Defence, infrastructure and healthcare sectors should continue to see improvement in credit profiles.

FinTech BizNews Service

Mumbai, April 1, 2026: The Crisil Ratings credit ratio, or the proportion of rating upgrades to downgrades, stood at 1.50 times in the second half of fiscal 2026, moderating from 2.17 times in the first half.

Overall, there were 383 upgrades and 255 downgrades during the period (see the chart in annexure).

The reaffirmation rate was ~82%, compared with ~80% in the previous half, underscoring the resilience of companies.

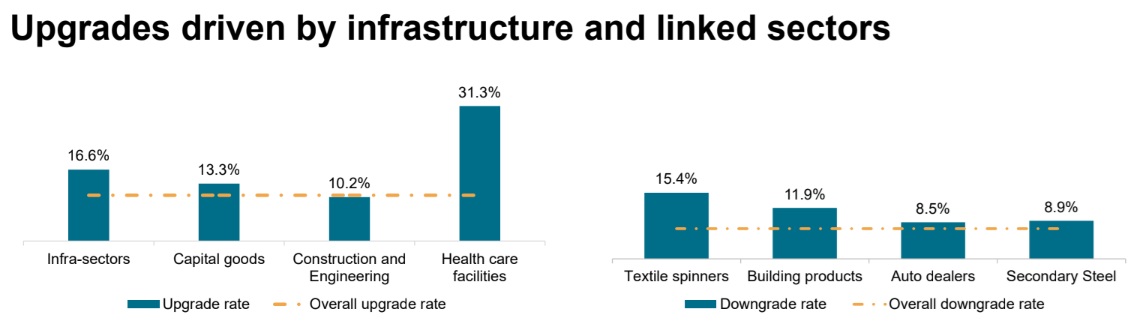

The upgrade rate declined to ~10.6% (14.0% in the previous half), aligning with the 11% average of the past decade. Infrastructure and related sectors—construction and engineering, roads, renewables, capital goods—and healthcare were at the forefront of upgrades.

The downgrade rate edged up to 7.0% (6.4% in the first half), a tad higher than 10-year average. Consequently, the credit ratio moderated, with the overhang of tariff-related uncertainties impacting companies with greater dependence on exports.

India Inc is expected to benefit from tailwinds from goods and services tax rationalisation and some lag effect of income tax cuts announced last year, infrastructure capital expenditure spends of the government and reversal of the US reciprocal tariffs. Defence, infrastructure and healthcare sectors should continue to see improvement in credit profiles.

The West Asia conflict, however, would increase cost pressures and necessitate realignment of supply chains for India Inc. Amid this, India Inc's credit quality outlook for fiscal 2027 is stable but cautious.

Crisil Ratings conducted a stress test of 30 sectors exposed to the West Asia conflict either directly or indirectly. These account for 65% of our rated corporate debt.

Says Subodh Rai, Managing Director, Crisil Ratings, "Our assessment indicates 23 of these 30 sectors will see limited impact on credit profiles because of the conflict, despite higher input prices and disruption in gas supply. Clearly, strong balance sheets (median debt-to-equity ratio of 0.45 time as on March 31, 2026) lends cushion. The impact could be moderately negative for six sectors and adversely affect one. A prolonged conflict would, however, be a systemic risk and could have a cascading impact on India Inc's credit quality.”

While it is not possible to predict with precision when the conflict will end and when crude oil and gas supplies will return to normalcy, our stress test is based on the following key assumptions for fiscal 2027:

• Conflict-related fuel disruption and stabilisation period lasts for a total 4–5 months (starting from February 28, 2026, and 3–4 months in fiscal 2027)

• Crude oil prices at $100 per barrel in the first quarter and averaging $85–90 for the full fiscal

• First-order impact will be from the gas supply shock, crude-oil linked price increases, direct trade exposure and foreign currency exposure. Second-order impact due to inflationary pressures affecting discretionary demand in some pockets is also considered

Based on these assumptions, we assessed the impact of the conflict on sectoral revenue and operating margin. We have further evaluated whether balance sheet strength can offset the impact. We have not considered further policy or regulatory support measures. The results are as follows:

• Only one of the 30 sectors assessed is expected to see an adverse impact.

• Six sectors could see moderately negative impact on their credit quality mainly because of impact on operating margin

• The remaining 23 sectors would see limited impact on their credit quality on account of:

• No major impact of foreign currency depreciation: Our analysis shows companies either have a natural hedge through trade or have forward cover on their forex exposure. The share of foreign currency debt in corporate debt is also low.

If the conflict is prolonged, some sectors considered resilient earlier may see vulnerabilities emerge. These vulnerabilities would be more prominent in sectors where the demand is discretionary or dependent on global demand drivers1.

Bank credit growth in fiscal 2027 is expected at 13%, tad lower than fiscal 2026, which is in line with the economic growth. Credit growth will still be reasonable, driven by the micro, small and medium enterprises (MSME) and retail sectors, and continued substitution of corporate bonds with bank loans because of relatively lower interest rates. The West Asia conflict could drive up India Inc’s working capital debt in the short term even as private sector capex may see some lag. Sustained deposit growth will be crucial as the gap with credit growth has widened. Gross non-performing assets are expected to remain range bound.

Non-banks will see assets under management continue to grow at a steady 18–19% in fiscal 2027, driven by consumption demand and supportive policy measures. The unsecured business loan and micro loan against property segments have seen an uptick in delinquencies and will remain under watch. The impact of stock market decline on asset quality of personal loans, especially of leveraged retail investors, would bear watching. Asset quality of microfinance loans is expected to stabilise, but the impact of policy measures in a few states—such as loan waivers and stricter loan recovery measures— will need to be monitored. Balance sheets remain healthy.

For both banks and NBFCs, however, the impact of the West Asia conflict on MSMEs, with exposure to the region as well as on those dependent on gas supplies and crude, will bear watching.

Says Somasekhar Vemuri, Senior Director, Crisil Ratings, “Corporate India’s agility and resilience are being tested again after the Covid-19 pandemic and the tariff tantrums. Our credit quality outlook is stable for now, backed by resilient domestic demand and strong corporate balance sheets. But overall, we remain cautious as the duration and intensity of the West Asia conflict is uncertain. If it prolongs, slower global growth, gas availability challenges, higher-for-longer crude oil prices and consequently impact on consumer sentiment will bear watching. The government and regulators may have to step up relief and supportive measures, as seen in the past. The extent of these can also have a bearing on the credit quality outlook.”