The risk-reward in the sector is now turning attractive.

FinTech BizNews Service

Mumbai, October 3, 2025: Kotak Institutional Equities has come out with a noteworthy report on IT Services.

Steadier quarter for IT services

We expect a steadier quarter for IT services, with sequential growth of 0.2-6% across companies. We believe that the rupee depreciation, combined with cost measures, will ensure steady margins. Deal wins will likely be steady to strong, but cost takeout-driven and intensely competitive. In our view, Infosys, Coforge and LTIM will report a strong quarter, while Wipro and TCS will trail. We incorporate KIE economist’s revised currency rates and potential H-1B risks, and take a more conservative stance about FY2027 recovery, leading to a 0-3% cut in FY2026-28E EPS and a 2-9% cut in fair values. The risk-reward in the sector is now turning attractive. Infosys, TechM, Coforge and Hexaware are our key picks.

One of the better quarters

Unlike the earlier quarters, there has been no demand deterioration through the course of this quarter, a positive. We expect all Tier 1 companies to report sequential growth, with Infosys leading the pack at 2% qoq. Mid-tier companies should report another strong quarter, with growth in the range of 1.5-6.0%. Coforge will likely once again lead the way on growth at 6.0% qoq, followed by Persistent at 4.0%. ERD companies will likely report another moderate quarter, with organic revenue growth of (-)2.5% to +1.7%, largely due to weak demand in the automotive vertical.

EBIT margins: Rupee depreciation to come to the rescue

Rupee depreciation has come to the rescue in a quarter impacted by pricing pressures and will likely allow for steady margins. Companies may use rupee depreciation to offset the pricing pressure in large deals or increase variable compensation payout. We believe Tier 1 IT companies, except for HCLT, will report steady EBIT margins yoy. Mid-tier companies will likely report a yoy EBIT margin increase, led by leverage from growth and greater margin focus. Wage revision announcements in FY2026 are scarce and may be a focus area.

Guidance: Largely unchanged

We expect Infosys to raise its FY2026 revenue growth guidance to 2-3% from 1-3% earlier—our estimates do not include the recently acquired Versent Group. The guidance implies a revenue decline of (-)1.1% to +0.2% in the next two quarters. HCLT will likely retain its 3-5% revenue growth guidance for FY2026. Wipro’s revenue growth guidance for 3QFY26 will likely move to a positive number of 0.5%, at the midpoint of (-)0.5% to +1.5%.

Estimates update: Bake in revised USD/INR rate

We capture KIE economist’s revised USD/INR rate of 86.9, 89 and 91 for FY2026E, FY2027E and FY2028E compared to 86.1, 88 and 89 earlier. In addition, we moderate our FY2027 recovery assumptions and incorporate 3-6% organic growth for Tier 1 companies, capturing multiple headwinds. Our rationale for growth acceleration in FY2027E is based on a reduction in the current headwinds, viz., macro headwinds and loss of share to captive centers. The recovery will be partly offset by a higher deflationary hit from GenAI adoption by enterprises. The key changes to our estimates and Fair Values are detailed in Exhibit 15.

We bake in continued uncertainty in the demand environment through a 1-2X cut in multiples. The risk-reward is turning attractive after the recent correction. Our top picks are Infosys, TechM, Coforge and Hexaware.

At an interesting juncture—multiple headwinds with a couple of offset

Indian IT services companies are at a crucial juncture, with undercurrents of technology evolution amid multiple business challenges: (1) wallet share shifts within enterprise tech budgets, (2) growing relevance of captives, (3) macro and regulatory uncertainties and (4) tightening immigration norms. The result is a sharp moderation in revenue growth to low-single digits and profitability pressures becoming more evident for companies aggressively participating in vendor consolidation deals. The growing relevance of as-a-service companies and investments in AI initiatives have constrained growth in services budgets even as overall tech spends have grown at a reasonable rate. Further, rising mid-market captive setups have led to a rethink of enterprise sourcing decisions. While most companies have put in place dedicated teams to tap into the opportunity, it is unlikely to be net-new for the industry.

A tougher stance on immigration policies was expected under the Trump administration. However, large transformation projects can get stuck in limbo, given the elevated demand and supply-side uncertainties. We believe that companies can absorb incremental costs, which could have a moderate impact on the profitability before exploring mitigation measures. However, stringent measures to limit offshoring activity could have wide-ranging implications.

We expect genAI to be initially deflationary to the extent of 2-3% in the next 2-3 year period. GenAI use cases are currently focused on productivity improvement, with tools and accelerators acting as coding assists, addressing summarization and knowledge management use cases as well as contact-center BPO. We expect the impact to be higher in these areas as the adoption picks up. We believe that most of the current hype around agentic AI will eventually cool off.

The positives are (1) pressure on captive shift is reducing and (2) although FY2026 is adversely affected by the tariff war uncertainty, the impact may recede going into FY2027.

Valuation multiples would be under scrutiny in case of limited improvement in CY2026 budgets

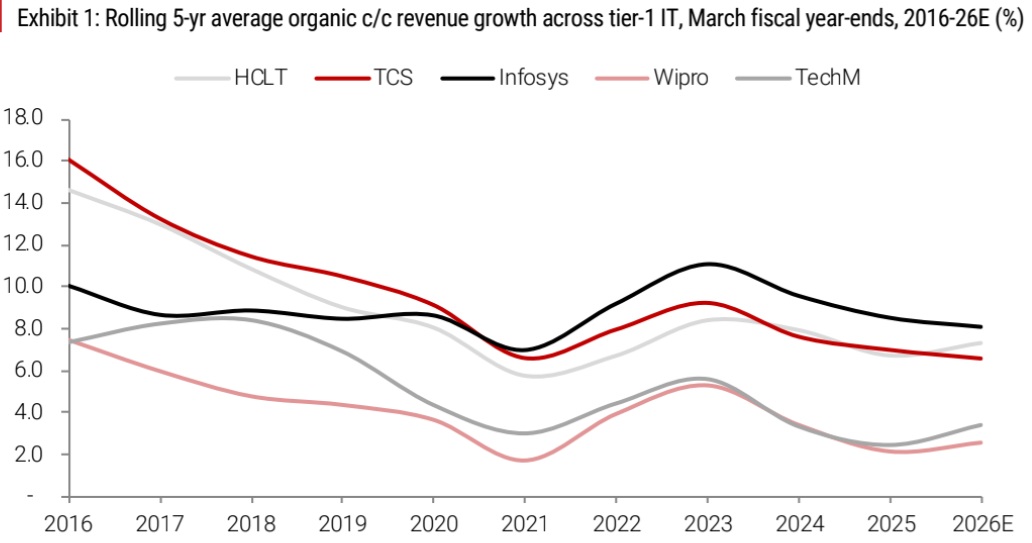

On a five-year average basis, organic revenue growth across tier-1 IT (ex-Infosys) has decelerated (Exhibit 1). Infosys has maintained its growth rate in a tight band. Another year of the continuation of a subdued demand environment would feed into the popular narrative of AI hurting the prospects of IT services companies, and this perception may weigh on valuation multiples, in our view.

In a perverse manner, the slowdown in AI initiatives of clients due to either not-justifiable RoI or a lack of enterprise readiness would free up incremental budgets for services companies. A moderate re-rating is likely in this scenario.

We continue to prefer Infosys, TechM, Coforge and Hexaware within our coverage. Infosys’s ability to participate in large deals, investments to capture growth opportunities and proactive measures to maintain profitability underpin our preference for the company. We believe that TechM is on the right path, with improving quality of deals and a gradual improvement in margins, although achieving the aspirational margin band would require some help from favorable macros. Coforge and Hexaware have scalability attributes, even as the businesses have contrasting dynamics. They are our picks in mid-tier IT.

Another moderate quarter for ERD services pure-plays

LTTS is likely to lead pure-play ERD services companies on qoq revenue growth at 1.9% c/c. The services business of TTL should remain reasonably strong despite the weakness in both anchor clients. However, the weakness in technology solutions segment would limit revenue growth to 1%. The weakness in automotive is likely to result in a 2.4% revenue decline for KPIT on an organic basis. TELX and Cyient (DET) are likely to report modest growth and margin improvement. We expect minimal disruption from the cybersecurity incident at JLR for TELX and TTL. We do not expect significant improvement in demand in the December quarter in the automotive segment, given the shift in the priorities of clients. While the deal pipelines across companies remain at peak levels, conversion and ramp-up timelines remain uncertain. Hopes of an improvement would be pinned on CY2026 budgets, which would bake in reduced regulatory uncertainty while end-consumer preferences remain fluid. European auto OEMs are significantly focused on reducing their cost structures, which could play out in increased offshoring of R&D activity. However, some of this would be meant to improve their competitiveness in China, which is unlikely to benefit Indian pure-play ESPs. Further, increased competitive intensity should result in pricing pressures for new engagements.

Healthy performance across BPO services providers

In our view, pure-play BPO services providers should report a reasonable quarter, with organic qoq revenue growth in the range of 2.2-4.8% c/c, with Sagility leading on sequential revenue uptick. On an organic yoy basis, revenue growth would be in the range of 9.3-14.6%, led by eClerx. Revenue growth would be led by the healthcare vertical for FSOL and Sagility, while the continued strength in BFS should help eClerx. Profitability should improve as well across companies qoq. Operating leverage should aid a 240-bps qoq uptick at eClerx. FSOL should improve EBITM by 20 bps qoq to 11.5%. Adj. EBITDA margin at Sagility is likely to improve by 80 bps qoq to 24.8%. We expect Sagility to raise adj. EBITDA margin guidance to 24%+ (from 23-24%). GenAI risks remain in parts of the businesses across companies, which could impact the existing book of business in the medium term. However, we believe that challengers can demonstrate better performance, gaining share from incumbents. In our view, industry-specific processes will be relatively resilient in the near term.

Key metrics to watch out for

4 | Deal wins. Deal TCV has been healthy in the past few quarters, dominated by large cost-takeout and vendor consolidation deals. We expect a similar trend in the September 2025 quarter as well. TCS, Infosys and HCLT have all announced large deals during the quarter. However, these include significant renewal portions. Further, net new deals for companies have mostly been a result of wallet share shifts between services providers rather than incremental technology budgets. These deals typically are fiercely competed for, resulting in significant pricing pressure. A few companies with a track record of strong engagements with clients and delivery excellence should continue to gain share. Select mid-tier challengers have aggressively gained share against larger competitors. |

4 | Headcount. Utilization as a lever has maxed out for most companies. Further, campus hiring picked up in the past year to realign the employee pyramid, which has deteriorated in the past couple of years. The September quarter would usually involve the onboarding of trainees. Most companies should register headcount additions. TCS and HCLT have undertaken a significant employee restructuring program. We expect TCS to report a headcount decline on a sequential basis. |

4 | GenAI. Capabilities and enterprise adoption are picking up, led by better models, maturity of end-applications, reduced inference and training costs and lower latency. However, the benefits of brownfield implementation have not met their promise. Use cases to realize new/alternate revenue streams are yet to emerge. In the interim, a deflationary impact is likely, but the debate on the extent and offsets available with companies will continue. |

4 | Onsite wage implications. We believe that the tighter H-1B norms will nudge companies to either increase the dependence on subcontractors or step up local hiring. 9MFY25 H-1B visa applications have been significantly lower across most companies. While onsite tech unemployment remains near the long-term average, sudden changes in demand-supply dynamics could lead to an escalation in onsite wage costs for companies during a period of subdued demand. The ability to pass on these costs to clients would be monitored. |

Discussion on individual companies

4 | TCS. We forecast moderate revenue growth of 0.2% qoq. The ramp-downs in a few accounts and share losses could lead to moderate growth. We expect stable EBIT margins; the impact of the wage revision, effective September 1, will be offset by rupee depreciation. P&L charges from employee separation are not baked into our estimates. We expect TCV of US$10 bn+ for the quarter. The company has announced a mega-deal in the quarter. The focus will be on the rationale for the planned 12k employee separation, the impact on employee morale and costs associated with the separation. We expect investor focus on (1) the reasons for the underperformance in growth in developed markets and any potential share losses; (2) whether the impact on demand resulting from the imposition of tariffs by the US subsided; (3) the pace of GenAI adoption and deflationary impact on spends; (4) the impact of GCC ramp-up on the growth of companies and GCC as a growth lever; (5) H-1B dependence and plans for further de-risking; and (6) margin aspirations in light of elevated competitive intensity. |

4 | Infosys. We forecast revenue growth of 1.8% qoq, driven by (1) higher billing days and (2) continued strength in the financial services vertical. We do not assume any incremental revenues from the sale of third-party items. We expect stable EBIT margin both qoq and yoy. Tailwinds from rupee depreciation should be offset by the normalization of the provision of post-sales client support, compared to a reversal benefit of 40 bps in the June 2025 quarter. We expect large-deal TCV of US$3 bn, ~22% growth yoy and a decline qoq. We believe that Infosys will raise FY2026 revenue growth guidance to 2-3% from 1-3% earlier. The revised guidance will imply a decline in revenues in the second half. Our guidance estimates do not include the recently announced acquisition of Versent Group. We expect investor focus on (1) program cancellations and the impact on demand from verticals directly affected by the imposition of tariffs by the US; (2) pricing pressure in large deals; (3) the key markers for improvement in discretionary demand; (4) the pace of enterprise AI adoption and the resultant pricing and deflationary pressure; (5) estimates embedded from the sale of third-party items in the second half of FY2026; and (6) H-1B dependence, measures to reduce it and margin implications. |

4 | HCL Tech. We forecast 1.7% qoq growth, driven by mega-deal ramp in engineering services. Growth will be led by the services business (1.8% qoq), while the products business’ growth at 0.8% qoq will be marginal. We forecast an underlying EBIT margin increase of 70 bps qoq to 17%. EBIT margin is after 50 bps of restructuring charge. We expect an EBIT margin decline of 160 bps yoy due to the base effect, wherein, for 2QFY25, there was a large license booking in the products segment. We expect healthy TCV of deal wins in the US$2.5-3 bn range. HCLT closed two large deals that management hoped for and communicated in its 1QFY26 earnings call. We expect the company to retain 3-5% revenue growth guidance for FY2026, along with 17-18% EBIT margin guidance. We expect investor focus on (1) the path of margin recovery to the 18-19% band; (2) the impact of reciprocal tariffs imposed by the US on directly impacted segments of manufacturing and retail; (3) profitability in cost takeout and vendor consolidation deals; (4) the state of discretionary spending; (5) the pace of enterprise GenAI adoption, new opportunities consequent to AI adoption and the likely deflationary impact; and (6) the underlying environment for growth to accelerate to high-single digits. |

4 | Wipro. We expect growth near the midpoint of guidance at 0.2% c/c qoq. The performance is an improvement from the underwhelming growth in the earlier quarter. We forecast an EBIT margin decline of 40 bps qoq despite rupee depreciation. The decline is largely due to upfront costs associated with large deals. We expect large-deal TCV to be in the US$1.5 bn range, a strong outcome, noting the recent aggression in large-deal pursuits. We expect a revenue growth guidance of (-)0.5% to +1.5%. The positives of the quarter are the ramp-up of Phoenix and other mega-deals. The negatives are furloughs and a weak demand environment. We expect investor focus on (1) the state of demand in the tariff-impacted sectors of retail and manufacturing; (2) costs associated with large deals— the pricing pressure is intense in large deals; (3) large-deal pipeline and win rates; (4) the pace of GenAI adoption and its deflationary impact on services spends; (5) GCC growth strategy; and (6) catch-up timeframe on growth with peers. |

4 | TechM. We forecast c/c revenue growth of 0.9%, led by financial services and retail. We expect a stable communications vertical. We expect EBIT margin expansion of 70 bps to be led by leverage from growth and rupee depreciation. We forecast net-new deal wins of ~US$800 mn, stable qoq and a 33% increase yoy. More important, new deals are won at higher margins. We expect further margin improvement and expect the company to exit FY2026E with 13% EBIT margins. We expect investor focus on (1) the path to profitability of 15% in FY2027 in light of a challenging macro environment; (2) deal-win acceleration, necessary for revenue growth and margin aspiration; (3) growth in the keenly watched financial services vertical; (4) H-1B visa dependence and risk mitigation measures; (5) health of deal pipeline and positioning in cost take-out deals; (6) any revenue leakage in existing accounts; and (7) TechM's point of view on GenAI, expected productivity benefits and the likely disruption in the BPO business. |