The capital market players exposed to market volatility (brokers and exchanges) will outperform companies exposed to market levels (AMCs, wealth and RTAs)

FinTech BizNews Service

Mumbai, April 8, 2026: The latest Kotak Institutional Equities report on Capital Markets provide useful info about the capital market players:

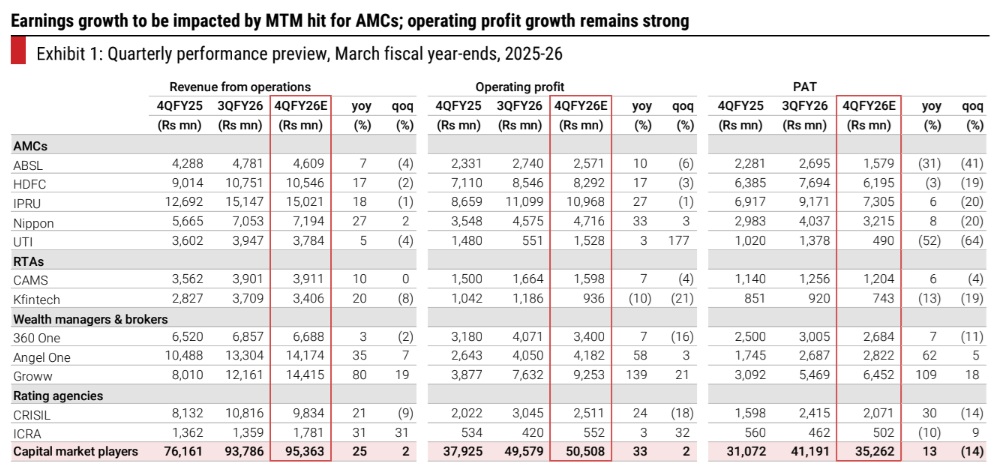

4QFY26 Preview: Activity over assets

We believe that capital market players exposed to market volatility (brokers and exchanges) will outperform companies exposed to market levels (AMCs, wealth and RTAs). MTM pressure should lead to weaker reported profitability across AMCs despite stable retail flows, with relatively better AUM growth at IPRU, Nippon and HDFC. CAMS should outperform Kfin on most metrics. 360 One will likely report sequentially weaker results due to MTM and lower transaction income, while brokers benefit from strong retail activity. Groww is likely to report the strongest quarter among companies under coverage.

AMCs and RTAs: MTM takes a toll

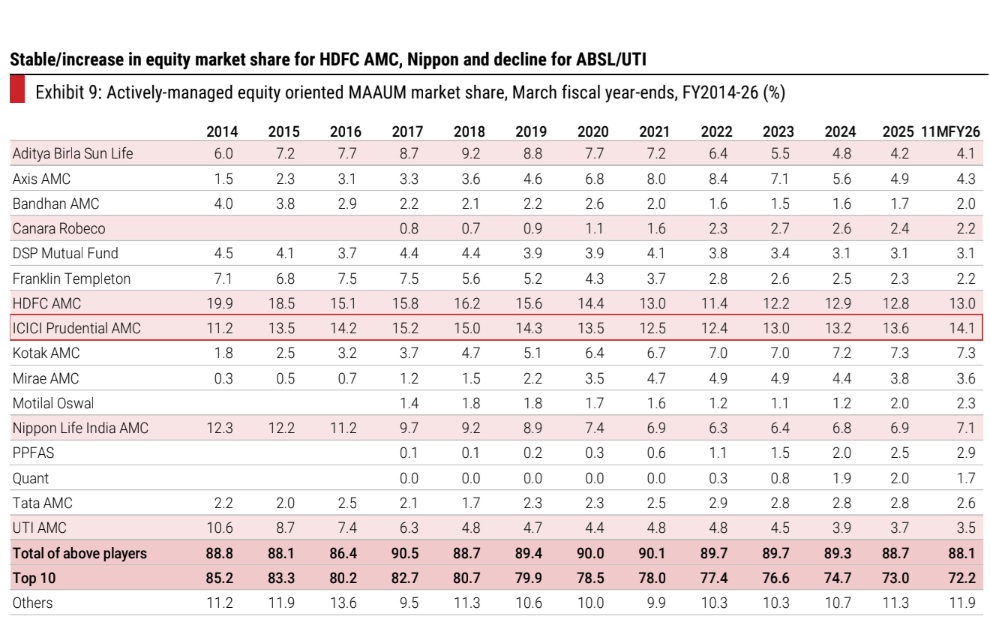

AMCs: 4QFY26 saw about 3% decline on average in Nifty-500 and about 14% decline on a period-end basis. Reported net inflows in Jan-Feb and estimated flows in March suggest stable trends in retail flows in active equity funds. AMCs have already reported quarterly average AUM: we see relatively stronger AUM growth for IPRU, Nippon and HDFC, followed by ABSL and UTI (Exhibit 2). The sharp qoq decline in PAT reflects the MTM impact on the investment book (10-15% of the investment book is in equity funds). Core earnings growth is likely to be marginally lower for most of the AMCs, barring Nippon and UTI (one-offs in the base quarter).

RTAs: Among RTAs, we expect CAMS to report marginally better AUM growth compared to Kfin. Kfin’s financial performance is likely to be weaker due to (1) yield decline due to the mix effect (ETF AUM growth) and (2) issuer solutions impacted by weak growth in retail folios and one-offs. More broadly, CAMS is benefiting from larger clients growing faster while Kfin is delivering healthy growth in the international business.

Wealth managers and brokers: Groww to outshine

360 One: We expect 360 One to report sequentially weak results, as we build in lower transactional revenues, along with MTM impact in other income. Recurring revenues, yields and net new money trends are likely to be relatively stable (although net new money to be lower versus the higher base of 3Q).

Brokers: We expect Angel One and Groww to benefit from stronger retail activity levels, especially volumes in index options and commodities. MTF growth is likely to be relatively subdued due to the market fall. We expect stronger margin uplift in Groww as compared to Angel One. Within coverage, Groww stands out with the strongest performance during the quarter.

Rating agencies: Decent revenue trends, helped by inorganic growth

We expect 15-16% yoy growth in rating revenues for CRISIL and ICRA, likely supported by better growth trends in bank credit. Bond issuances have been weak yoy (-10%) while up qoq (10%). Non-ratings business is always harder to forecast, but recent M&As will help report stronger revenue growth.