Artificial Intelligence is perceived as the most disruptive development likely to reshape banking operations: FICCI-IBA Bankers’ Survey

FinTech BizNews Service

Mumbai, April 19, 2026: The twenty-first round of the FICCI-IBA Bankers’ Survey captures industry sentiment for the outlook period January to June 2026. A total of 24 banks, comprising Public Sector Banks, Private Sector Banks, Foreign Banks, Small Finance Banks, and Cooperative Banks, participated in this round.

The survey was conducted at a time when India’s macroeconomic environment is in a healthy phase with headline inflation of around 2.75% in January 2026 under the revised data series with GDP growth registering approximately 7.8% in Q3 of FY 2025-26. India’s banking sector continues to demonstrate resilience, supported by improved asset quality, strengthening capital buffers, robust retail and SME credit momentum, and early signs of revival in private capital expenditure. Against the backdrop of heightened geopolitical uncertainties, alongside evolving global liquidity conditions and steady domestic growth consolidation, the survey offers timely insights into credit outlook, sectoral credit demand dynamics, emerging risk perceptions, and the strategic priorities shaping the banking ecosystem.

Summary of Survey Findings

The survey results suggest that the banking sector maintains a broadly constructive outlook on credit growth over the near term, supported by improving balance sheets, steady economic activity, and sustained demand across multiple segments of the economy. Most respondents expect the current monetary policy stance to remain broadly stable in the coming months, indicating a view that the existing policy framework remains appropriately calibrated to balance growth and inflation considerations.

Expectations regarding overall credit expansion remain positive, with banks anticipating continued momentum in non-food credit. Public Sector Banks appear particularly confident in the outlook, reflecting improved asset quality, stronger capital positions, and increasing traction in corporate lending. Private Banks demonstrate a balanced and selective approach to credit growth, while Foreign Banks display moderate optimism consistent with their focused exposure to corporate and institutional segments.

Sectorally, credit demand from services and retail segments is expected to remain a key driver of overall lending growth. The services sector outlook reflects strong expectations of expansion, supported by activity in real estate, financial services, logistics, and tourism-related industries. Retail lending is also projected to remain robust, reinforcing its role as a central pillar of banking sector growth.

SME credit demand is expected to remain particularly strong, with respondents expressing high confidence in continued expansion in this segment. This reflects improving business activity among smaller enterprises, increased formalization of credit channels, and continued policy emphasis on supporting MSME growth.

In contrast, industrial credit growth is expected to expand at a more measured pace, reflecting a gradual recovery rather than a sharp acceleration. The outlook suggests steady investment activity led by infrastructure development, manufacturing-linked sectors, and government-led capital expenditure. Term loan demand is expected to be largely driven by infrastructure, real estate, auto and auto components, pharmaceuticals and emerging sectors such as data centres and defence-related industries.

Working capital demand, by contrast, appears more closely linked to trade cycles and operational financing requirements. Sectors such as textiles, automobiles, pharmaceuticals, engineering goods, and food processing are expected to drive industrial working capital borrowing, while services-related working capital demand is likely to be led by wholesale and retail trade, transport operators, tourism, and hospitality.

The survey also highlights several structural shifts shaping the banking landscape. Artificial intelligence is widely perceived as the most disruptive development likely to reshape banking operations in the near term, particularly in areas such as credit underwriting, risk assessment, and collections. Competition and collaboration with fintech and Big Tech platforms are also viewed as significant forces influencing the future banking business model.

From a strategic perspective, banks increasingly prioritize climate risk management and financial inclusion as key focus areas for the coming year, reflecting the sector’s growing engagement with sustainability and inclusive finance agendas. At the same time, traditional priorities such as credit growth, asset quality management, and digital transformation remain important components of banks’ strategic planning.

The findings further underscore the growing prominence of sustainable finance opportunities, with renewable energy financing emerging as the segment perceived to have the strongest growth potential. This aligns with the broader transition toward green investments and India’s long-term energy transition objectives.

Finally, the survey highlights cybersecurity risk as the most pressing challenge confronting banks today, reflecting the increasing digitalization of financial services and the need for stronger technological resilience.

Overall, the survey paints a picture of a banking sector that is reasonably optimistic about credit growth while simultaneously preparing for structural changes driven by technology, sustainability imperatives, and evolving competitive dynamics. The outlook suggests continued expansion in credit demand, supported by services activity, retail lending, and SME financing, alongside a gradual revival in investment-led sectors of the economy.

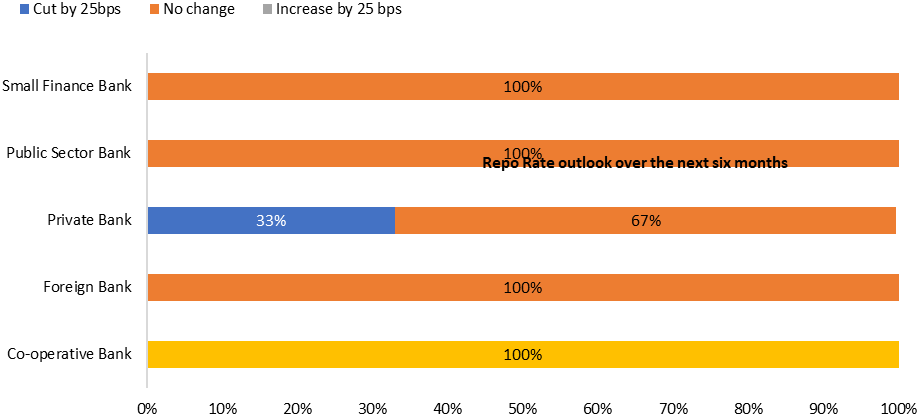

Repo Rate outlook over Jan’26 - Jun’26

The survey indicates a strong consensus toward maintaining current policy rates, with most banking segments expecting no immediate change. Small Finance Banks, Public Sector Banks, and Foreign Banks unanimously anticipate a status quo. Private Banks show a mild easing bias, while Cooperative Banks uniquely signal expectations of a rate increase.

Small Finance Banks, Public Sector Banks, and Foreign Banks report a unanimous (100%) expectation of no change in policy rate. Private Banks also largely align with this view, with 67% anticipating a status quo, while 33% expect a 25-basis point rate cut. In contrast, Cooperative Banks stand out, with 100% of respondents expecting a 25-basis point rate increase.

Overall, the results suggest that market participants view the current monetary policy stance as appropriately calibrated, with limited anticipation of near-term shifts.

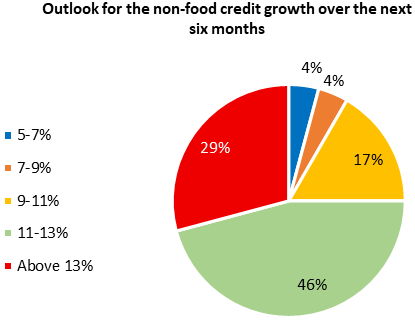

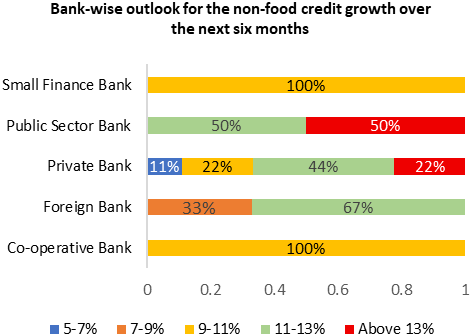

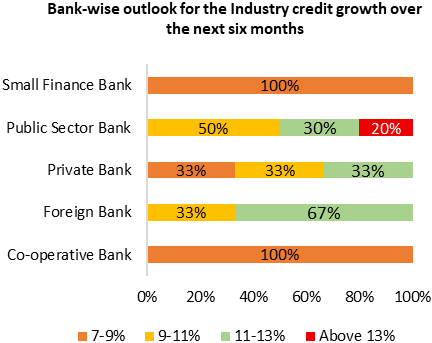

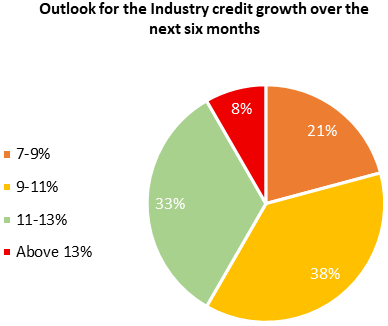

The aggregate distribution of responses indicates that 46% of participants expect overall non-food credit growth in the 11%-13% range, making it the dominant view. A further 29% anticipate growth above 13%, while 17% expect growth in the 9%-11% range. Only 8% of respondents foresee growth below 9%, evenly split between the 5%-7% and 7%-9% categories.

Small Finance Banks and Cooperative Banks largely cluster in the 9%-11% growth range, reflecting relatively conservative expansion expectations.

Public Sector Banks display stronger confidence, with expectations split between the 11%-13% and above 13% categories. This suggests optimism anchored by improved asset quality, strengthened capital buffers, and continued traction in corporate lending, particularly amid signs of capex revival.

Private Banks show a more diversified distribution of responses, though the majority are concentrated in the 11%-13% and above 13% growth bands. This indicates a selective but growth-oriented approach, supported by robust retail portfolios, MSME lending momentum, and calibrated corporate exposure strategies.

Foreign Banks predominantly expect growth in the 11%-13% range, with a smaller proportion indicating 7%-9% growth. This reflects moderate optimism, largely shaped by global liquidity conditions, capital allocation priorities, and selective participation in domestic corporate credit markets.

The survey responses indicate a moderately optimistic but calibrated outlook for industrial credit growth over the next six months, with expectations concentrated in the 9%-13% range. The results suggest that the consensus outlook is centered around mid-to-high single digit to low double-digit growth, with nearly 71% of respondents expecting growth between 9% and 13%.

While expectations are broadly positive, the relatively small proportion (8%) projecting growth above 13% indicates that respondents do not foresee a sharp acceleration in industrial credit. Instead, the outlook reflects steady and gradual expansion, likely supported by ongoing capex revival, infrastructure push, and sectoral demand recovery.

Segment-wise responses indicate clear variation in expectations across bank categories. Small Finance Banks and Cooperative Banks are largely clustered in the 7%-9% growth range, reflecting relatively conservative outlooks on industrial credit expansion, possibly due to limited exposure to large industrial borrowers and a stronger orientation toward retail and MSME lending.

Public Sector Banks exhibit comparatively stronger optimism, with expectations largely concentrated in the higher growth bands, particularly within the mid-to-upper growth ranges. A significant share of respondents anticipates double-digit expansion, reflecting confidence in sustained credit momentum.

Private Banks present a more diversified outlook, with expectations spread across the lower to mid growth ranges. This distribution indicates a balanced and calibrated approach to credit expansion, combining selective growth strategies with continued emphasis on risk management and asset quality.

Foreign Banks are primarily concentrated in the mid growth band, suggesting moderate confidence in the trajectory of industrial credit growth while maintaining a measured lending stance.

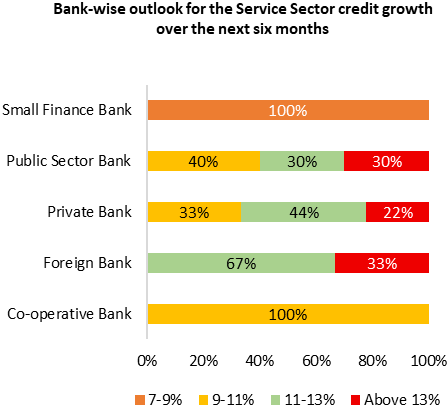

The survey responses indicate a strongly optimistic outlook for credit growth to service sectors, with expectations skewed toward double-digit expansion and a meaningful proportion anticipating acceleration above 13%.

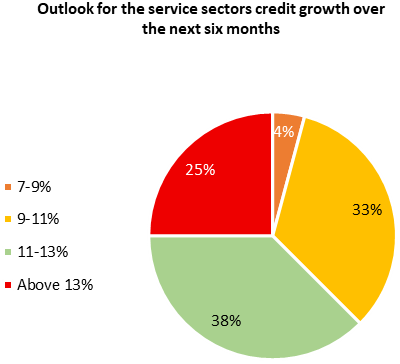

The response pattern suggests a broadly positive outlook for credit growth to the services sector, with expectations largely concentrated in the higher growth bands. The largest share of respondents anticipate expansion in the mid double-digit range, followed by a sizeable segment expecting growth in the lower double-digit range. A further group projects even stronger expansion, indicating a meaningful degree of optimism regarding credit demand from services. Only a very small proportion foresee growth in the lower band, implying that downside expectations remain limited and that the overall outlook for service-sector credit is firmly anchored in double-digit territory.

Across bank groups, expectations reflect distinct portfolio orientations and risk appetites.

Small Finance Banks are clustered in the lower growth band, indicating a relatively cautious outlook. This likely reflects their higher exposure to MSME-driven service segments and sensitivity to localized demand dynamics. Cooperative Banks are concentrated in the moderate growth band, suggesting steady but measured optimism consistent with their community-based lending model and strong orientation toward SMEs and small service enterprises.

Public Sector Banks exhibit expectations spanning from moderate to higher growth ranges, reflecting confidence in a broad-based recovery in service-sector credit demand supported by their diversified sectoral exposure. Private Sector Banks display a balanced distribution across the higher growth bands, indicating a growth-oriented stance while maintaining portfolio diversification across service sub-segments.

Foreign Banks are largely concentrated in the higher growth ranges, with a smaller share expecting even stronger expansion, pointing to relatively strong confidence in credit momentum within the service sector.

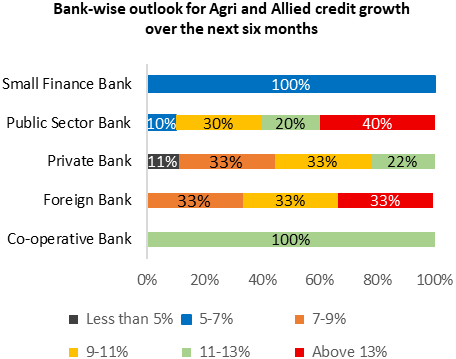

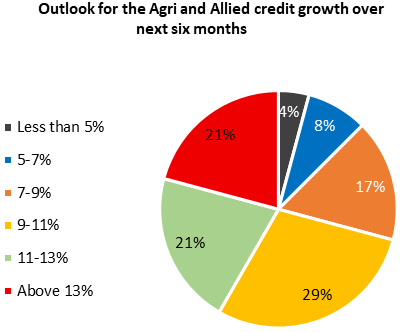

The survey responses indicate a moderately positive but measured outlook for agriculture and allied sector credit growth, with expectations concentrated in the 9%-13% range and a meaningful share anticipating growth above 13%. The distribution of responses indicates that 29% of respondents expect y-o-y growth in agriculture and allied credit to fall in the 9%-11% range, making it the largest share. A further 21% anticipate growth in the 11%-13% band, while 21% expect expansion above 13%, reflecting a meaningful degree of optimism. Meanwhile, 17% project growth in the 7%-9% range, and only 4% foresee growth below 5%, suggesting that downside expectations remain limited and the overall outlook is anchored in moderate to strong expansion.

Co-operative Banks show a strong concentration in the 11%-13% growth band (100%), indicating robust optimism.

Public Sector Banks display expectations spanning moderate to higher growth ranges, with a notable concentration in the upper bands. The presence of respondents anticipating stronger expansion alongside those projecting moderate growth reflects a balanced yet relatively confident outlook on credit to the agriculture sector.

Private Banks show expectations largely centered around the lower to mid growth ranges, with fewer respondents anticipating stronger expansion. This distribution suggests a measured and selective approach to agricultural credit growth, balancing expansion opportunities with prudent risk management.

Foreign Banks’ expectations are similarly concentrated in the moderate growth ranges, with a segment anticipating stronger expansion. This pattern points to cautious optimism, likely reflecting their relatively limited direct exposure to primary agriculture and a greater focus on lending to agri-linked corporates and supply chains. Small Finance Banks are concentrated in the lower growth band, indicating a relatively conservative outlook.

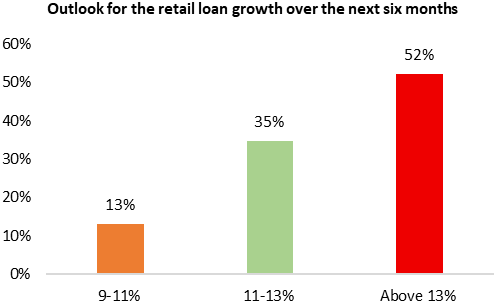

Outlook for the retail loan growth:

The survey responses indicate a strongly optimistic outlook for retail loan growth, with expectations heavily skewed toward high double-digit expansion. The distribution of responses indicates that 52% of respondents expect y-o-y retail loan growth to be above 13%, making it the dominant view. A further 35% anticipate growth in the 11%-13% range, while 13% expect expansion in the 9%-11% band. Notably, there are no responses projecting growth below 9%, underscoring broad-based confidence in retail credit momentum and reinforcing the perception that retail lending will remain a key driver of overall credit growth in the near term.

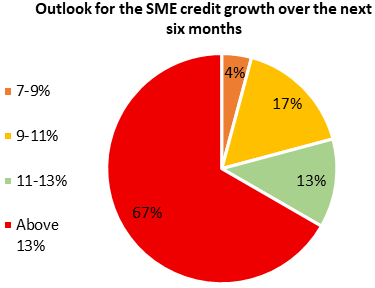

Outlook for the SME credit growth:

The survey responses indicate a highly optimistic outlook for SME credit growth, with a dominant expectation of strong double-digit expansion over the next six months. The distribution of responses points to a strongly optimistic outlook for SME credit growth, with the majority of respondents expecting expansion in the highest growth band. A further segment anticipates growth in the upper mid-range, while a smaller share projects moderate expansion. Only a very limited proportion of respondents expect growth in the lower band, and notably none foresee expansion below that level. Overall, the pattern of responses underscores strong confidence in sustained and robust momentum in SME credit demand over the next six months.

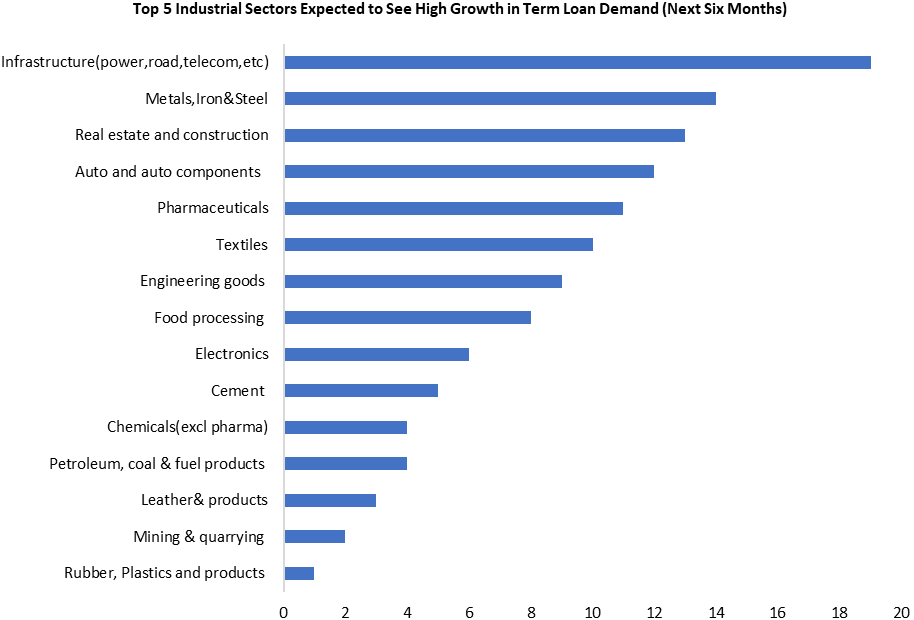

The responses indicate that Infrastructure (including power, roads, and telecom) is expected to witness high growth in demand for term loans over the next six months, followed by Metals, Iron and Steel, Real Estate and Construction. Auto and auto components, Pharmaceuticals, Textiles, and Engineering Goods, also feature prominently among the top sectors anticipated to see increased borrowing activity. Other sectors such as Chemicals (excluding pharma), Leather and Leather Products, and Rubber and Plastics received comparatively fewer mentions.

In addition, respondents highlighted Power, Ports, Defence, and Data Centres as other key sectors with expected high growth in demand for term loan over the next six months.

The outlook for term loan demand over the next six months appears capex-heavy and infrastructure-led, with strong support from real estate and manufacturing-linked sectors. The responses reflect optimism around investment-led growth rather than consumption-driven sectors.

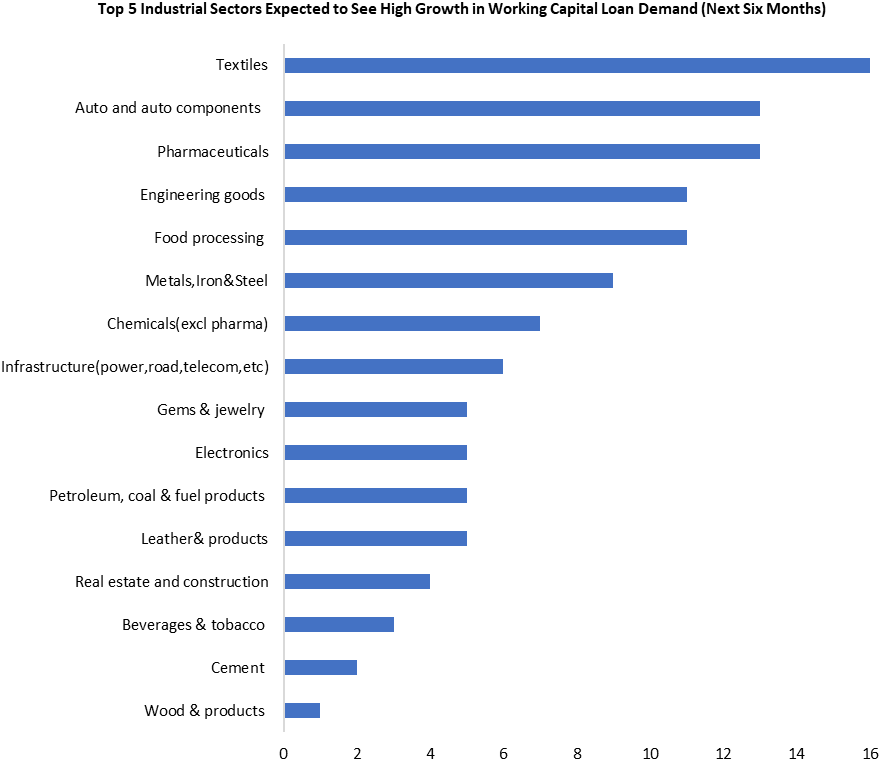

The responses indicate that Textiles is expected to witness high growth in working capital loan demand over the next six months. This is followed by Auto and Auto Components and Pharmaceuticals, which received an equal number of responses. Engineering Goods and Food Processing complete the top five sectors anticipated to see strong growth in working capital requirements.

Other sectors that also received notable mentions include Metals, Iron & Steel, Chemicals (excluding pharma), and Infrastructure (power, roads, telecom, etc.), though at comparatively lower levels. Sectors such as Gems & Jewellery, Electronics, Petroleum, Coal & Fuel Products, Leather & Products, and Real Estate & Construction received moderate responses, while Beverages & Tobacco, Cement, and Wood & Products were cited even less frequently. In addition, respondents highlighted Defence as other key sector with expected high growth in demand for Working Capital loan over the next six months.

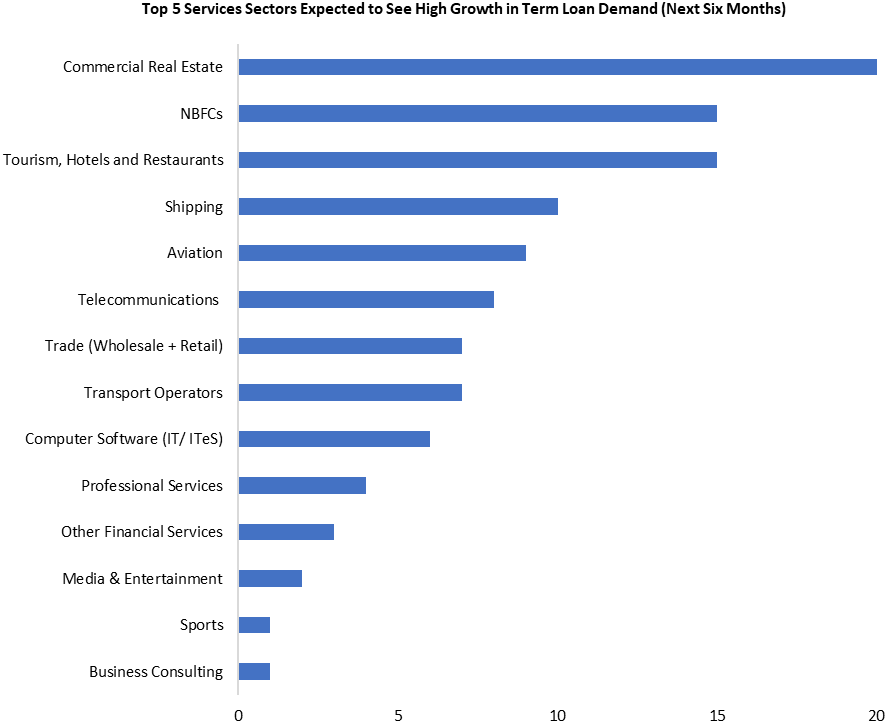

The responses indicate that Commercial Real Estate is expected to see high growth in term loan demand over the next six months, receiving the maximum number of mentions. This is followed by NBFCs and Tourism, Hotels and Restaurants, which are tied as the next most cited sectors. Shipping and Aviation also feature prominently among the leading sectors anticipated to witness increased borrowing activity.

Other sectors receiving notable responses include Telecommunications, Trade (Wholesale & Retail), Transport Operators, and Computer Software (IT/ITeS). Comparatively fewer mentions were recorded for Professional Services, Other Financial Services, Media & Entertainment, Sports, and Business Consulting.

Respondents also highlighted Data Centre/AI-related services, Warehousing, Logistics and Renewable Energy & EV-related segments as other key sectors with high term loan demand.

The outlook suggests that term loan demand in services will be asset-heavy and expansion-driven, led by commercial real estate and financial intermediation (NBFCs), with continued recovery momentum in tourism and logistics-linked sectors. Asset-light service industries, by contrast, show limited near-term capex demand.

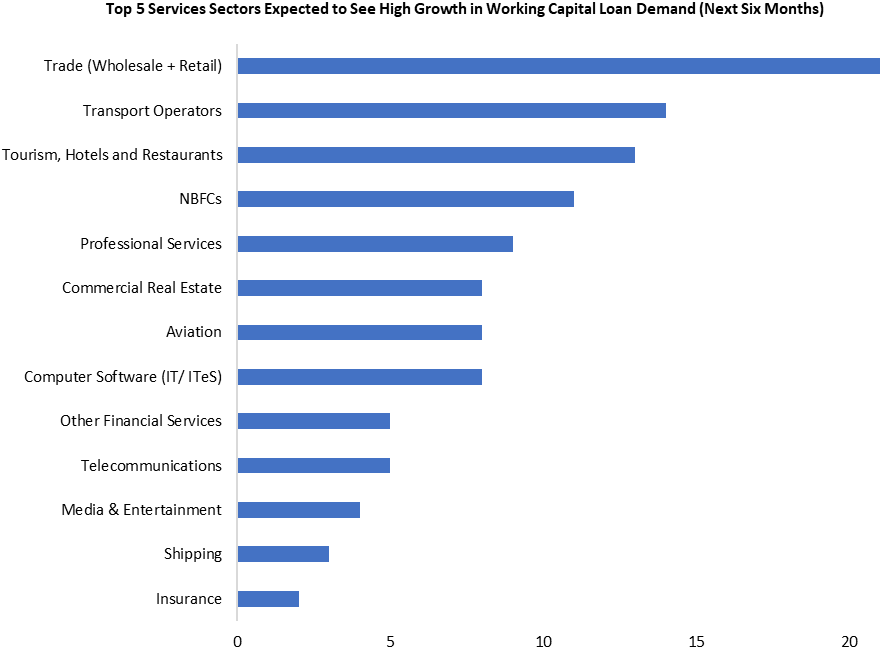

The responses indicate that Trade (Wholesale & Retail) is expected to witness high growth in working capital loan demand over the next six months. This is followed by Transport Operators and Tourism, Hotels and Restaurants, which also received strong mentions. NBFCs and Professional Services complete the top five services sectors anticipated to see increased demand for working capital financing.

Other sectors receiving notable responses include Commercial Real Estate, Aviation, and Computer Software (IT/ITeS). Comparatively fewer mentions were recorded for Other Financial Services, Telecommunications, Media & Entertainment, Shipping, and Insurance.

Respondents also identified Construction, Defense-related services, Logistics and Healthcare as key sectors with anticipated high demand for working capital loans over the next six months,

Unlike term loan demand (which was more asset-expansion driven), working capital demand in services appears trade- and mobility-led, driven by consumption cycles, logistics, and hospitality activity. The pattern suggests short-term liquidity needs linked to operating cycles rather than large infrastructure or asset acquisition investments.

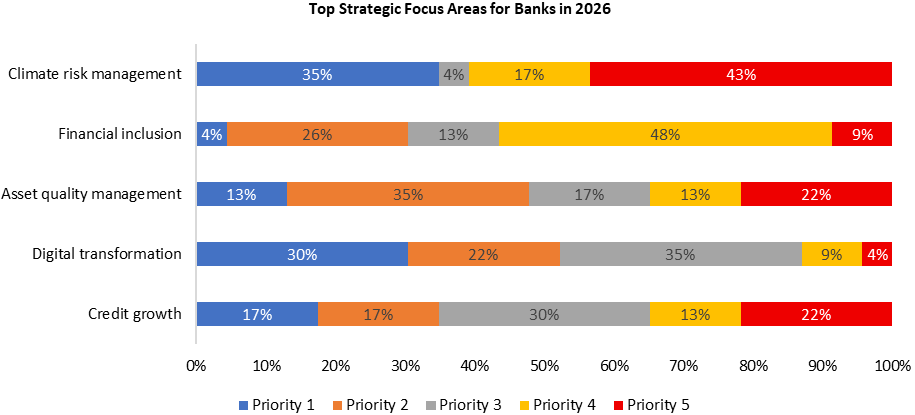

The survey responses indicate that Climate Risk Management and Financial Inclusion emerge as the highest strategic priorities for banks in 2026, with the largest share of respondents assigning them the top rankings. Climate Risk Management received the highest proportion of top-priority rankings, followed closely by Financial Inclusion.

Asset Quality Management and Credit Growth reflect a more balanced distribution across priority levels, indicating they remain important but are not uniformly viewed as the top-most focus areas.

Digital Transformation shows a relatively mixed ranking pattern, with a significant proportion assigning it mid-level priority (Priority 3), while a smaller share ranked it as the highest priority.

Overall, the results suggest a strategic tilt toward sustainability and inclusion-focused themes, alongside continued attention to core risk and growth management areas.

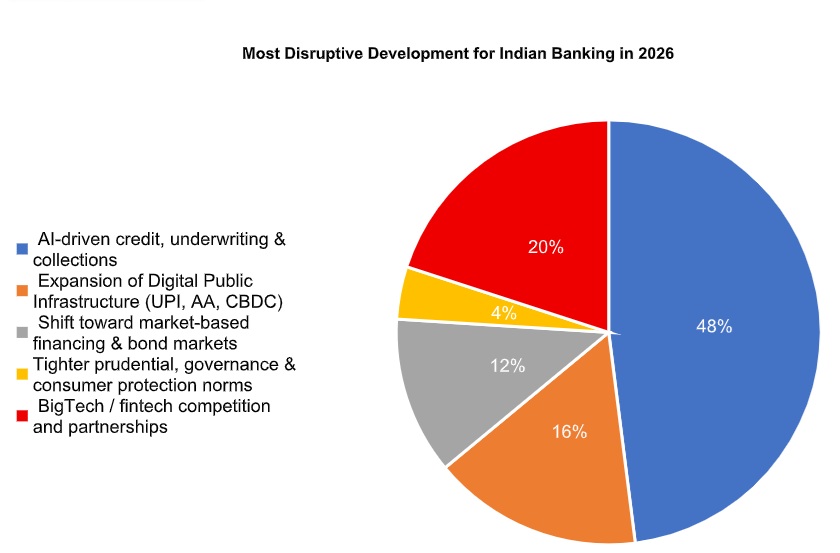

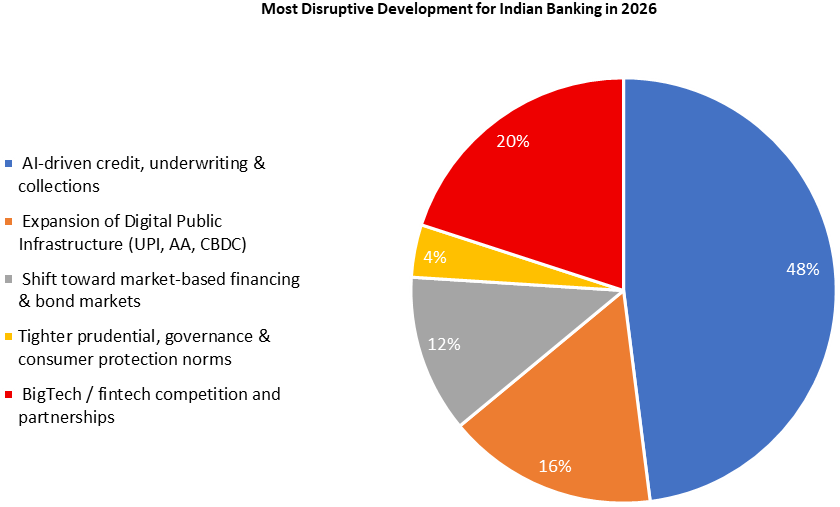

The survey responses indicate a clear consensus that AI-driven credit, underwriting, and collections (48%) will have the greatest disruptive impact on the Indian banking business model in 2026. Nearly half of respondents selected this option, underscoring the expectation that artificial intelligence will fundamentally reshape risk assessment, customer onboarding, fraud detection, pricing models, and recovery mechanisms. This suggests that technological disruption is viewed not merely as incremental improvement, but as structural transformation of core banking operations.

The second most cited factor is BigTech / fintech competition and partnerships (20%), highlighting concerns around platform-based ecosystems, embedded finance, and digital-first customer acquisition models. This reflects the growing influence of technology firms in financial intermediation and the need for banks to either compete or collaborate strategically.

Expansion of Digital Public Infrastructure (UPI, AA, CBDC) (16%) ranks third, indicating recognition of India’s evolving digital rails as a major structural enabler of new business models, data-driven lending, and seamless payment ecosystems.

A smaller share of respondents point to a shift toward market-based financing and bond markets (12%), suggesting moderate expectations of disintermediation from traditional bank lending. Finally, only 4% anticipate tighter prudential, governance, and consumer protection norms as the primary disruptive force, indicating that regulatory tightening is seen as evolutionary rather than transformational.

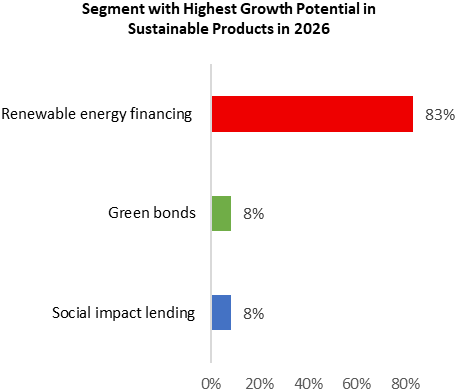

Segment with Highest Growth Potential in Sustainable Products:

The survey results clearly indicate that Renewable Energy Financing (83%) is overwhelmingly perceived as the segment with the highest growth potential in sustainable products. An overwhelming majority of respondents selected this category, signaling strong conviction that energy transition financing will dominate sustainable banking opportunities in the near term.

In comparison, both Green Bonds (8%) and Social Impact Lending (8%) received relatively limited responses. This suggests that while these segments are acknowledged as important components of sustainable finance, they are not viewed as primary growth engines relative to renewable energy financing.

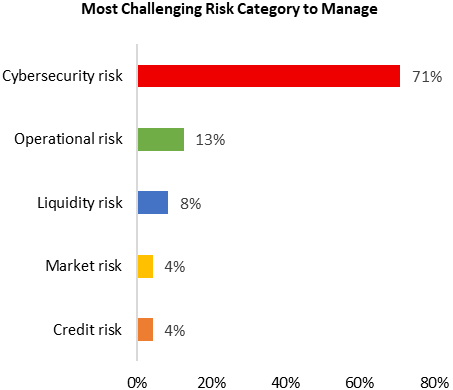

Most Challenging Risk Category to Manage:

The survey responses clearly identify Cybersecurity Risk (71%) as the most challenging risk category currently facing banks. With an overwhelming majority selecting this option, cybersecurity stands out as the dominant concern, significantly outpacing all other risk categories.

In comparison, Operational Risk (13%) ranks a distant second, followed by Liquidity Risk (8%), while both Market Risk (4%) and Credit Risk (4%) are perceived as relatively less challenging at present.