As per estimates; states would lose Rs 0.8 lakh crore if Centre’s excise duty is reduced to nil, keeping all else same. However, higher oil prices will benefit states by around Rs 30,000 crore, so the net impact of excise duty cut on states revenue would be Rs 50,000 crore.There is a need for a comprehensive policy on balance of payments

FinTech BizNews Service

Mumbai, 16 May 2026: The State Bank of India’s Economic Research Department has come out with a special research report on the “RUPEE”, authored by Dr. Soumya Kanti Ghosh, Group Chief Economic Adviser, State Bank of India.

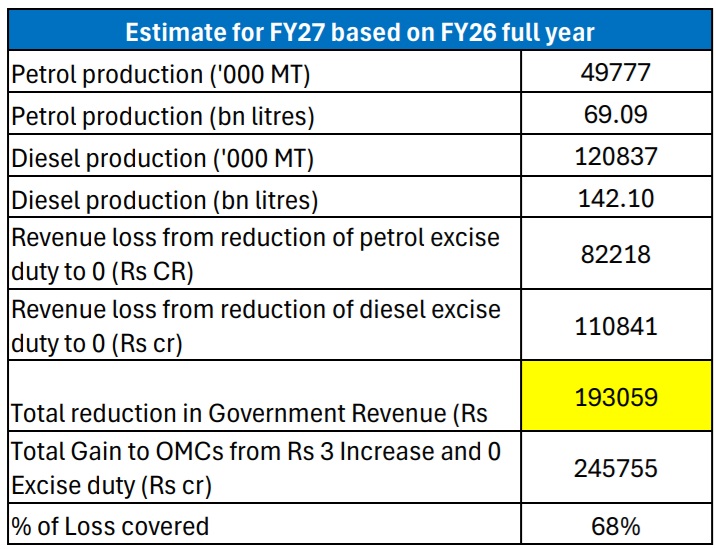

Retail fuel price has been hiked by Rs 3 per litre in order to reduce the losses incurred by the OMCs owing to unchanged fuel prices amidst rising Brent Crude price. OMC’s under recoveries on sales of petrol and diesel are soaring because of unchanged retail prices. As per the Union Minister OMCs are incurring losses to the tune of Rs 1000 crore per day which amounts to around Rs 3.6 lakh crore a year. The current increase in oil price by Rs 3 is likely to provide relief of Rs 52,700 crore in OMCs under recoveries, which is 15% of the expected total loss of the OMCs in FY27.

The measure is not likely to have much impact on oil consumption as historical data shows that hike in petrol and diesel price has been followed by decline in consumption immediately after the hike, only to recover thereafter with no decline visible in the annual consumption levels. Further, immediate impact on CPI inflation is likely around 15-20 bps in MayJune 2026. So, we revise our FY27 forecast to 4.7%. There is no direct impact of this hike on the fiscal situation.

Notably, the Government has earlier reduced the excise duty earlier by Rs 10 on diesel and petrol during the year to help the OMCs for which the revenue loss for the Centre is estimated as Rs 1.1 lakh crore. In a similar way if we assume that the excise duty is further rationalized to zero to help OMCs reduce their losses, it would entail a revenue loss of Rs 1.9 lakh crore or 0.5% of the GDP for the Government. The states will also loss Rs 80,000 crore.

However, further rupee depreciation can exhaust all these gains by increasing the $ price of crude import. Our calculations show that, even an additional depreciation of Rs2 in the rupee (from FY27 current average at Rs 94 stays put) raises the effective crude oil price pushing the landed import cost which fully offsets the gains from the current fuel price hike. Thus, the rupee has already approached a critical depreciation threshold, beyond which further currency weakness could substantially erode the intended benefits of domestic fuel price revisions. Meanwhile, as per the latest IEA report crude will continue to remain under pressure owing to the depleting inventories. Assuming flows through the Strait gradually resume from June, IEA projects global oil supply to decline by 3.9 mb/d on average in 2026, to 102.2 mb/d. Meanwhile, world oil demand is forecast to contract by 420 kb/d y-o-y in 2026, to 104 mb/d, 1.3 mb/d less than the pre-war forecast.

RETAIL FUEL PRICE HIKED BY RS 3/LITRE

Petrol diesel price has been hiked by Rs 3 per litre in order to give relief to the oil marketing companies which were incurring losses owing to higher brent crude price. OMC’s under recoveries on sales of petrol and diesel are soaring because of unchanged retail prices. As per the Union Petroleum minister, in the current quarter the under-recoveries are around Rs 1.98 lakh crore. Meanwhile, OMC’s are incurring losses to the tune of Rs 1000 crore per day which amounts to around Rs 3.6 lakh crore a year. The current increase in oil price by Rs 3 is likely to provide relief of Rs 52,300 crore in OMCs under recoveries, which is 15% of the expected total loss of the OMCs in FY27.

IMPACT ON CONSUMPTION & INFLATION

The historical data shows that hike in petrol and diesel price is followed by decline in consumption immediately after the hike but it recovers thereafter with no decline visible in the annual consumption levels.

Further, immediate impact on CPI inflation is likely around 15-20 bps in May-June 2026. FY27 inflation forecast is accordingly revised to 4.7%.

There is no direct impact of this hike on the fiscal situation.

IF OIL EXCISE DUTY IS REDUCED TO ZERO

If we assume that the Government reduced the excise duty on petrol and diesel to zero from its current level of 11.9% and 7.8% respectively, it will lead to reduction in government revenue/gain of OMCs to the tune of Rs 1.9 lakh crore. This might increase fiscal deficit by 0.5% of GDP, if the government doesn’t reduce the expenditure.

Thus the overall loss of the government from excise duty cut in the current fiscal including the net loss calculated earlier of Rs 10 duty cut in March would amount to Rs 3 lakh crore.

Meanwhile, 15% of the OMCs loss would be covered by increase in retail price by Rs 3 and 53% with reduction in oil excise duty to nil.

Furthermore, our estimates suggest that states would lose Rs 0.8 lakh crore if Centre’s excise duty is reduced to nil, keeping all else same. However, higher oil prices will benefit states by around Rs 30,000 crore, so the net impact of excise duty cut on states revenue would be Rs 50,000 crore.

BRENT CRUDE AND EXCHAGE RATE VOLATILITY STARTS CONVERGING...

We computed volatility using rolling standard deviations of monthly percentage changes in the Indian basket crude oil prices and the USD/INR exchange rate. Our results show a high degree of convergence between the two volatility series in recent times especially after the Iran War, with a correlation coefficient of 0.53, indicating a substantial co-movement between crude oil and exchange rate volatility.

This suggests that fluctuations in global crude oil markets are increasingly being transmitted into the domestic exchange rate environment.

RUPEE HAS EXHAUSTED ITS LIMIT OF BEING A SHOCK ABSORBER…

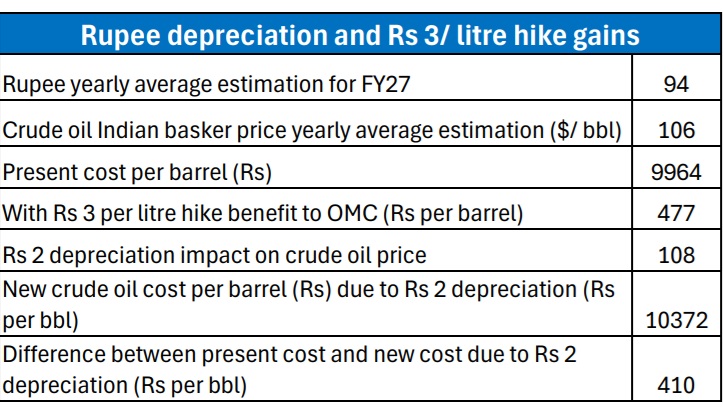

We calculate the threshold level of rupee depreciation beyond which the gains accruing to OMCs from the recent Rs3 per litre fuel price increase are effectively neutralized by the rising cost of crude oil imports.

Assuming an average FY27 exchange rate of Rs94/USD and an average Indian basket crude oil price of $106 per barrel, the present landed crude cost works out to nearly Rs9,964 per barrel. The Rs3 per litre increase provides an estimated benefit of around Rs477 per barrel to OMCs.

However, even an additional depreciation of Rs2 in the rupee raises the effective crude oil price pushing the landed import cost which fully offsets the gains from the fuel price hike.

Thus, the rupee has already moved beyond a critical depreciation threshold, beyond which further currency weakness could substantially erode the intended benefits of domestic fuel price revisions.

BRENT CRUDE AND IEA PROJECTION

The Brent Crude has been under pressure hovering around $107/bbl. The closure of Strait of Hormuz amidst the West Asia was has reduced the shipments crossing through the Strait significantly. The shipments through the Strait have declined to 14.6 million barrels per day (mb/d) in Q1 2026 from an average of 20 (mb/d) of crude oil and oil products were shipped in 2025. Meanwhile, LNG supply through Strait of Hormuz which was average of 10.85 billion cubic feet per day in 2025 reduced to 7.3 billion cubic feet per day in Q1 2026.

As per the latest IEA report crude will continue to remain under pressure owing to the depleting inventories. Global oil supply declined by a further 1.8 mb/d in April to 95.1 mb/d, taking total losses since February to 12.8 mb/d.

Assuming flows through the Strait gradually resume from June, IEA projects global oil supply to decline by 3.9 mb/d on average in 2026, to 102.2 mb/d. Meanwhile, world oil demand is forecast to contract by 420 kb/d y-o-y in 2026, to 104 mb/d, 1.3 mb/d less than the pre-war forecast.