India now ranks 3rd globally in AI capability (up from 7th in 2025), with 3,100+ AI start-ups, USD 2.9 Bn raised by top 100. The USD 5–50 Mn mid-stage AI start-ups have proven product-market fit, early revenue traction, and capital-lean operations. The report examines where innovation is thriving, where opportunities remain untapped, and what it will take to build an ecosystem that empowers entrepreneurs to create products and services with lasting impact.

FinTech BizNews Service

Mumbai, March 28, 2026: Indiaspora has released two new reports in partnership with Zinnov, a global management and strategy consulting firm, on Artificial Intelligence’s (AI) impact across India’s Startup and GCC Ecosystem.

Indiaspora-Zinnov report on the Top 100 AI Startups in India examines where innovation is thriving, where opportunities remain untapped, and what it will take to build an ecosystem that empowers entrepreneurs to create products and services with lasting impact.

India now ranks 3rd globally in AI capability (up from 7th in 2025), with 3,100+ AI start-ups, USD 2.9 Bn raised by top 100. The IndiaAI Mission (Rs10,372 Cr), USD 200 Bn+ in commitments, and population-scale digital infrastructure (Aadhaar, UPI, DigiLocker) create a rare convergence where decisive action in 2026–27 will define India's AI trajectory for the next decade.

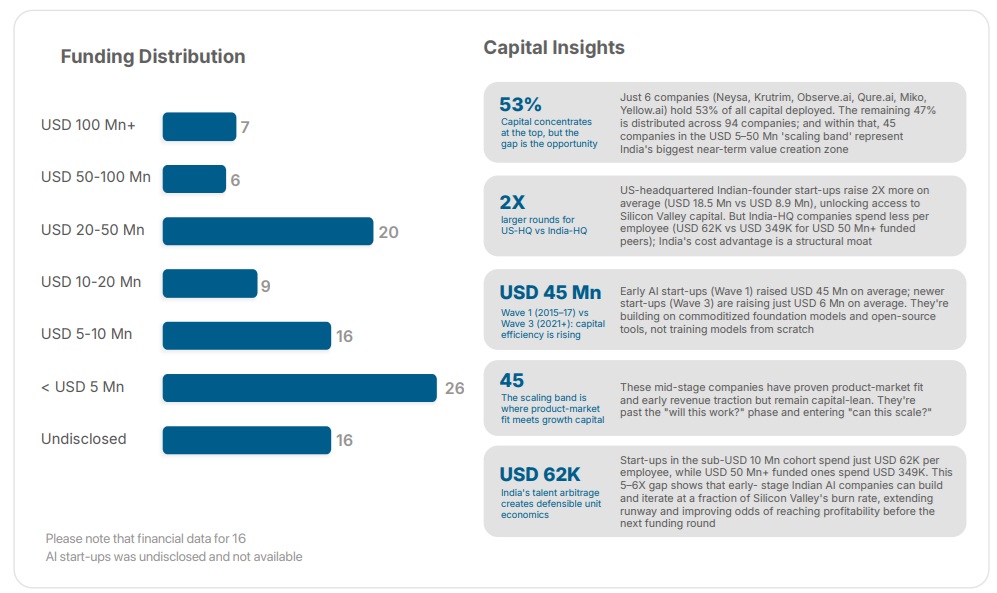

The USD 5–50 Mn mid-stage AI start-ups have proven product-market fit, early revenue traction, and capital-lean operations. They've moved past "will this work?" and are entering "can this scale?" This cohort is positioned beyond binary execution risk but remains pre-hypergrowth valuations, creating a high-concentration zone for strategic investment and partnership opportunities.

Early-stage start-ups spend USD 62K per employee vs USD 349K for late-stage peers. Wave 3 companies (2021–24) raise USD 6 Mn on average vs USD 45 Mn for Wave 1, yet ship faster by building on commoditized foundation models. This 5–6X efficiency gap extends runway and enables paths to profitability—transforming cost structure from operational advantage into strategic moat.

Investment flows to: (a) autonomous B2B agents with deep vertical integration (BFSI, Healthcare, Legal, Agriculture), (b) sovereign AI infrastructure (compute, models, governance), and (c) proprietary datasets.

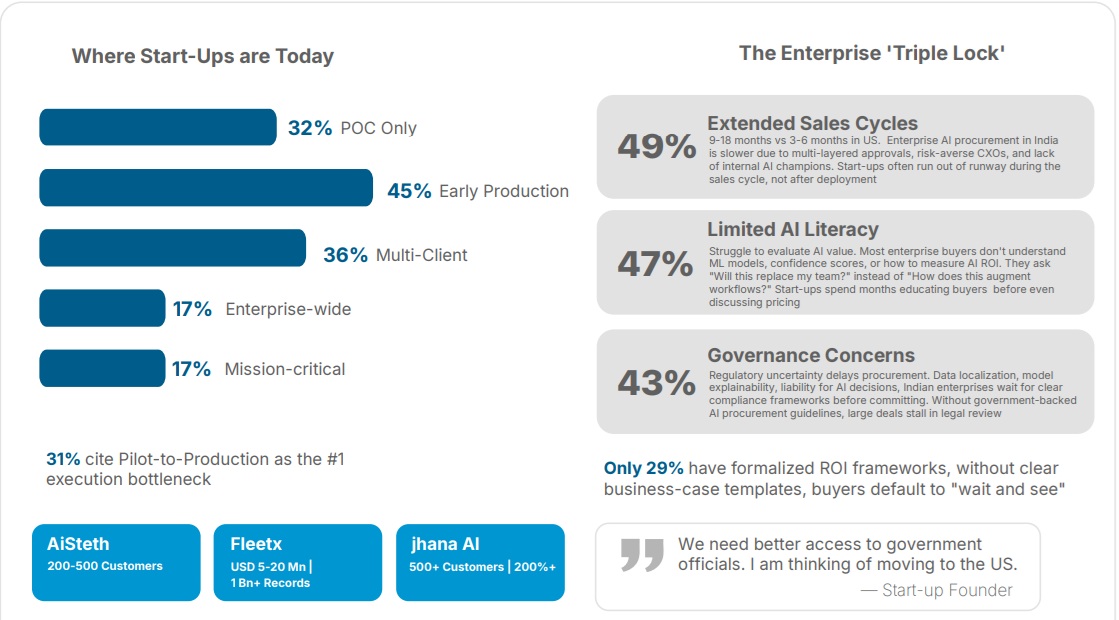

Start-ups that build repeatable deployment playbooks, embed trust-by-design (explainability, governance), and create formalized ROI frameworks capture disproportionate market share. Companies solving the pilot-to-production gap are winning multi-year enterprise contracts despite extended sales cycles (9–18 months).

According to Pari Natarajan CEO Zinnov, India is not catching up to a global AI wave. India is beginning to set its own terms. For much of the last decade, the Indian tech narrative was about convergence, replicating proven playbooks, adapting global models to local conditions. That chapter is closing. Across 3,100+ AI start-ups analyzed for this report, something qualitatively different is visible: an ecosystem that has stopped asking how do we get there, and started asking where exactly are we trying to go? India entered the AI era with an unusual inheritance, Aadhaar, UPI, ONDC. Public rails that make new applications cheaper and faster to build here than almost anywhere else. But the DPI edge is not automatic. It requires the coordinated, whole-of-nation intent that produced cryogenic engines and 4G equipment and India Stack itself. The AI chapter demands the same. The durable businesses are not the ones with the most compute. They are the ones with the clearest answer to who this works substantially better for, and why. Wrapping a frontier model in a chat interface is not a company. It is arbitrage with a shelf life measured in months. The real opportunity lies in frugal, localized - models tuned to Indian languages, SME workflows, and actual compute realities. DeepSeek proved globally what Indiaʼs constraints have long demanded domestically: disciplined architecture beats scale when the market is specific enough.

SIX THESES

Infrastructure is the moat. India Stack gives founders structural advantages no one replicates from outside. AI extends this — it doesnʼt replace it. Frugal beats large. The winning model is not the biggest — itʼs the most precisely tuned to Indian languages, sectors, and realities. 18–36 months to differentiate. The application layer will commoditize fast. Proprietary data, integration, and distribution must be built now. Coordination is not optional. Indiaʼs biggest tech wins were never market accidents. AI requires the same whole-of-nation alignment.

Building for Bharat: India's AI is going to be its AI Doctors, AI Tutors, AI Financial Advisors, AI Farmers & more.

AI-led Services: India led in Services 1.0. No reason it cannot again lead in Services 2.0, which is 80% AI and 20% human

The direction is clear. Indiaʼs AI story will be won at the intersection of public infrastructure depth, frugal model architecture, and founders who build systems that are, by design, hard to replicate from anywhere else.

India's AI Landscape

India's AI market is entering a defining phase; 2026–27 is the window to build category-defining companies

2016–2020

India Stack (Aadhaar, UPI, eKYC, DigiLocker) built population-scale digital rails for identity, payments, and data Policy direction emerged early (NITI Aayogʼs National Strategy for AI), framing AI as public infrastructure AI activity remained limited; value creation concentrated in talent supply across IT Services, start-ups and GCCs.

2021–2023

GenAI momentum accelerated interest, but institutional response focused on capacity building (CoEs, datasets, skilling) INDIAai* evolved into a national knowledge and coordination platform, signalling intent to mainstream AI Enterprises and GCCs remained in pilot mode: high POC volume, limited scaled deployments, unresolved governance and liability.

2024–2025

The IndiaAI Mission (Rs10,372 Cr / USD 1.2 Bn) marked a shift to direct state investment in compute, data platforms, start-ups, and research AI talent became a structural advantage, with India emerging as one of the deepest global AI talent pools Governance formalized via India AI Governance Guidelines 2025, embedding safety, accountability, and sandbox-led innovation.

2026+

Strategic focus shifts to AI sovereignty: building domestic compute, models, and platform capabilities AI integrates into digital public infrastructure and sectoral systems, moving from pilots to population-scale deployment Trust, safety, and localization emerge as key differentiators as enterprise AI spending scales Indiaʼs next challenge: convert digital public infrastructure and talent advantage into globally competitive AI products and platforms.

USD 126 Bn: India AI Market Opportunity by 2030.

USD 1.7 Tn: Indiaʼs GDP Impact by 2035.

3rd Global AI Ranking — up from 7th (2025).

3,100+ AI Start-ups in India (as of FY2025)

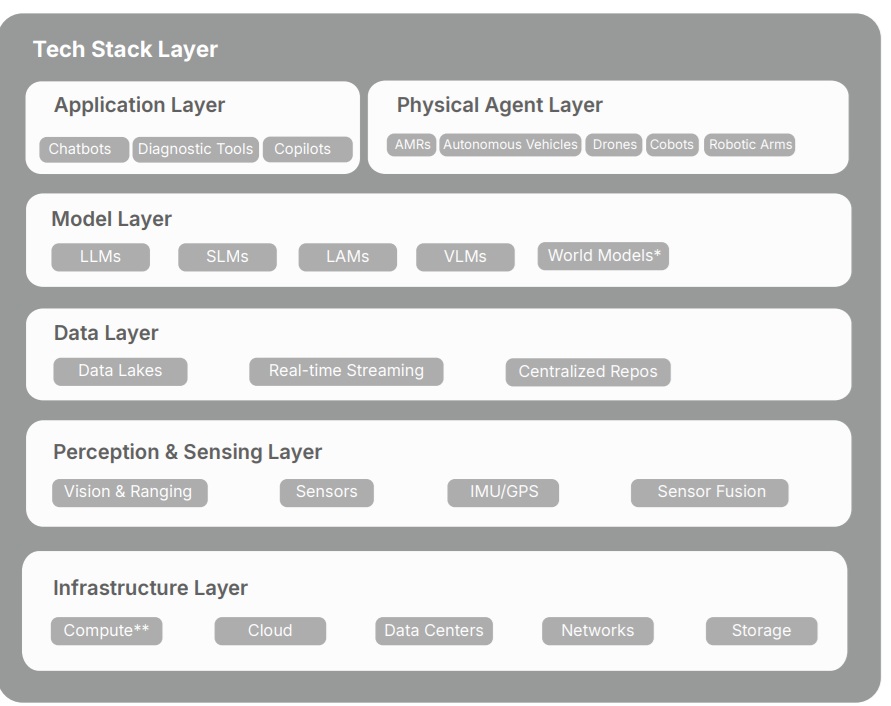

India has built strong application and model capabilities, and continues to develop sovereign compute, data, and Physical agent layer.

Three decades of technology heritage, a decade of digital infrastructure, and accelerating capital give India an AI foundation no other market can build in time.

Policy & Government

IndiaAI Mission

Rs10,372 Cr funds sovereign compute, research, and skilling; removes GPU access and talent bottlenecks for startups.

AI Impact Summit 2026

USD 200 Bn+ commitments signal global capital now sees India as AI product hub.

Regulatory Approach

Sector-specific sandboxes allow innovation without broad regulatory risk, Fintech AI, Healthcare AI, and Agri AI can ship pilots faster than in over-regulated markets.

Central and State Bodies

Coordinated AI policies (Nasscom, National Data Center Policy, Telangana/Karnataka AI policies) align state incentives with national strategy; reduces fragmentation, speeds adoption.

Technology & Talent Heritage

IT SERVICES: USD 315 Bn* Industry

TCS, Infosys, Wipro, HCLTech built enterprise delivery muscle at scale; this becomes the go-to-market engine for AI productization (implementation, integration, support)

1,760+ GCCs (FY ‘25) AI R&D at Scale

Global Fortune 500s already run AI model deployment, use-case development, and cross-market innovation from India; GCCs are the world's largest distributed AI lab

ACADEMIA AI Talent Pipeline

IITs, IISc, IIMs, IIIT produce AI/ML talent at scale; 38 founders from IIT Delhi alone on Hurun India Future Unicorn Index 2025 top list; proven track record of translating research into commercial ventures.

DEVELOPER BASE: 2nd Largest Globally

GitHub, Kaggle, Hugging Face communities show India's open-source depth; fuels rapid experimentation, reduces time-to-MVP* for AI start-ups

DIGITAL PUBLIC INFRA: Population-scale Rails

Aadhaar (1.4 Bn), UPI (75% of retail), DigiLocker (5 Bn+ docs), 958 Mn internet users (TRAI, 2025); no other emerging market has this level of digital identity + payments infrastructure for AI to plug into.

Funding Environment

USD 643 Mn

AI Start-up Funding across 100 deals in 2025 (+4.1% YoY)

USD 20 Bn+

Hyperscaler Investment Commitments Through 2030 to Build AI-Ready, Sovereign Cloud Infrastructure

8X

Indiaʼs Total Datacenter Capability Growth by 2030 (1GW in 2025 to 8GW in 2030)

WHY IT MATTERS

Indiaʼs AI advantage is not one thing; itʼs a convergence. A USD 315 Bn* IT services industry that built the worldʼs back office. 1,760+ GCCs running enterprise AI. An academic pipeline (IITs, IISc) producing world-class talent. Population-scale digital rails (Aadhaar, UPI) no other market has, and a government that delivered both in under a decade.

Key AI Investors: Lightspeed | Peak XV | Accel | Pi Ventures | Kalaari | Khosla | Stellaris | Blume | Blackstone | FTV Capital

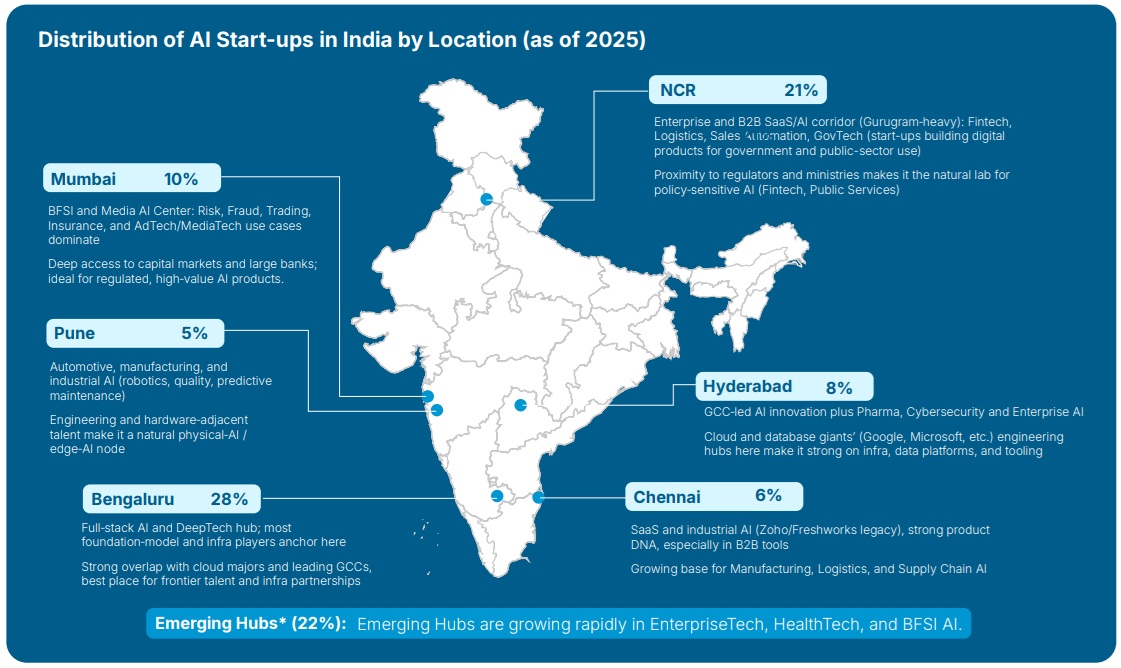

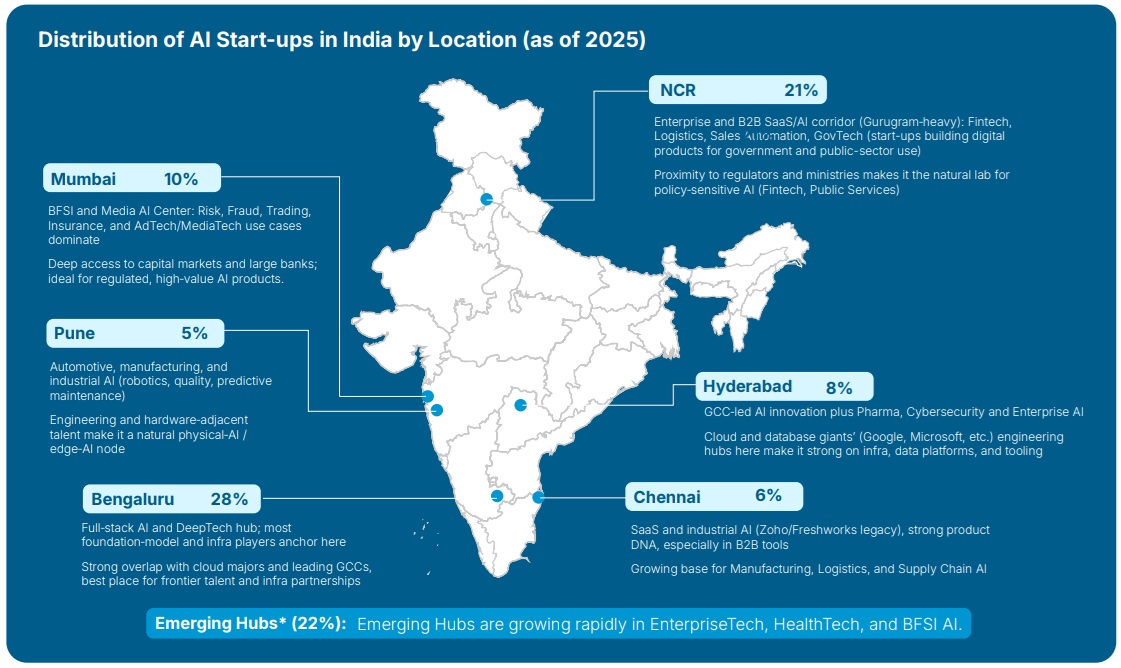

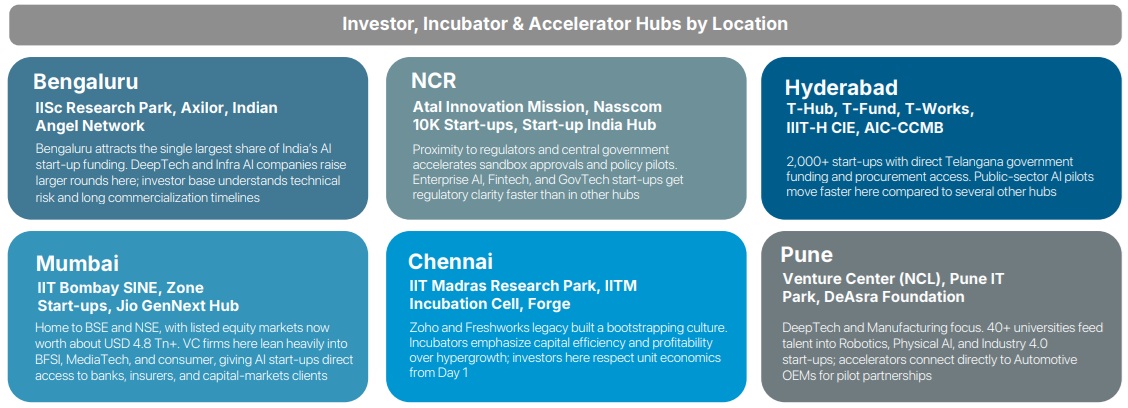

SECTION II: Ecosystem by Location

Bengaluru commands 28% of India's AI ecosystem, but a geography shift is already underway

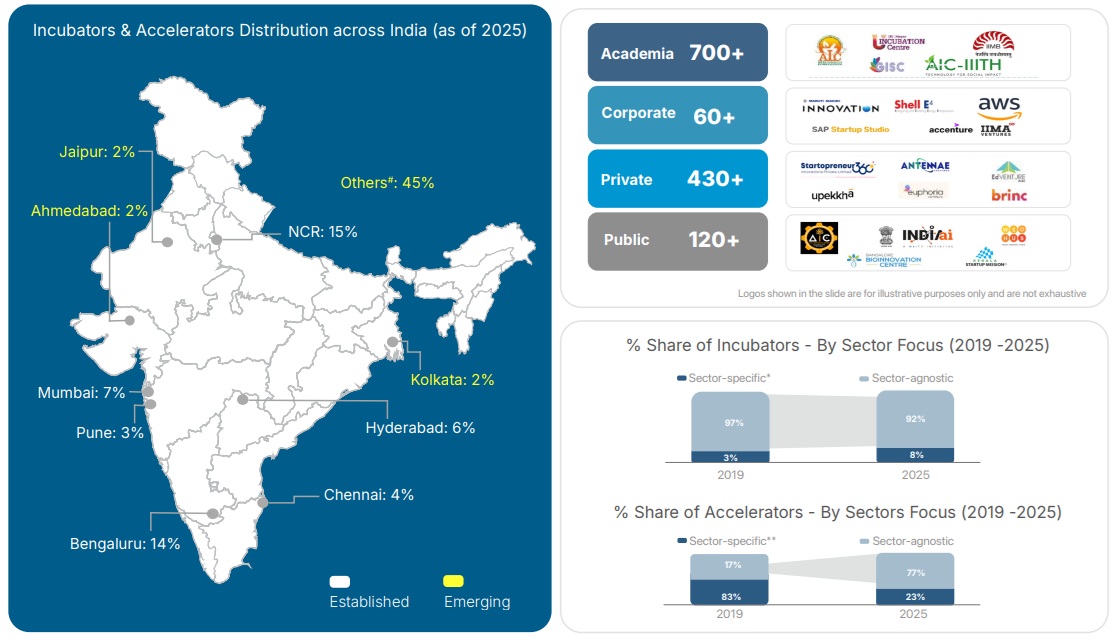

1,300+ Incubators & Accelerators across India, the deepest start-up support infrastructure in any emerging market

India’s AI hubs are becoming specialized, with capital and support aligning to each city’s strengths

Top AI VCs:

Activate, Together Fund, Neon Fund, Boundless VC, Lightspeed, Peak XV, Accel, Pi Ventures, Kalaari, Stellaris, Blume

Global participation:

Khosla Ventures, FTV Capital (USD 150 Mn Kore.ai), Blackstone (USD 600 Mn Neysa). AI Impact Summit 2026: USD 200 Bn+ commitments

Trend:

Investor focus has shifted from rapid deployment to long-term differentiation. Three categories now attract the majority of funding: (1) autonomous B2B agents with deep vertical integration, (2) sovereign AI infrastructure (compute, models, tooling, safety), and (3) companies building on proprietary, hard-to-replicate datasets Seed-stage diligence has become more rigorous; technical moats and clear paths to defensibility now matter as much as traction. Meanwhile, well-differentiated AI companies are seeing faster Series A+ rounds and larger cheque sizes, signaling investor confidence in India's ability to build category-defining AI products.

India's 100 Top AI Start-ups

India’s AI ecosystem is now producing a dense cohort of well-funded, execution-ready start-ups.

All the above insights are derived from analysis of the 100 top AI start-ups in India

The 100 Top AI start-ups represents India's highest-concentration pool of execution-ready AI start-ups, selected through a multi-source framework spanning quantitative scoring, VC validation, ecosystem analysis, and founder surveys. This list now includes both India HQ and Indian-founder global start-ups.

Within India’s 100 top AI start-ups, 45 in the USD 5–50 Mn band are the core scaling cohort

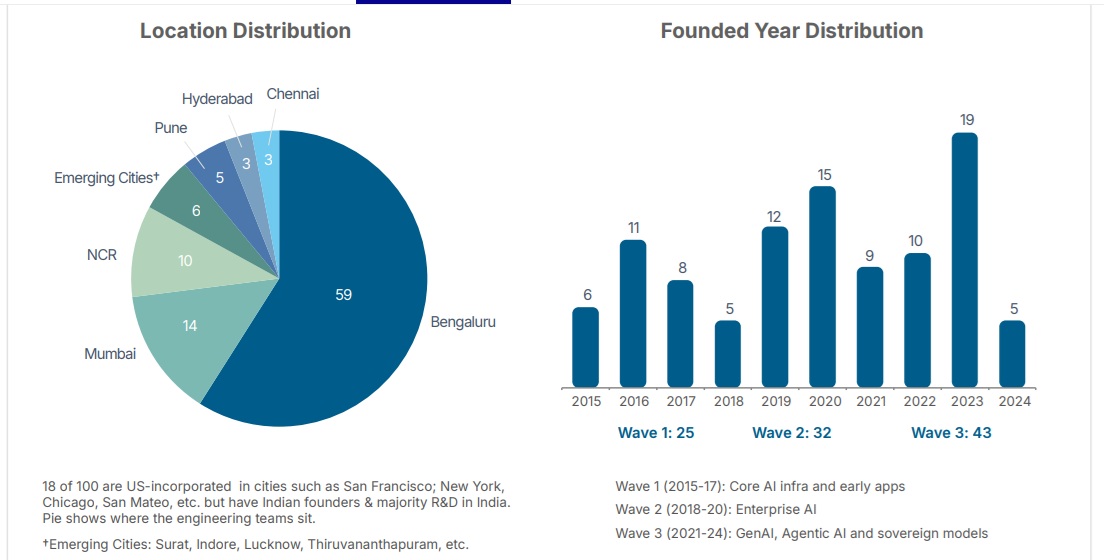

Bengaluru is home to 59 of India’s 100 top AI start-ups, including R&D teams of US-incorporated firms

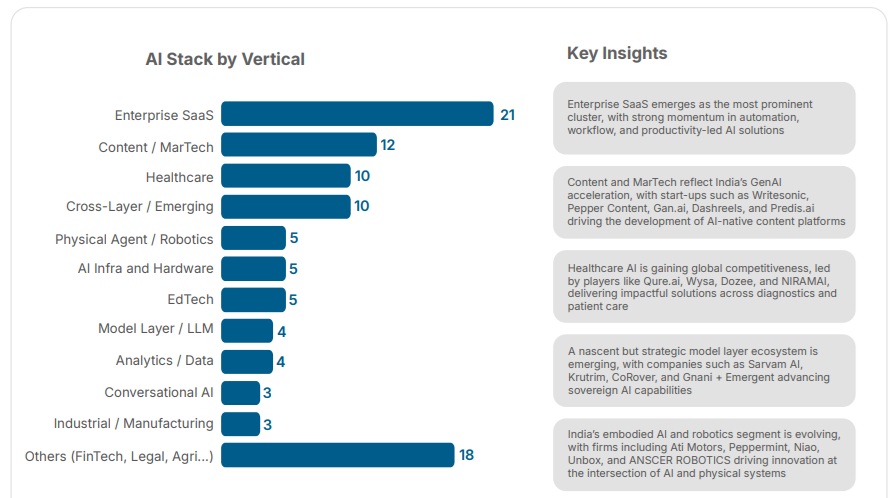

India’s top AI start-ups are concentrated at the application layer, led by Enterprise SaaS, Content/MarTech, and Healthcare

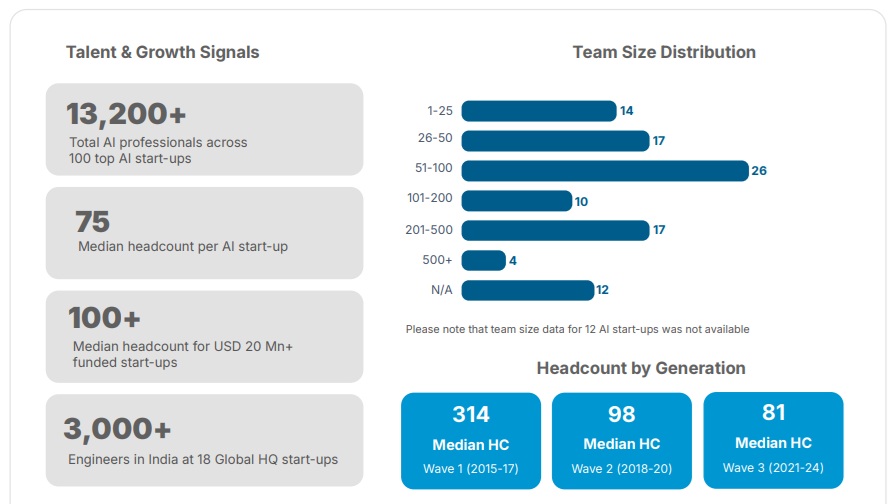

India’s top AI start-ups are building lean, execution-ready teams

India’s top AI start-ups are building lean, execution-ready teams

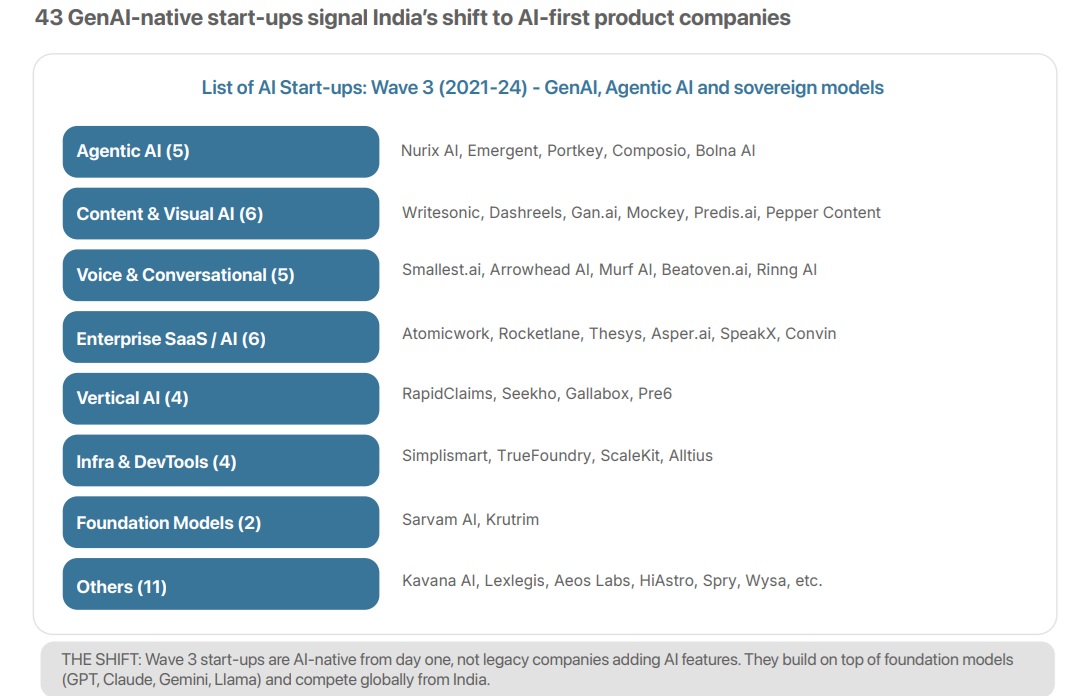

43 GenAI-native start-ups signal India’s shift to AI-first product companies

SECTION IV

Future Outlook & Survey Results SECTION IV What 250+ AI Start-up Founders Told Us

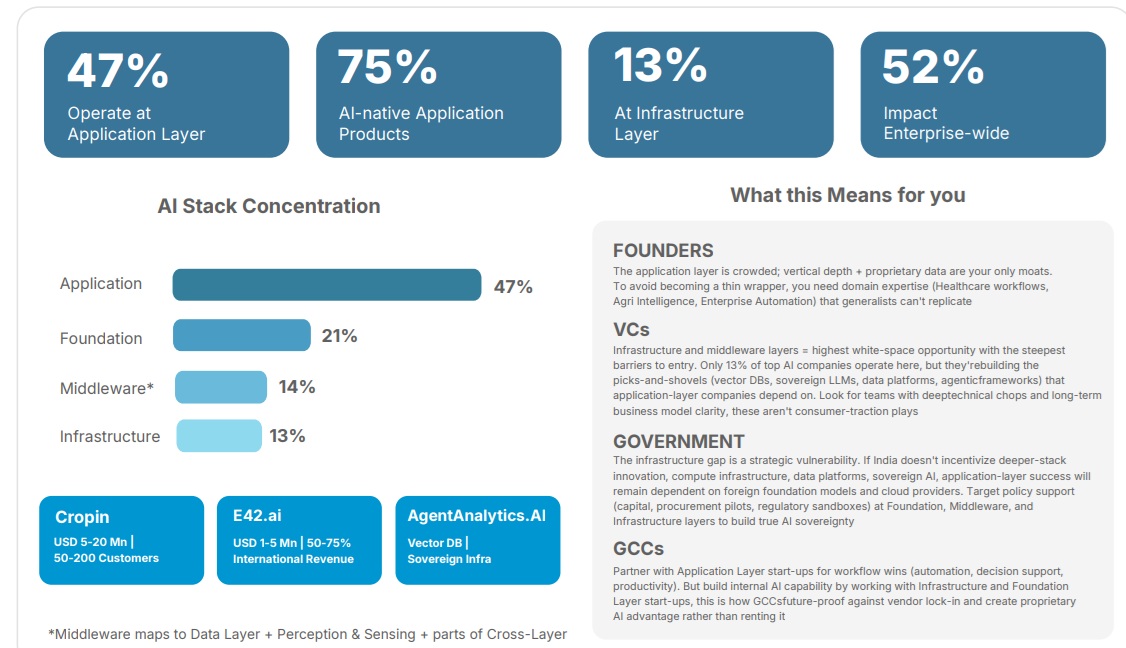

India’s AI ecosystem is application-heavy, the next phase depends on building foundation and infrastructure

AI start-ups are advancing beyond pilots, though enterprise readiness continues to influence scale

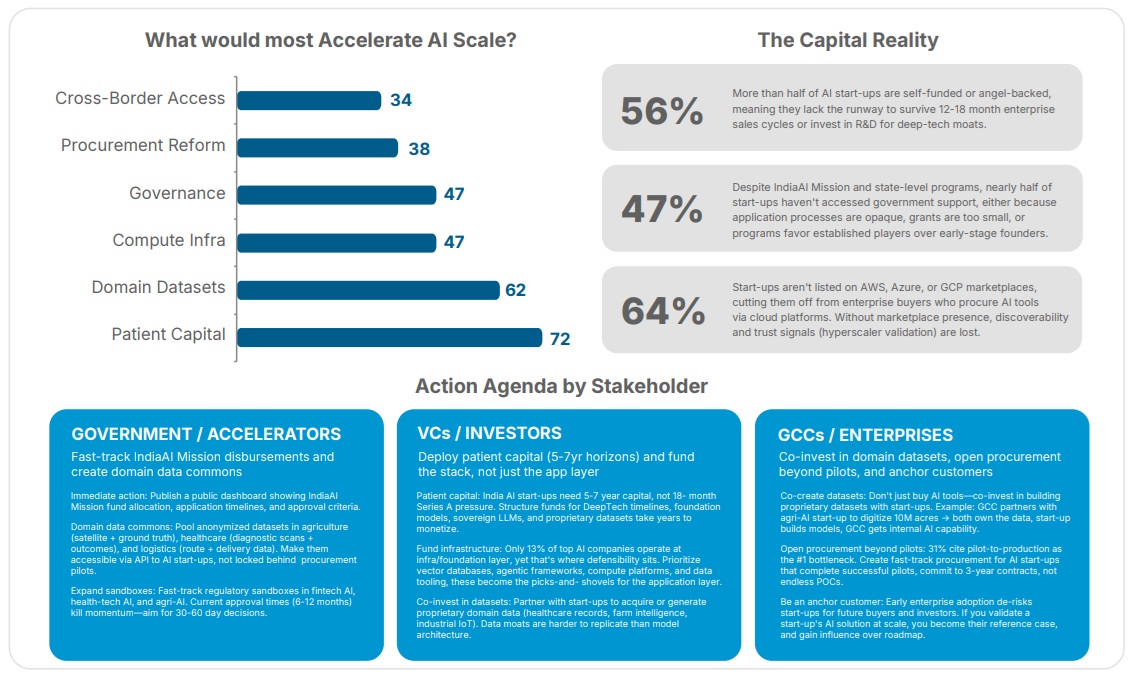

Patient capital and domain data are the key factors shaping the next phase of AI scale in India

.

.

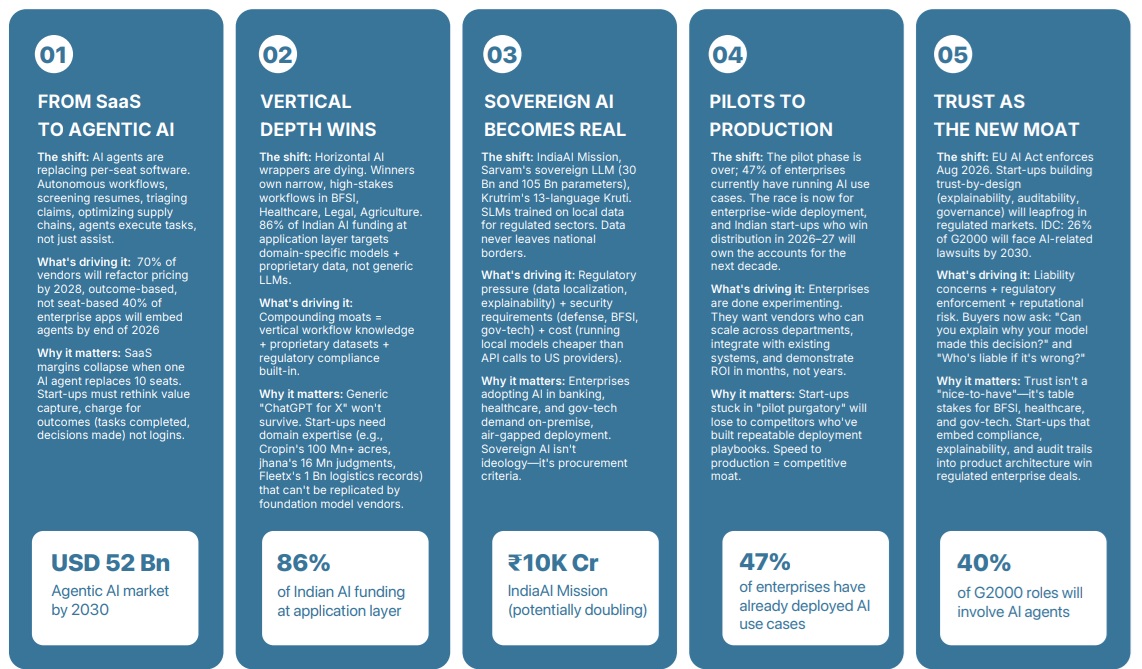

Five Forces Shaping India's Next Generation of AI Start-ups

Investor Perspective: The VC View on India's AI Start-up Ecosystem

Indiaʼs AI opportunity is not about models, it is about owning workflows, distribution, and data at scale.

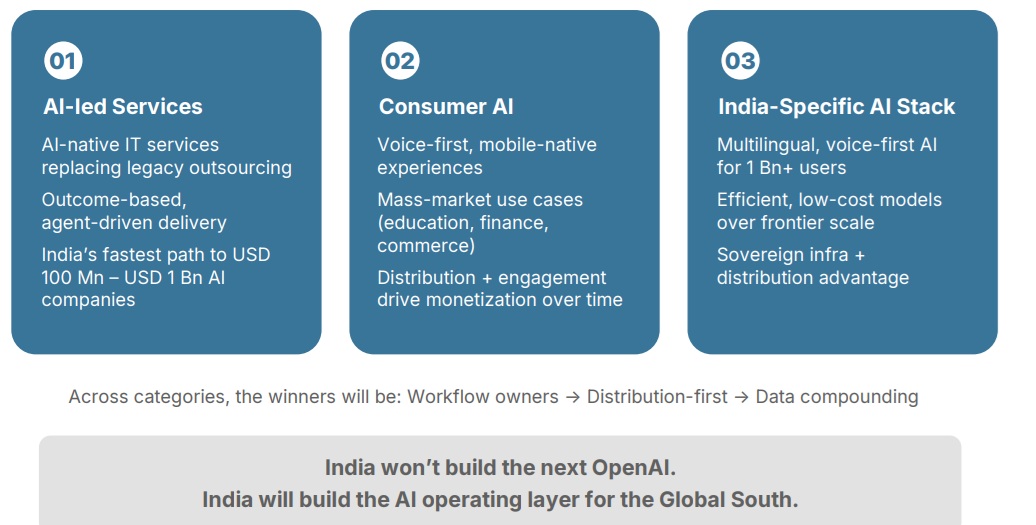

According to Aakrit Vaish Founder, Activate, At Activate, we believe Indiaʼs AI moment is being shaped by a new generation of deeply technical founders building from first principles. Through our inception investing approach, partnering with founders even before a company exists, weʼre seeing early signals across three powerful themes: Consumer AI reimagining everyday experiences, AI-led services redefining how work gets done, and Sovereign AI building Indiaʼs own foundational capabilities. Indiaʼs edge lies in its unique constraints and scale, and the most enduring companies will be those that combine world-class technology with deep local insight. We are still in the earliest innings of this transformation.

According to MR Rangaswami Founder & Chairman Indiaspora, India is no longer an emerging player in AI, it is a proving ground for how AI will be built, deployed, and scaled for the world. The 100 start-ups in this report are not riding a wave; they are shaping the contours of a new, distinctly Indian AI playbook. For investors, this is a moment to act with conviction, not caution. The easy bets in AI are already crowded and commoditizing fast. Indiaʼs real opportunity lies deeper: in backing companies that own workflows, proprietary data, and distribution in complex, high-friction markets. The application layer may dominate today, but the outsized, enduring returns will come from those who also fund the foundational stack, compute, models, and infrastructure. This is not a short-cycle trade; it is a decade-long value creation opportunity. For policymakers, incrementalism will not suffice. Indiaʼs early advantage, built on digital public infrastructure, must now be extended into sovereign AI capabilities. That means decisive investments in compute, data access, and research, alongside regulatory clarity that enables innovation while building global trust. India has done this before. It will need to do so again, faster and at greater scale. For the start-up community, the message is unequivocal: the bar has been raised. Thin wrappers and fast followers will not endure. The winners will be those who go deep, owning mission-critical workflows, building with Indiaʼs constraints in mind, and creating solutions that are, by design, hard to replicate anywhere else. This is the time to move from pilots to production, from features to platforms, and from local success to global ambition. This report captures an ecosystem that has crossed the threshold from experimentation to execution. The next phase will separate the durable from the transient. With aligned capital, bold policy, and founder ambition, India is not just participating in the AI revolution, it is positioning itself to lead it.