RBI foreign currency reserves increased by $4.4 bn during the fortnight, indicating the desire of RBI to also recoup foreign exchange reserves; There is strong market confidence in top-rated NBFCs, allowing them to borrow more cheaply short-term than states can borrow long-term

FinTech BizNews Service

Mumbai, July 12, 2026: The State Bank of India’s Economic Research Department has come out with a research report, authored by Dr. Soumya Kanti Ghosh, Group Chief Economic Adviser, State Bank of India:

Latest fortnightly bank deposit numbers reveal a surge indicating buoyancy in capital flows aided by recent RBI and Government of India measures...CP and Bank credit have both expanded indicating economic growth has potentially surprised on the upside in Q1FY27.

Overall deposits within the banking system jumped by around Rs 7 lakh crores for the fortnight ended 30th June 2026, third highest fortnightly growth in 29-years. Netting out the quarter end deposit mobilization, we believe that the surge is also on account of a potential jump in capital flows because of FCNR(B), ECB and OFCB.. India has also received $7 bn FII inflows since the measures announced by the Government to bring the foreign inflows and boost the rupee. Cumulative Debt FAR inflows amount to $2.7 bn since then

• An informed guess of the magnitude of overall capital flows stripping out the trend growth indicates that this number could be ~$15 bn. FCNR(B) flows have picked up pace

• Separately, RBI foreign currency reserves increased by $4.4 bn during the fortnight, indicating the desire of RBI to also recoup foreign exchange reserves…

• Long tenor G-sec yields rallied faster than corporate bond yields in May and June, supported by foreign inflows and stronger sovereign bond demand, with corporate yields being sticky amid continued liquidity demand, credit and duration premium demand by investors.. Meanwhile, 3-year AAA saw better demand with low duration risk and relatively contained supply pressure, with issuers partly shifting to CPs, Bank loans and short tenor funding

• CP issuances increased in Q1FY27 with June issuances at 55 month high. Meanwhile, incremental bank credit also showed higher growth indicating the economy has continued to expand meaningfully in Q1FY27..Top sectors with higher CP issuances in Q1 has also showed higher bank credit growth. Moreover, these sectors account for 69% of the new projects announcement in Q1

• Rupee also appreciated around 2.2% till June-end from its lowest level of Rs 96.8 per US dollar on 20 May 2026. However, the recent heightened geo-political tensions after the US President remarks on NATO and ending of the US-Iran ceasefire has led to increase in Brent crude price and depreciation in the Rupee (-0.4%). But its outlook remains positive with average crude oil price for Indian basket now expected at $80 bn or lower leading to savings of at least $30 to $35 bn in oil import bill against our previous estimate when oil price had crossed $130/bbl.

Record-High Deposits Accumulation & Accretion to Foreign currency reserves for Fortnight ending 30 June 2026

Fortnight ended Change in Deposits

31 March 2026 Rs 12.17 lakh crore

31 December 2025 Rs 7.25 lakh crore

30 June 2026 Rs 6.97 lakh crore

THIRD HIGHEST in 29 Years.

Reasons

1. Quarter ending Impact of around Rs 3.5-4 lakh crore

2. Substantial amount of flows primarily due to FCNR (B), portfolio flows, ECB & OFCB: Overall capital flows could be hypothetically around ~ $15 bn

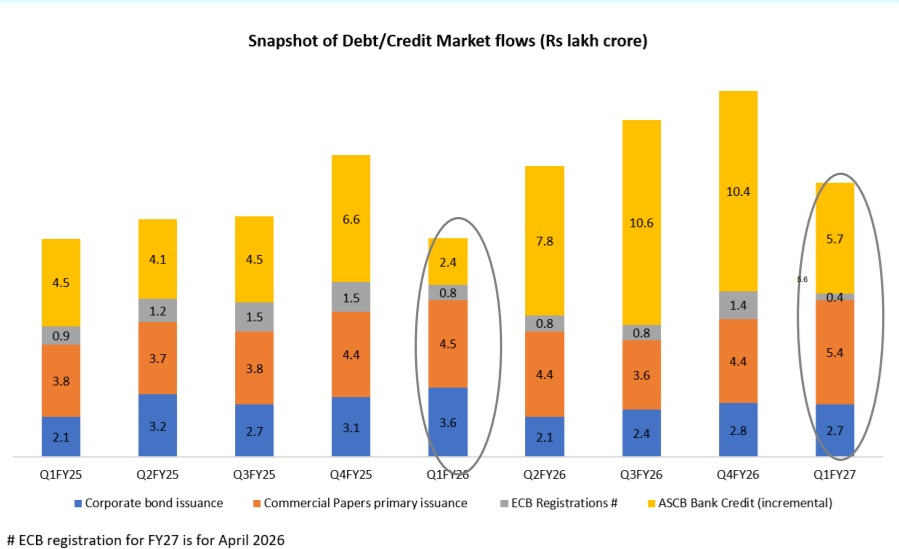

CP issuances & bank credit both have risen in Q1FY27 compared to Q1FY26

Bank Credit and CP Issuances moving in the same direction – indicating economic resilience

Corporates are resorting to higher short-term borrowings through Commercial paper, with Q1 FY27 issuances rising 19% yoy. Meanwhile, incremental bank credit too rising to Rs 5.6 lakh crore in Q1 FY27 compared to Rs 2.4 lakh crore in Q1 FY26

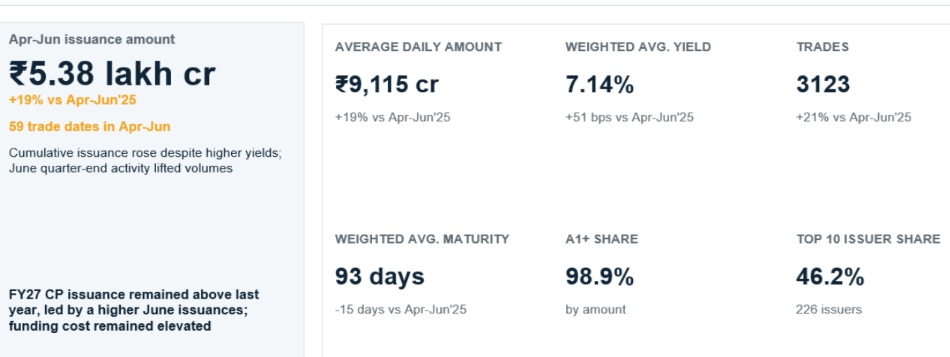

CP Issuances Q1 FY27

Apr-Jun FY27 issuances were Rs5.38 lakh cr, +19% YoY; June highest monthly issuances since Nov’21, with WAY at 7.14%.

Apr-Jun FY27 issuances were Rs5.38 lakh cr, +19% YoY; June highest monthly issuances since Nov’21, with WAY at 7.14%.

Monthly activity & Tenor Mix in CP market

June issuance rose +85% MoM to Rs2.55 lakh crore; number of trades rose +34% as quarter-end funding demand picked up Q1 FY27 remained concentrated in 62–91D CP (73.9%), but the share was lower than Q1 FY26 (81.4%); short-tenor buckets rose while 272– 366 D share reduced in Q1 FY27 Maturity wall is front-loaded: Of Rs 5.42 lakh crore outstanding, Rs 4.11 lakh crore (76%) is maturing in Jul-Sep

Top sectors with CP issuances also showed high bank credit growth

Top 10 industries with highest CP issuances in Q1 FY27 include Broking & Financial institutions, NBFC, oil & gas, textile, HFC, Steel, Power, Telecom, Real Estate and Cement. Bank credit to these sectors (except telecom) has shown higher growth. Meanwhile, project announcements in these sectors account for ~69% of the announcements in Q1 FY27, with Rs 6.5 lakh crore alone for Nuclear power projects

Comparative Short-term rates- CP WAY higher than 3M CD rate and 91D T-bill, but its spread from WALR has reduced

Spread between CP WAY and Bank WALR has reduced

The spread between CP WAY and 91D T-bill has increased to 200 bps in June 2026 from 140 bps in March 2026 and 87 bps in June 2025. Meanwhile, CP WAY spread from bank lending rate has reduced to 115 bps in May 2026 from 169 bps in March 2026 and 230 bps from a year ago period

Corporate Bond spread over G-Sec has been rising over the longer tenure

Long tenor G-sec yields rallied faster than corporate bond yields in May and June, supported by foreign inflows and stronger sovereign bond demand, with corporate yields being sticky amid continued liquidity demand, credit and duration premium demand by investors. Meanwhile, 3-year AAA saw better demand with low duration risk and relatively contained supply pressure, with issuers partly shifting to CPs, Bank loans and short tenor funding

10-year AAA corporate bond yield remained elevated at 7.7% (average) in June 2026. With 10-year G-sec at 6.9%, the spread has now reached 81 bps, same as in March 2026

Banks have been borrowing through CDs and this trend is likely to reverse

Surplus system Liquidity has moderated Bank borrowings through CDs increased 32% yoy in Q1 FY27 to Rs 3.37 lakh crore from Rs 2.55 lakh crore a year ago. Meanwhile WAY increased to 6.9% compared to 6.4%. But the liquidity situation has also started changing recently. With record deposits boost of Rs 7 lakh crore in the fortnight ended, liquidity is likely to become comfortable!

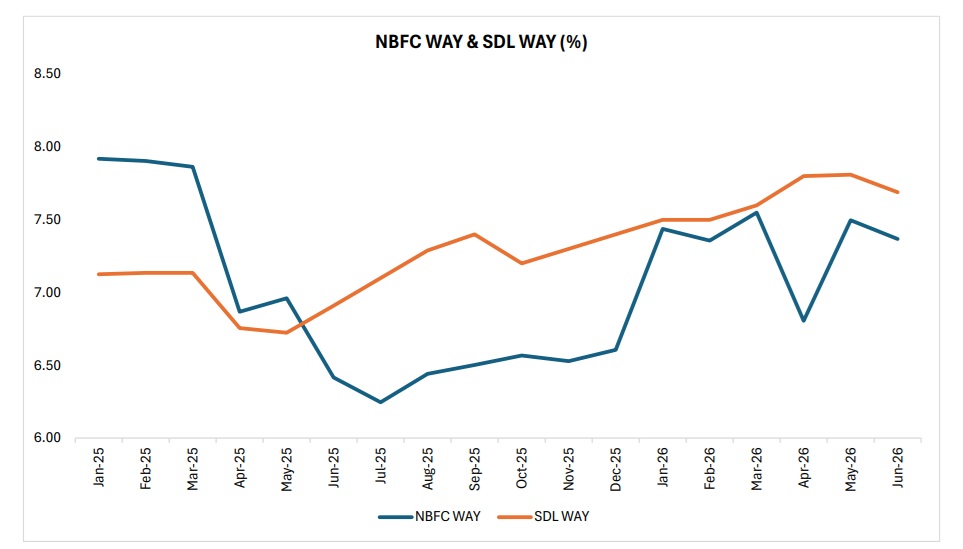

NBFCs are borrowing at lower cost through CP than State Government market borrowing WAY.. Spread has narrowed

NBFCs are borrowing at lower rate than the SDL WAY since June 2025, indicating surplus short-term banking liquidity combined with high structural. It shows strong market confidence in top-rated NBFCs, allowing them to borrow more cheaply short-term than states can borrow long-term

FII inflows turned positive after recent Government measures

India has received $7.0 bn FII inflows since the measures announced by the Government to bring the foreign inflows and boost the rupee. Cumulative Debt FAR inflows amount to $2.7 bn since then

Rupee gained more than 2% till end-June from its lowest on 20 May

Rupee has appreciated around 2.2% till Juneend from its lowest level of Rs 96.8 per US dollar on 20 May 2026 However, recent increase in geo-political tensions have again put upward pressure on the exchange rate

The increase in geo-political uncertainty in the recent days amid the US President remarks on NATO and ending of the US-Iran ceasefire has led to increase in Brent crude price and depreciation in the Rupee (-0.4%)

However, outlook for Crude oil is still positive

Average crude oil price for Indian basket is now expected at ~$80/bbl which will lead to savings of $30 to $35 bn in oil import bill against our previous estimate when oil price crossed $130/bbl