Most Banks Still Trading Below Fair Values; MSME portfolios likely to be vulnerable in a prolonged slowdown

FinTech BizNews Service

Mumbai, 26 June 2026: The latest Kotak Institutional Equities report on Banks states that banks’ ability to raise adequate FCNR/foreign currency borrowings, which would reduce the pressure on the cost of funds, could act as key trigger points for re-rating the sector.

Tying the near-term investment argument

We are in an interesting juncture in the cycle where re-rating is likely to be driven by yield discipline (public banks) and improved access to lower-cost of borrowings (FNCR deposits). Asset quality should remain resilient, supported by strong retail vintages and stable corporate balance sheets, while MSME risks appear contained with policy support. Valuations remain attractive despite recent outperformance, with scope for multiple expansion and earnings compounding. We have a relative preference for frontline private banks alongside SBI among public sector lenders.

Actions from two key players drive the investment argument

We believe that actions by public banks related to driving loan yields higher that provide the tailwind for other players to operate with a bit more freedom and banks’ ability to raise adequate FCNR/foreign currency borrowings, which would reduce the pressure on the cost of funds, could act as key trigger points for re-rating the sector. We do acknowledge that the benefits could be partly offset based on banks’ decisions to pursue growth. We are a bit skeptical about the loan demand situation and believe that the strong flow of foreign funds is likely to reduce the cost of funds as it would lower demand for deposits than boost loan growth. Recent disclosures from the RBI suggest that the growth can be explained more by credit substitution from bond markets rather than an increase in demand.

Asset quality should hold up well in FY2027 as well

We believe that asset quality is unlikely to be a concern in the near term. We expect public and private banks to report lower slippages, though banks could increase coverage for ECL transition. Retail asset quality is entering the current phase from a significantly stronger starting point versus FY2023 and pre-Covid vintages, aided by tighter underwriting since FY2024 and the seasoning of weaker cohorts. Unsecured lending should see the sharpest improvement following prior stress. MSME portfolios may be relatively vulnerable in a prolonged slowdown, though systemic stress is currently not evident, with guarantee schemes such as ECLGS and CGTMSE providing meaningful risk mitigation. Large corporate balance sheets remain resilient, with lenders comfortable supporting drawdowns, despite near-term sectoral uncertainties.

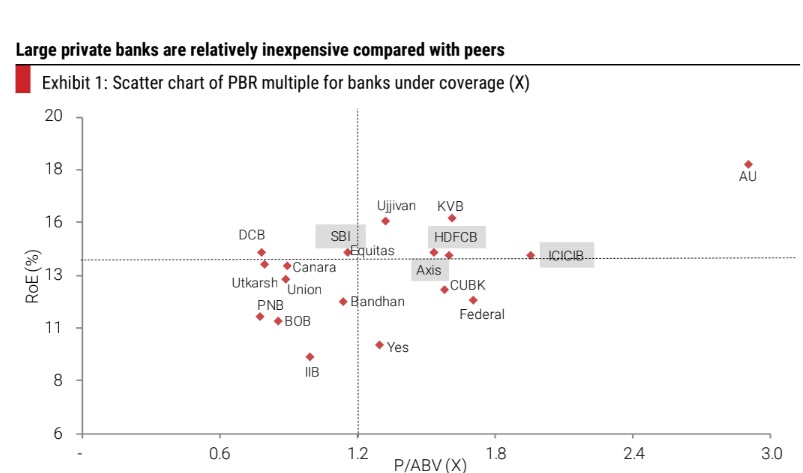

Valuations are comfortable to remain positive on frontline banks

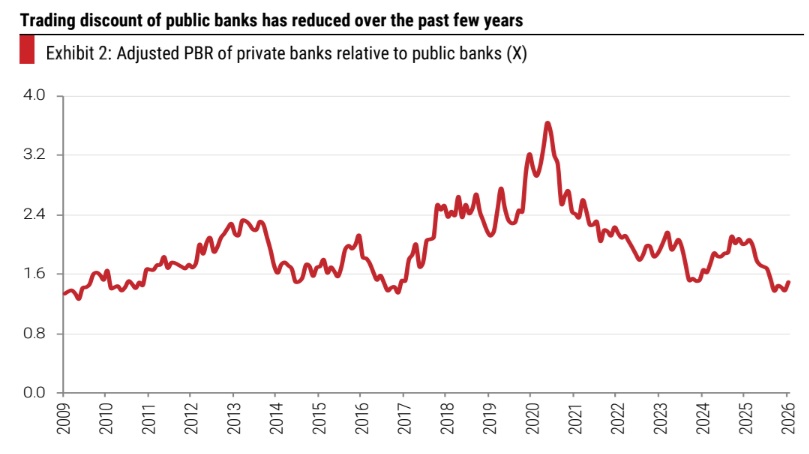

Valuations remain compelling, despite recent outperformance, with most banks still trading below our fair values. We see scope for multiple expansion alongside steady earnings compounding. Within this context, we maintain a relative overweight stance on frontline private banks. We favor HDFC Bank and ICICI Bank at current levels, while Axis Bank needs to demonstrate improved franchise performance relative to peers to justify a premium over HDFC Bank. Although benign asset quality trends and a supportive funding environment could warrant higher risk-taking, current valuations appear to adequately reflect this upside. Among public sector banks, SBI remains our preferred exposure.