A gradual weakening in the DIY-investing trend seen over FY2021-25

FinTech BizNews Service

Mumbai, April 20, 2026: The latest report of Kotak Institutional Equities, authored by Sanjeev Prasad, MD & Co-Head, note that FII outflows were quite high in India and the performance of India was weaker compared to other EMs such as South Korea and Taiwan in this period, resulting in the latter two markets seeing further increases in their weights at the expense of India.

Game of patience

Indian retail investors have continued with their systematic investments and added lump-sum investments to their mutual fund investments during market dips despite weak trailing returns. Returns have been quite abysmal for two years now. The conviction levels of new and old retail investors may get tested further if trailing returns were to stay muted.

Quick Numbers

Rs1.1 tn of equity inflows into active equity mutual funds in India 1QCY26 versus Rs4.5 tn in CY2025 and

Rs4.1 tn in CY2024

7% decline in the number of active clients of Indian brokerages in FY2026

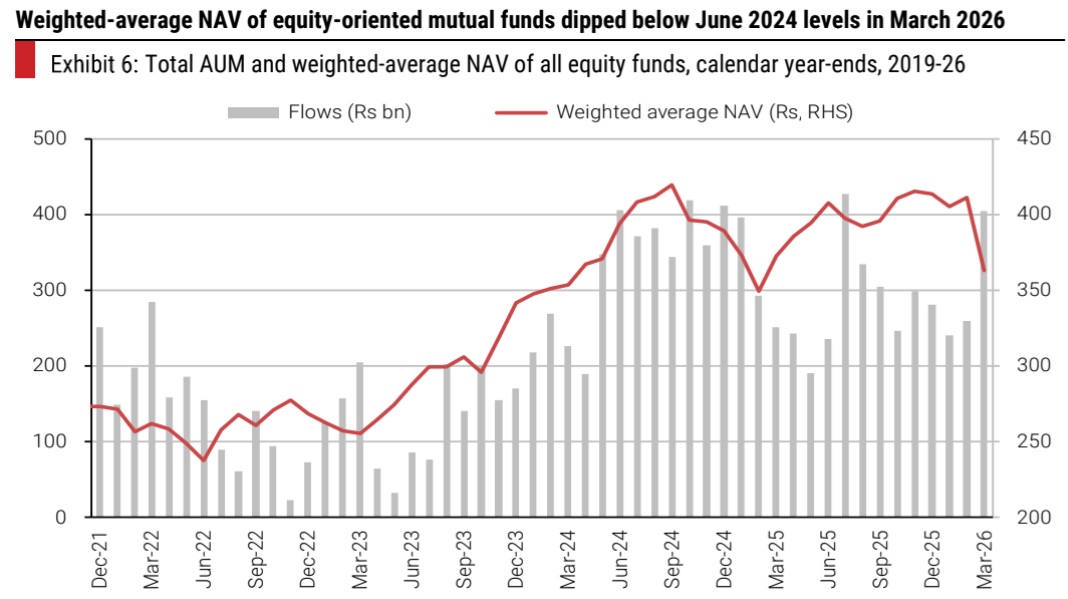

Weighted-average NAV of equity mutual funds down 14% from peak levels of September 2024

Retail investors reposed faith in MFs but wavered in direct investments

The sharp volatility and correction in broader markets in March 2026 notwithstanding, retail investors continued their mutual fund investments through SIPs and higher lump sums. We note that most fund types witnessed an increase in retail flows in March 2026, even as the allocation toward (1) passive funds, (2) multi-asset funds and (3) flexi-cap. funds saw a sharp increase in 1QCY26. At the same time, the active retail investor base shrank in FY2026, suggesting a gradual weakening in the DIY-investing trend seen over FY2021-25.

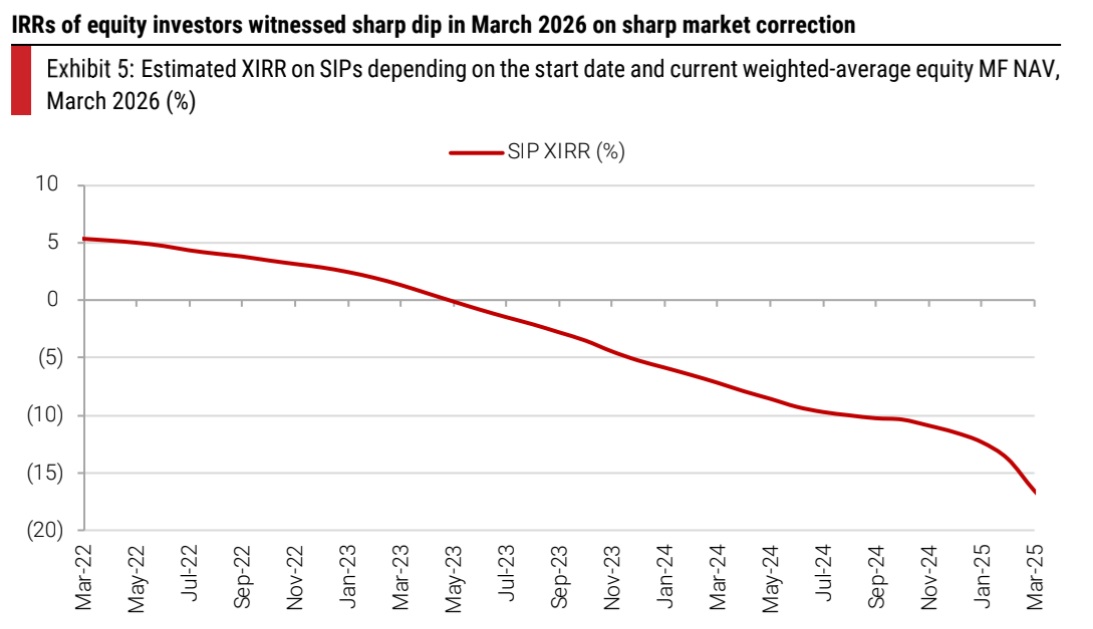

Sharp dip in markets resulted in negative IRRs on mutual fund investments

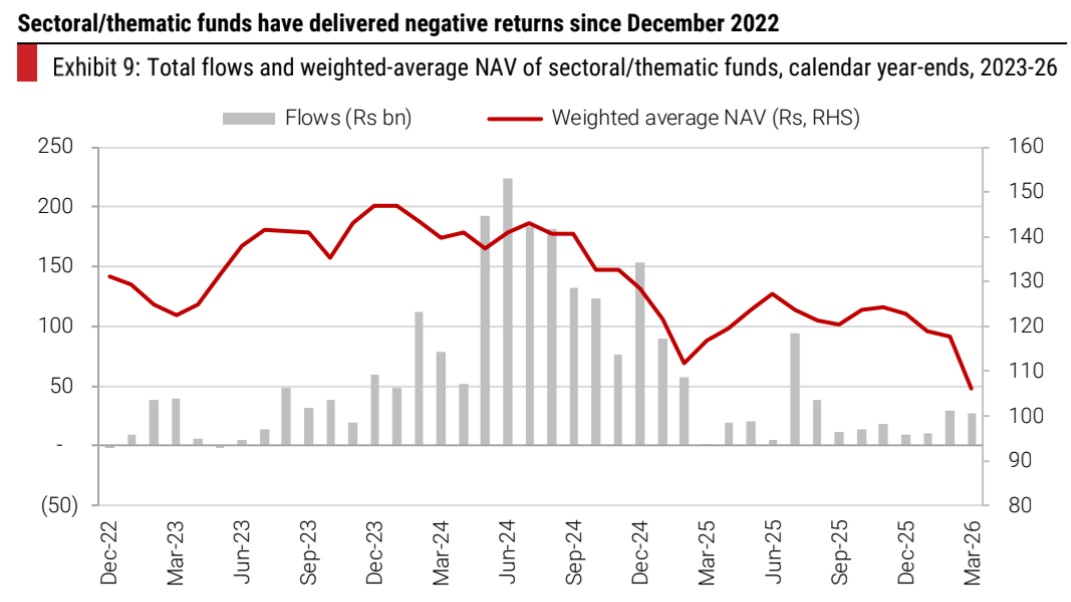

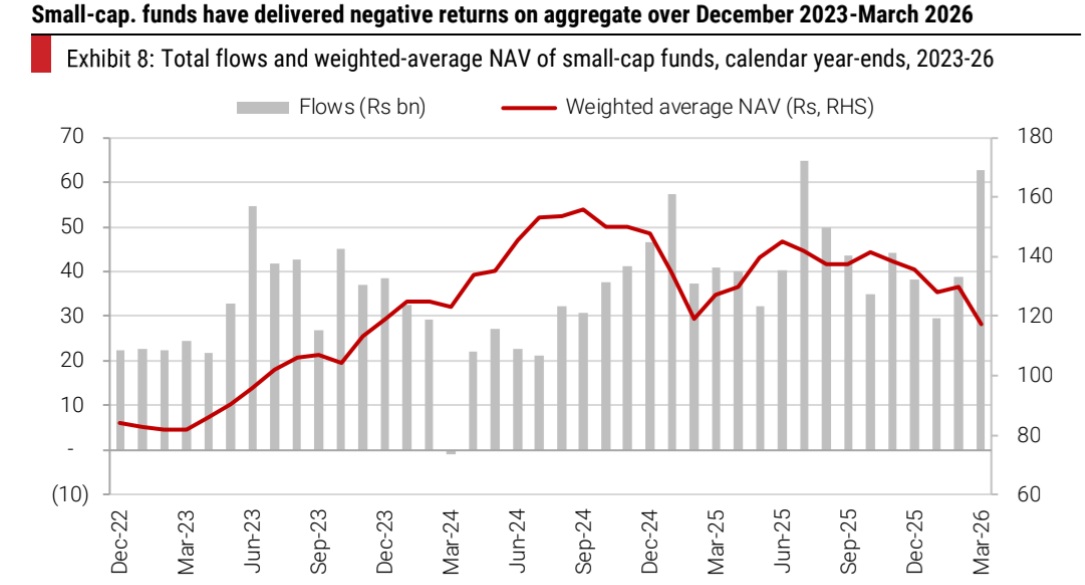

Our analysis of weighted-average NAVs of equity-oriented MFs shows that retail investors have made poor returns over July 2024-March 2026, even as the total flows in this period are 58% of the total flows mobilized by MFs in CY2022-26. The small-cap. and thematic funds have performed far worse than the overall equity funds in the past 21 months, while they captured a decent portion of the flows in this period.

Both active and passive FPIs sold India in the past 45 days

Indian equity markets witnessed relentless FPI outflows in the past 45 days, with (1) US$14.2 bn sold during the market correction over February 28 and March 30 and (2) US$3 bn sold during the market recovery from March 31 till date. We note that (1) FII outflows were quite high in India and (2) the performance of India was weaker compared to other EMs such as South Korea and Taiwan in this period, resulting in the latter two markets seeing further increases in their weights at the expense of India. In addition, passive flows remained weaker for India, relative to South Korea and Taiwan, in recent weeks, similar to the trend seen in the pre-war period.

Higher active and passive flows supported cash levels of mutual funds

Continued FII selling, both during the sell-off as well as bounce-back phases of the Indian market over the past 45 days, was largely ‘absorbed’ by domestic MFs, driven by (1) strong active and passive inflows (including EPFO allocation to equities) and (2) modest decline in cash levels. We note that balanced funds and multi-asset funds have not materially increased their weight in equities in March 2026. FPIs may continue to keep a nuanced stance towards India until India’s earnings outlook and valuations versus other major EMs improve materially. Cash levels of MFs have come off, resulting in lower buffers against continued FPI selling.