BCG-FICCI-IBA Report: Indian Banking Sector Must Grow 3-3.5 P.P. To Realize Viksit Bharat Mission

FinTech BizNews Service

MUMBAI, August 25, 2025: Boston Consulting Group (BCG) in association with FICCI and Indian Banks’ Association has released a report titled “Charting New Frontiers”. The report emphasizes that India is at a critical inflection point in its development trajectory, where the next two decades could transform today’s momentum into sustained global leadership. Realizing its ambitious ‘Viksit Bharat Mission’ will hinge on the evolution of a robust, innovative, and resilient banking and financial sector, capable of supporting India’s aspirations for sustainable, inclusive growth.

Mr. Ruchin Goyal, Managing Director and Senior Partner at BCG

For India to meet its Viksit Bharat targets, banking assets need to grow at 3.0–3.5 percentage points faster than its nominal GDP. Currently, economies and their banking sector operate in a complex, multipolar world with volatile trade flows, shifting supply chains and geopolitical risks.

The combined disruption of AI/ GenAI and shifting consumer expectations is unfolding at a scale never seen in the last few decades.

The Indian banking industry is poised to reach for leadership – it is profitable, well capitalized and

highly valued. The report highlights that it will need to seize this opportunity by charting new

frontiers:

Mr C S Setty, Chairman of Indian Banks’ Association,

1) Unlocking credit growth

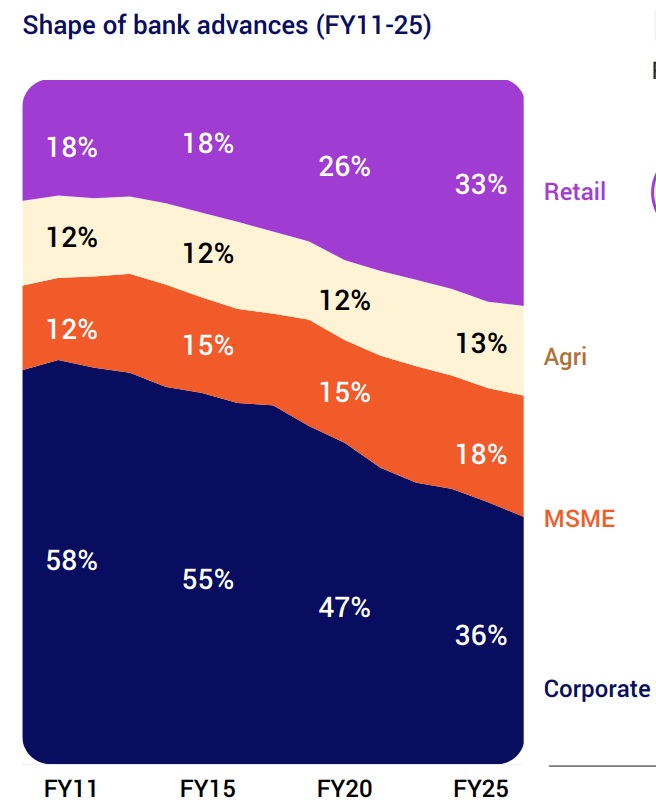

The bank lending mix has changed significantly over the last 14 years, with share

of corporate advances dropping from 58% to 36%.

Corporate funding has moved away from banks, towards capital markets and

alternate funding avenues (e.g., Private credit). Within bank funding, the mix is

shifting towards short-term working capital compared to long term capex.

NTC retail lending is at an all-time low – at this rate, universal credit penetration

will take more than a decade. Historical performance shows that well-under written

NTC loans can perform at par with ETC customers, indicating room to expand

responsibly.

Financial inclusion efforts on MSME lending shows promise. Formalization efforts

(e.g., Udyam, GST), proliferation of digital payments (UPI, QR codes) and

enhanced coverage through guaranteed schemes have driven a high share of

NTC lending among MSMEs.

Lenders need to embrace the full power of data, including alternate data, and AI

capabilities to manage and measure new, emerging risks (e.g., fraud, climate).

For India to achieve its long-term Viksit Bharat ambitions, the corporate sector will play a key

role. Banks must re-engage in corporate credit, especially in infrastructure, manufacturing, and

renewables that will define the nation’s future. At the same time, resilience has to be embedded

as a core business priority, from managing climate risk to strengthening cyber defenses and

operational continuity. The ability of our banking system to fund growth while safeguarding

stability will be central to India’s journey toward a Viksit Bharat says Jyoti Vyij, Director

General, FICCI.

2) Driving productivity

The Indian banking industry's opex to assets ratio has risen by 26 bps over the

past 14 years, a trend that is opposite to the rest of the world.

Despite a decade of digitization, real productivity gains have been limited, with

only about 1% annual improvement over the past 15 years after adjusting for

inflation and capacity growth.

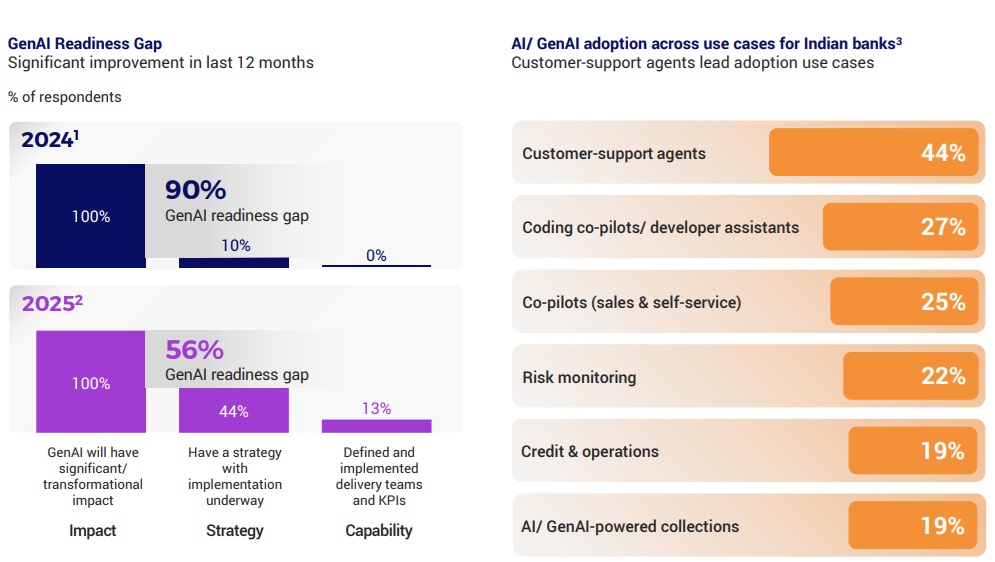

AI/ GenAI promises transformational capabilities. With mature deployment, 35-

40% of current low value activities can be automated.

AI/ GenAI programs have to be business led, enabled by engineering teams.

3) Digital maturity

Non-bank (especially UPI) apps are perceived to be more user friendly and

intuitive. However, customers still prefer to use their banks for loans and

investments.

The challenge with banks is that their digital journeys involve a lot of friction and

adoption issues. AI/ GenAI can enable seamless journeys and personalization

with conversational and agentic journeys.

DPI 2.0 aims to achieve more complex use cases — consent management and

lending. It will need to be designed in a manner that will enable as frictionless

transactions as with DPI 1.0.

ULI has the potential to create a UPI-like explosion in lending. Regulators,

Government and Financial Services sector, all will need to work together to build

access and digital registries to enable this (e.g., digital land records).

Mr C S Setty, Chairman of Indian Banks’ Association, said, “India’s Digital Public

Infrastructure has revolutionized access through Aadhaar, UPI, and Jan Dhan, and the next

frontier lies in DPI 2.0 platforms like Account Aggregator and Unified Lending Interface (ULI). To

unlock their full potential, banks must go beyond transactions and deliver seamless, end-to-end

digital experiences to the customers that combine trust, simplicity, and omni-channel support

leveraging GenAI as well. By doing so, banks can deepen inclusion, strengthen customer

relationships, and create a truly world-class digital banking ecosystem.”

4) Embedding resilience:

Banks need to move beyond credit risk and manage emerging macro risks, e.g.,

climate, cyber and geo-political risks.

Shared industry utilities such as NPCI, credit bureaus have done well to raise the

standards of all participants in the financial sector.

The Banking sector will benefit from creating new utilities for emerging risks like

climate finance and transaction monitoring.

Mr. Ruchin Goyal, Managing Director and Senior Partner at BCG, and a co-author of the

report, said, ‘‘India’s banks have delivered strong performance in recent years, but to truly power

the Viksit Bharat mission they must grow 3–3.5 percentage points faster than nominal GDP. The

sector has a unique opportunity to unlock the next wave of growth by leveraging alternate data

and DPI 2.0 to bring millions of new-to-credit households and MSMEs into the formal lending

system. At the same time, banks must move beyond incremental productivity gains and use

GenAI for a step-change—rewiring core processes, redeploying capacity to higher-value

activities, and setting new global benchmarks for efficiency. If they act decisively, banks won’t just

support the mission—they’ll become the very engine of Viksit Bharat.”

India’s banking sector is well-positioned but must accelerate transformation across growth,

productivity, digital maturity, and resilience to meet its Viksit Bharat ambitions. Simultaneously,

there is a need to expand into untapped credit segments, unlock productivity with AI/ GenAI,

deliver world class digital experiences, and embed a deep risk culture. Only then can banks

become the driving force behind India’s economic rise.

A joint push by industry participants, government, and regulators will be critical to this journey.

Key actions:

Banks to leverage alternate data for underwriting and build capabilities to manage

emerging risks.

Regulators to provide greater flexibility to banks in providing corporate credit and promote

world class utilities for Climate, Cyber and Fraud risks like NPCI, Credit Bureau.

Government to fast-track implementation of DPI 2.0 and standardize KYC norms across

financial products.