AI Spending Is Crowding Out IT Services Spend

FinTech BizNews Service

Mumbai, April 29, 2026: AI spending is crowding out IT services spend, even as total tech spending is growing at an accelerated pace. Every large player is operationally sound, eliminating share gains that cushioned performance for a few, a departure from the past 10-15 years, where at least two players had operational/execution challenges. AI deflation is becoming a reality (our base case is 3.5% for the industry), even as there is a timing lag in new programs resulting in weaker-than-expected growth guidance. Stock valuations are inexpensive for a sector that does not have much going for it. Mid-tier players are better-positioned than incumbents.

Slower growth amid AI-driven budget shifts

AI spending is crowding out IT services spend, even as total tech spending is growing at an accelerated pace. Every large player is operationally sound, eliminating share gains that cushioned performance for a few, a departure from the past 10-15 years where at least two players had operational/execution challenges. AI deflation is becoming a reality (our base case is 3.5% for the industry), even as there is a timing lag in new programs resulting in weaker-than-expected growth guidance. Stock valuations are inexpensive for a sector that does not have much going for it. Mid-tier players are better-positioned than incumbents.

None of above factors are new; 4QFY26 reinforced what was already known

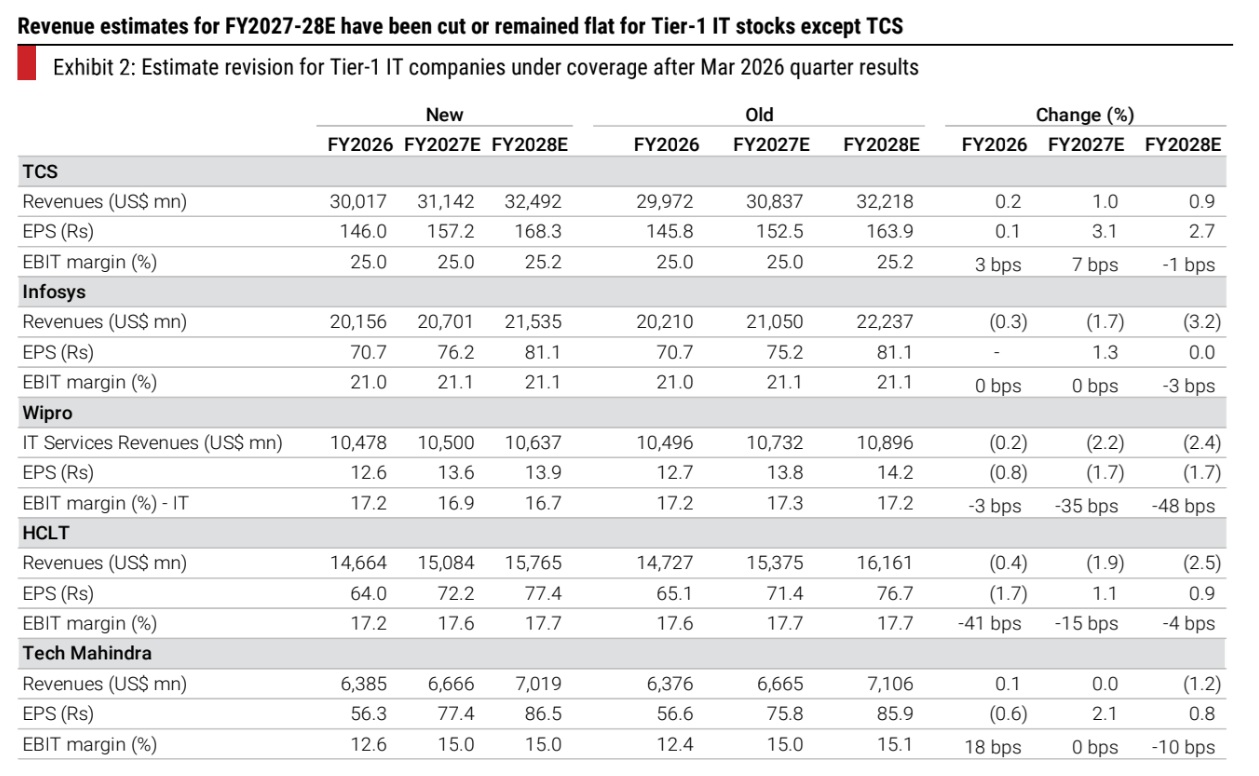

Investors may ask what 4QFY26 results revealed that was not already known. The honest answer is that very little is structurally new. AI deflation as a risk was well-flagged. Demand weakness was visible by March 2026. Competitive intensity was a known concern. What 4QFY26 did was reinforce and quantify. HCLT put a number on AI deflation level for the first time at 3-5% for the industry. Revenue misses were broader and deeper than the Street expected, with every Tier-1 except TCS missing estimates. The results did not change the thesis; they compressed the timeline for when the thesis bites. The market had been pricing marginal recovery in FY2027; the results confirm there is no recovery in sight. That is the new element.

All players healthy; the share gain offset is gone

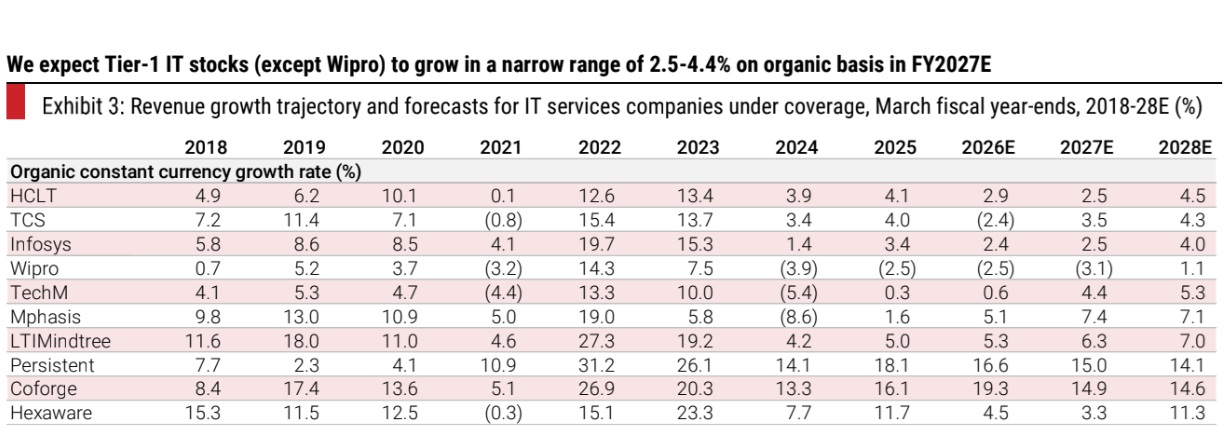

The dispersion in growth among Tier-1 companies may reduce in FY2027E (except Wipro). Over the past 10 years, at least 2-3 players have gone through operational execution challenges—TCS was absent from mega-deals, CTSH was in multi-year recovery, TechM was in self-inflicted decline, and Wipro had multi-year challenges of execution. Weak players gifted shares to strong ones. FY2027 guidance bands and consensus growth estimates are now tightly clustered at 1 to 4% across Tier-1 companies. TCS is back in mega-deals with a US$12 bn TCV. TechM has executed its turnaround and is winning large telecom contracts. Every player now bids for the same deals, in the same markets, at the same productivity benchmarks. The total deal market has not expanded to accommodate them. The share-gain era is over and is getting difficult. What remains is a fight over a services pie that is growing in nominal terms but shrinking in AI-adjusted pricing terms for Indian IT companies.

Deflation is arriving through renewals, the mechanism of deflation matters

The earliest GenAI use cases were in code generation and application development and were supposed to be the first deflationary hit. The actual pressure has arrived through renewals of large multi-year contracts, where clients embed productivity expectations into pricing. The distinction is relevant for margin forecasting. AI reducing the cost of delivery with proportionate headcount reduction is margin neutral for the vendor. A client demanding a price cut on an existing scope while the human intensity of work is unchanged is unambiguously negative for margins and revenues. A third scenario is expanded scope at the same price, which is margin dilutive but at least sustains revenue. What is not clear is the nature of renewals. Renewals of the first category are margin neutral, whereas the second and third categories are dilutive. In the normal course, the impact would have been visible through margin pressure, though rupee depreciation has made the visibility of transmission difficult.

Reasons to be constructive: Real but narrow

Three positives exist for the sector. GenAI deflation is cyclical, not secular, the 2-to-3-year deflationary phase gives way to new AI implementation work in data architecture, agentic workflow deployment and AI governance that did not exist as a billable category. Not all large companies will be able to capture this. Mid-tier is better positioned with PSYS leading the way.

Second, certain verticals are still in the pink of health such as financial services and E&U. Further, while the overall deal intensity has moderated, there are a few mega-deals still flowing through. Third, valuations are not demanding. Current Tier-1 prices embed only 3 to 4% USD revenue CAGR to perpetuity at stable margins, not a steep assumption for competent players with strong deal pipelines. This is a valuation floor, not a re-rating catalyst. Near-term earnings cuts remain a risk, but the downside from current levels is limited for the better-positioned names.

Services is partly funding enterprise AI spend

Enterprise technology budgets are not expanding fast enough to accommodate both AI infrastructure and services spending. The incremental dollar in enterprise tech is going to GPU infrastructure, foundation model licenses and AI software. These categories are inflating rapidly and consuming a rising share of fixed IT budgets. Total tech spending has grown at 10.9% in 2025 and likely to accelerate to 13.4% in CY2026, according to Gartner. On the other hand, IT services has grown at a rather tardy 3.1% in CY2025 and forecast of 4.2% in CY2026. POC spending compounded the sector challenges through 2025. Clients ring-fenced budgets for GenAI pilots that would otherwise have gone to services contracts. The shift to production from POCs does not relieve this pressure. Production deployments feed directly into renewal negotiations. Clients working with AI in production demand efficiency gains be passed through to pricing on existing contracts. The crowding out has been continuous, first from POC budgets and now from production-driven renewal pressure. The new implementation opportunity is large but masked by upfront deflationary pressure, while new opportunities are more gradual.

The long term debate is straightforward—will services spending grow?

The 10-year average growth rate for global IT services spending has been around 5% in constant currency terms. That number has slowed to roughly 3% in CY2025, according to Gartner, and is likely to remain range-bound around this level through CY2026 and beyond. Bears extrapolate this slowdown into an outright decline in IT services spending over the medium. That conclusion is premature. The counterpoint is not whether total technology spending will increase. Tech spending intensity is clearly increasing, driven by AI infrastructure, software and cloud. The real question is whether enough of this incremental spend flows through to the services bucket. For the bear case to hold, one of two things must happen: IT services spending decelerates further to 1-2% or decline, or competitive intensity rises so sharply that industry margins collapse. The latter is possible with the renewal pricing pressure a genuine risk, but the deterioration so far is not sufficient to change the view that revenue growth and EBIT growth should broadly move together over a cycle. On the spending side, industry forecasts and Google’s work on agentic AI adoption suggest there is sufficient complexity, integration and operational work for IT services to continue growing, even if at a slower rate than history. At ~3% growth, the IT services sector remains investable. The challenge is not growth disappearing, but the absolute pool growing slowly while competitive intensity remains high.