Spikes In Global Energy Prices Via Many Channels; Global growth remained resilient but below its historical average, with AI-driven investment and accommodative financial conditions somewhat offsetting tariff and geopolitical headwinds.

FinTech BizNews Service

Mumbai, April 8, 2026: Monetary Policy Report APRIL 2026 has been published today by the RBI. The report is published under Section 45ZM of the Reserve Bank of India Act, 1934:

Global growth remained resilient but below its historical average, with AI-driven investment and accommodative financial conditions somewhat offsetting tariff and geopolitical headwinds. Renewed inflation risks, driven by energy prices and volatile financial markets impart greater uncertainty to the global macroeconomic and financial outlook. Amidst heightened uncertainty and volatile capital flows, domestic financial markets fluctuated intermittently in the second half of 2025-26. System liquidity remained in surplus during H2. Money market rates evolved largely in sync with system liquidity and monetary policy actions. A combination of domestic and global cues hardened long-term government bond yields and rendered equity markets volatile.

The depreciation pressures in INR accentuated at the tail end of H2, breaching its previous record lows amidst concerns over West Asia conflict. While bank credit growth continued to improve and remained supportive of real economic activity, financing from non-bank sources also increased. Transmission of the policy rate to both lending and deposit rates continued in H2 and remained robust during the current easing cycle, albeit with some frictions.

In recent months, the combination of sustained credit demand and persistent gap between credit and deposit growth prompted banks to increase their term deposit rates, in addition to resource mobilisation through certificate of deposits, to bridge the funding gap. Domestic economic activity also remained resilient in the second half of 2025–26, primarily driven by private consumption, supported by both rural and urban demand, GST rate rationalisation and monetary easing. Structural reforms, favourable financial conditions and government’s thrust on infrastructure spending aided investment activity.

On the supply side, services remained buoyant, and manufacturing strengthened, although agricultural activity moderated due to weather disruptions. The underlying momentum in economic activity, buoyed by further progress on trade deals with major economies, bodes well for India’s overall growth outlook.

Global headwinds from geopolitical tensions, volatile commodity prices and supply-chain disruptions pose downside risks to the outlook. Specifically, intensification of the West Asia conflict could strain input supplies to various downstream sectors that may be growth inhibiting.

Headline inflation in India increased from historical low levels seen in October 2025 but remained below the target thereafter. The pick-up in inflation was driven by the food group where the waning of base effects led to a turnaround from deflation. Fuel group inflation remained moderate and core inflation remained contained barring precious metals. Major methodological changes brought about by the introduction of the new series have significant implications for inflation, such as higher food group inflation and lower core. The realised cost conditions: input costs, wage costs, and margins showed no major pressures up to February 2026.

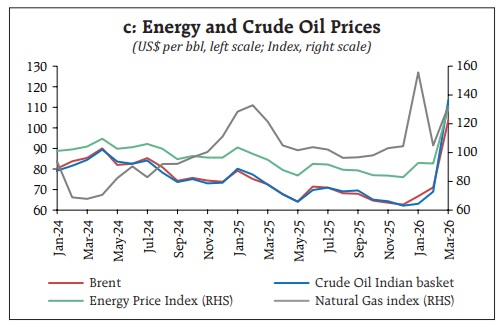

Contribution of imported inflation, however, has been rising and imported input cost pressures have accentuated in March. The impact of conflict-driven spikes in global energy prices is also likely through multiple channels. Going forward, India’s macroeconomic outlook remains resilient despite elevated geopolitical tensions and lingering global trade frictions. Strong fundamentals, including sustained growth, low inflation, and fiscal consolidation, provides India the wherewithal to withstand the adverse impact of heightened global uncertainties.

The surge in global crude oil prices since the West Asia conflict, exacerbated by significant supply disruptions, have tilted risks to inflation on the upside and growth on the downside, which have been communicated through asymmetric fan charts, scenario, and sensitivity analysis. In navigating through these turbulent times, monetary policy in India will continue to focus on reinforcing price stability while remaining growth supportive.