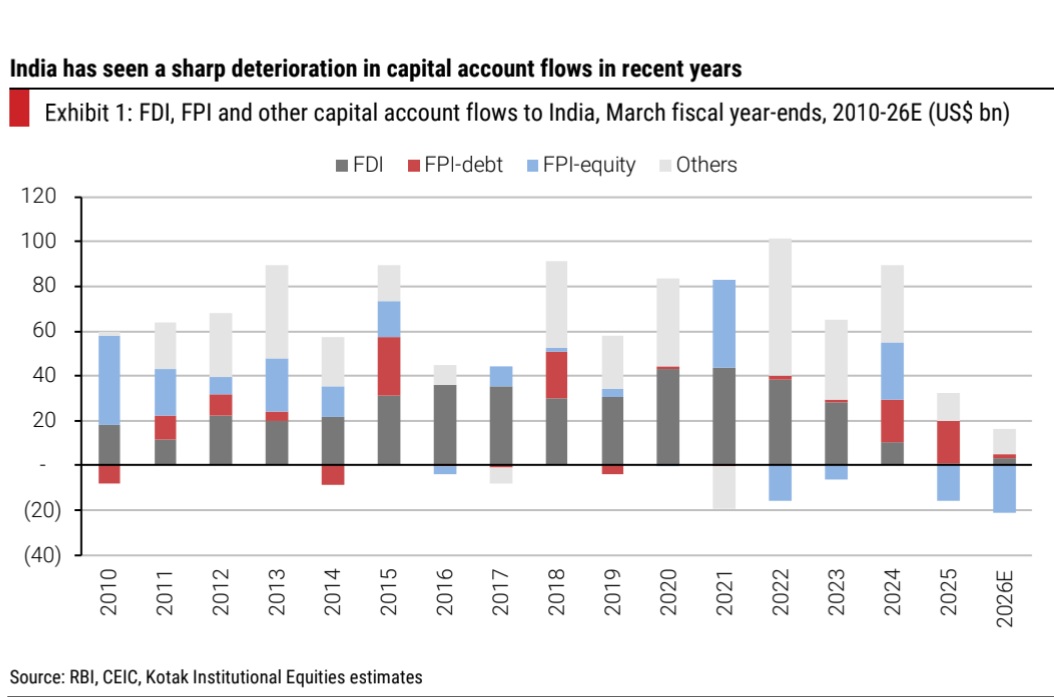

India’s CAD may weaken further in FY2027, given high crude oil prices, which will exert further pressure on India’s overall BoP. India has seen a sharp deterioration in capital account flows in recent years

FinTech BizNews Service

Mumbai, 26 May 2026: Kotak Institutional Equities has come out with a research report, authored by Sanjeev Prasad, MD & Co-Head.

India’s ‘capital’ problem

India’s external capital dependency has become more visible over the past two years with (1) a sharp slowdown in net FDI flows and an increase in FPI outflows coinciding with (2) higher CAD on high global energy prices. Large capital inflows until FY2024 offset India’s high structural trade and current account deficits. This vulnerability may persist without a structural fix to high CAD.

Lower capital inflows and weaker CAD

The persistent weakening in net FDI inflows since FY2021 and large FPI outflows over FY2025-26 have reduced capital account buffers to India’s extant structural trade deficits (see Exhibits 1-2). India’s CAD may weaken further in FY2027, given high crude oil prices, which will exert further pressure on India’s overall BoP. A combination of high current deficits but large capital surpluses sustained India’s BoP until FY2024. However, the rising cost of servicing the growing stock of external capital (see Exhibit 3) has also added to the CAD and BoP challenges.

Gross FDI outflows from foreign and Indian entities may sustain

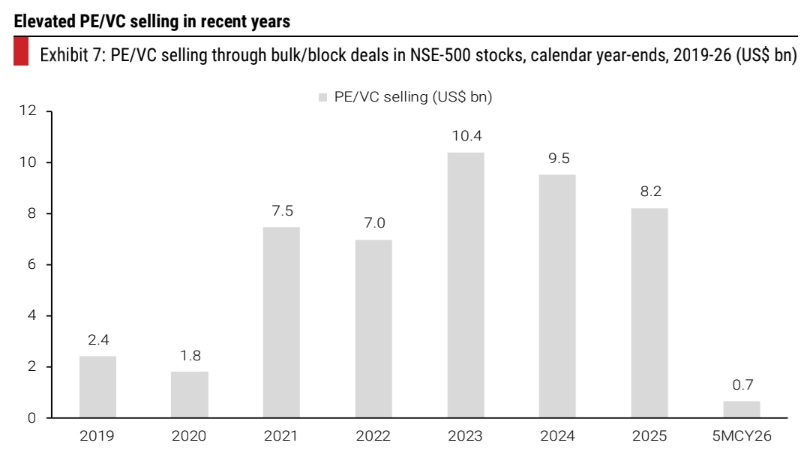

Our analysis on FDI flows shows that the weakness in net FDI flows is driven by a steady increase in gross FDI outflows of foreign (from US$27 bn in FY2021 to US$45 bn in 9MFY26) and Indian (from US$15 bn in FY2021 to US$28 bn in 9MFY26) entities. Gross FDI inflows from overseas entities have sustained, but they have been nullified by large outflows from PE/VC investors (exits from their extant holdings in India) and MNCs (OFS of stakes in their Indian subsidiaries in the primary and secondary markets). Indian companies may continue to pursue outward investments, given their strategic imperatives—(1) ambitions of geographical expansion and (2) compulsions of technology acquisition.

FPI flows may stay muted

We expect gross FDI outflows of foreign entities to stay at elevated levels, given the large holding of PEs and VCs in several large Indian listed and unlisted companies. PE/VC investors currently hold US$32 bn at current valuations in large listed entities (see Exhibit 6) and even more in unlisted entities. We note that the bulk of gross FDI outflows of overseas entities over the past few years is due to (1) selling by PE/VC investors and (2) listing by MNCs of their subsidiaries in India (large OFS share in primary issue amount).

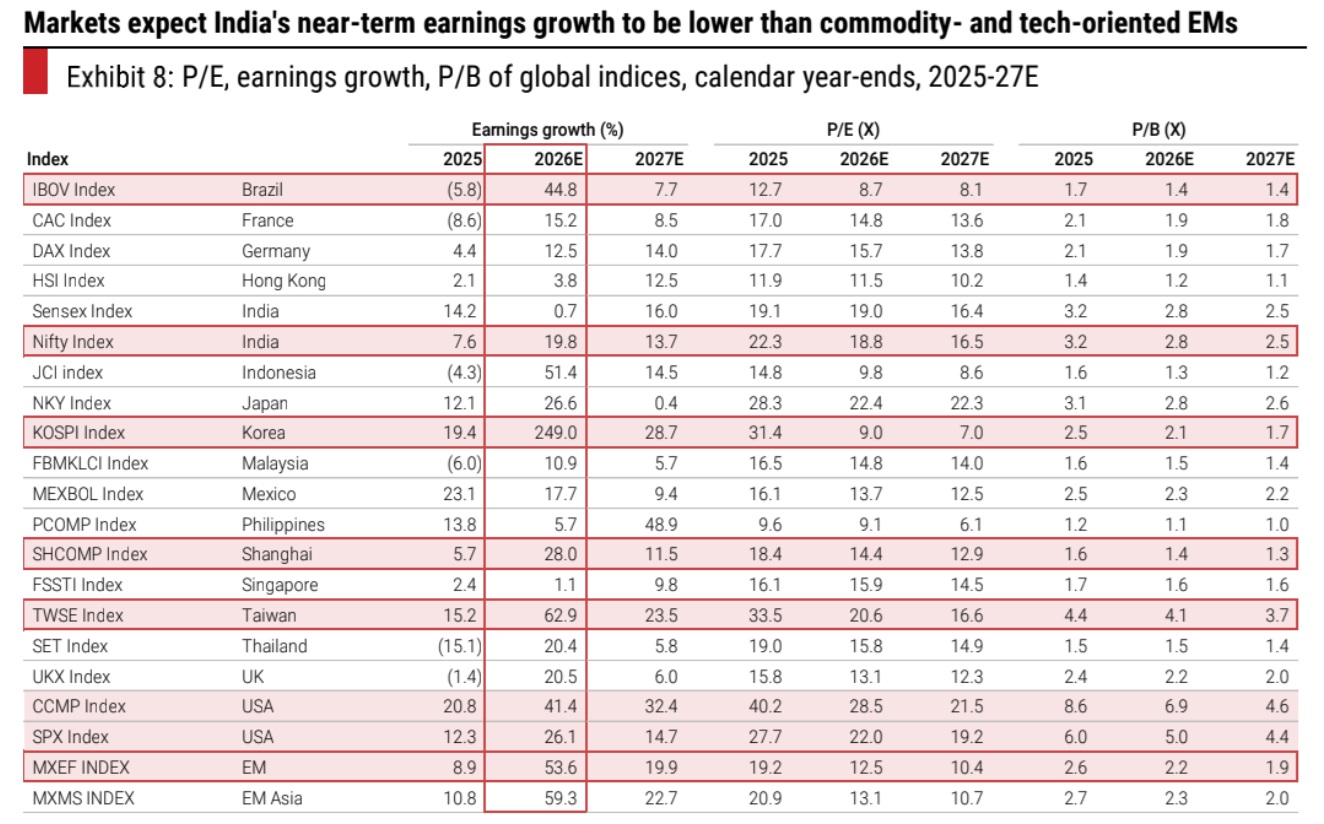

We expect FPI flows to stay muted, given India’s low attractiveness versus other EM markets due to (1) weaker relative FY2027E earnings growth in terms of quality and quantity, (2) ‘negative’ exposure to the ongoing AI and semiconductor cycle that may continue for another 1-3 years and (3) ‘negative’ exposure to commodities, especially crude oil and natural gas. Other EM markets offer high exposure to the AI and commodity cycles. The continued large FPI outflows from Indian equity markets reflect the steady deterioration of relative returns amid continued compression of relative earnings growth expectations.