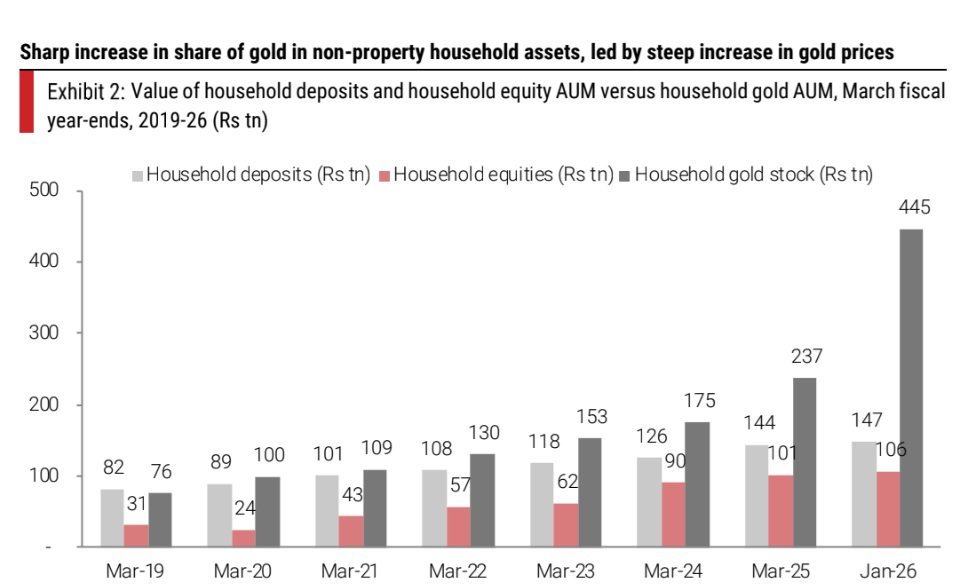

Steep increase in value of stock of gold with households

The value of the stock of gold with Indian households stands at a whopping US$5 tn (125% of GDP) and has gone up sharply in the past few months on the back of a sharp increase in gold prices. The growth in value of household gold stock was a lot more moderate in the previous decade. The value of stock of gold with households is now a sizable 65% of the non-property stock of wealth with Indian households.

Any change in household consumption behavior?

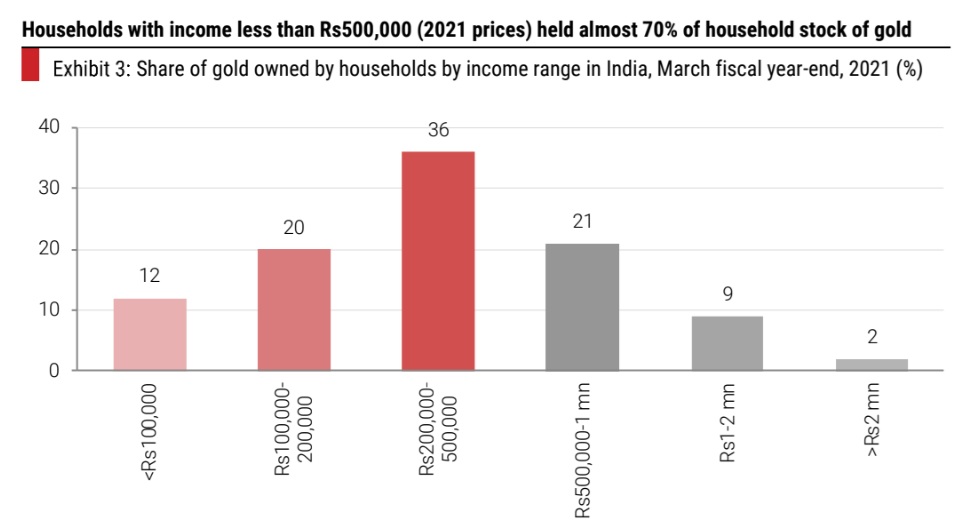

We would assume a moderate positive impact of the sharp increase in the wealth of households on domestic consumption even though there has been no correlation historically between (1) gold prices and (2) domestic consumption. We would note that household gold stock is held by a large number of households with a disproportionate share of holdings by low-income households. We would assume that the consumption behavior of low-income and high-income households will not change much with the change in gold prices. Low-income households may not have adequate financial security to change their saving and spending behavior.

Micro-economic benefits limited to gold loans

The nature of gold and its triple role of (1) store of value, (2) store of wealth (unaccounted for also) and (3) jewelry for Indian households severely restricts its usage as a productive asset. Loans against gold seem to be the only way to use gold in a productive manner. However, gold loans are a small portion of overall loans (a breakdown of loans of both banks and NBFCs) and retail loans despite the sharp increase in gold loan AUM over the past few years. We doubt the government can implement an amnesty scheme to ‘recycle’ household gold in order to reduce gold imports.

Macro-economic downsides of the ‘Midas’ touch

We note that households’ gold purchases represent a conversion of financial savings (bank deposits) into physical assets. This is tantamount to exports of household capital. Other external sector flows remaining constant, this implies a drawdown of RBI FX reserves, mirrored in lower net foreign currency assets on RBI’s balance sheet. By construction, this curtails reserve money creation (and system liquidity), weighing on deposit growth unless offset by RBI’s durable liquidity injections. Net gold and precious stone imports at US$500 bn dwarf FPI debt and equity net flows of US$200 bn and almost match FPI and FDI flows of US$600 bn over FY2011-10MFY26.

Quick Numbers

We estimate value of stock of gold with Indian

households at almost US$5 tn

We estimate value of stock of gold with Indian

households at 175% of value of deposits and equity

with Indian households as of January 2026

Gold loans AUM at Rs12 tn at end-FY2025 (around

5.5% of total loans and 12% of total retail loans)

Net purchase of gold and precious stones at 2.5X FPI

debt and equity flows and 85% of all foreign inflows

over FY2011-10MFY26