Policy and market structures must evolve to accelerate financial formalisation, deepen credit and improve rate transmission to support India’s US$30–35 trillion economy ambition

FinTech BizNews Service

Mumbai, 18 June 2026: India’s financial services sector is entering a defining transition phase, moving from rapid expansion in access and digital adoption to the need for deeper credit penetration, stronger financial participation and more efficient capital allocation. As India works towards becoming a US$30–35 trillion economy by 2047, the sector will need to move decisively beyond legacy policy frameworks, market infrastructure, technology and customer experience standards.

According to Deloitte India’s State of Financial Services in India (SOFSI) report, the sector has scaled significantly over the past two decades. Its market capitalisation rose from about 6 percent of GDP in 2005 to nearly 27 percent in 2025, while the share of NBFCs, insurers, asset managers and other non-bank participants increased from 15 percent to 43 percent. This has been a structural, not simply a cyclical, recovery.

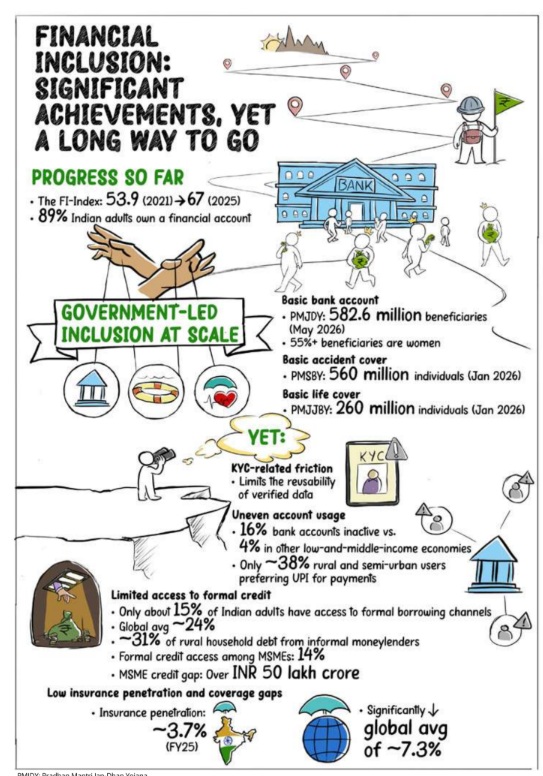

However, this expansion is yet to translate fully into deeper financial participation.

About 16 percent of bank accounts are inactive. Only about 15 percent of adults and 14 percent of MSMEs access formal credit. To fulfil MSME credit demand, the banking sector needs to be at least 30 percent larger than it is today, if not more. Insurance penetration remains at 3.7 percent of GDP, and mutual fund assets remain low relative to GDP and concentrated in the largest cities, while most GCCs continue to operate from a small group of tier-1 locations. These gaps are compounded by macroeconomic and geopolitical pressures.

Vijay Mani, Partner and Banking and Capital Markets Leader, Deloitte India, said, “India’s financial services sector needs a bold leap out of legacy across technology, customer experience standards, market infrastructure and policy frameworks. This requires reducing reliance on deposits for credit by deepening debt markets and improving risk transmission and rates. As India advances towards its Viksit Bharat 2047 vision, it must expand inclusion for households and MSMEs while strengthening services for large corporates.”

The report calls for action (strategic imperatives) across banks and NBFCs, insurance, asset management and financial services GCCs.

For banks and NBFCs, deepening bond markets must be supported by market-led benchmarks, calibrated reserve requirements, risk-based Basel III frameworks, PSL recalibration and asset tokenisation to improve lending and capital allocation. This will require stronger DPI for lending, transparent MSME credit tracking, integrated fraud prevention and efficient last-mile delivery. Institutions must rebalance portfolios, strengthen deposits and resilience and ensure that investments in AI and post-quantum readiness drive productivity and better customer outcomes.

SOFSI offers a forward-looking view of these imperatives to help financial services participants prepare for the next phase of their evolution.