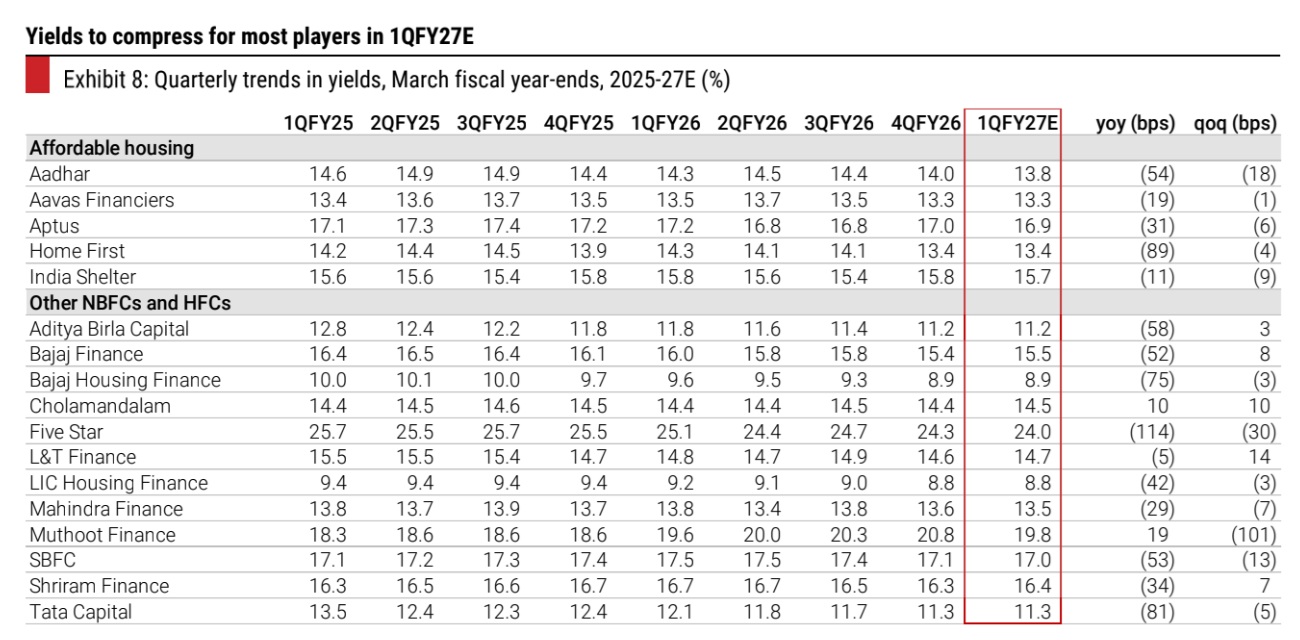

Most NBFCs will likely report healthy NIM expansion (9-80 bps yoy; some compression in Bajaj Housing, Five Star and SBFC), accelerating NII growth over AUM growth.

FinTech BizNews Service

Mumbai, July 6, 2026: The Kotak Institutional Equities has come out with a research report on Diversified Financials.

Let the good times roll

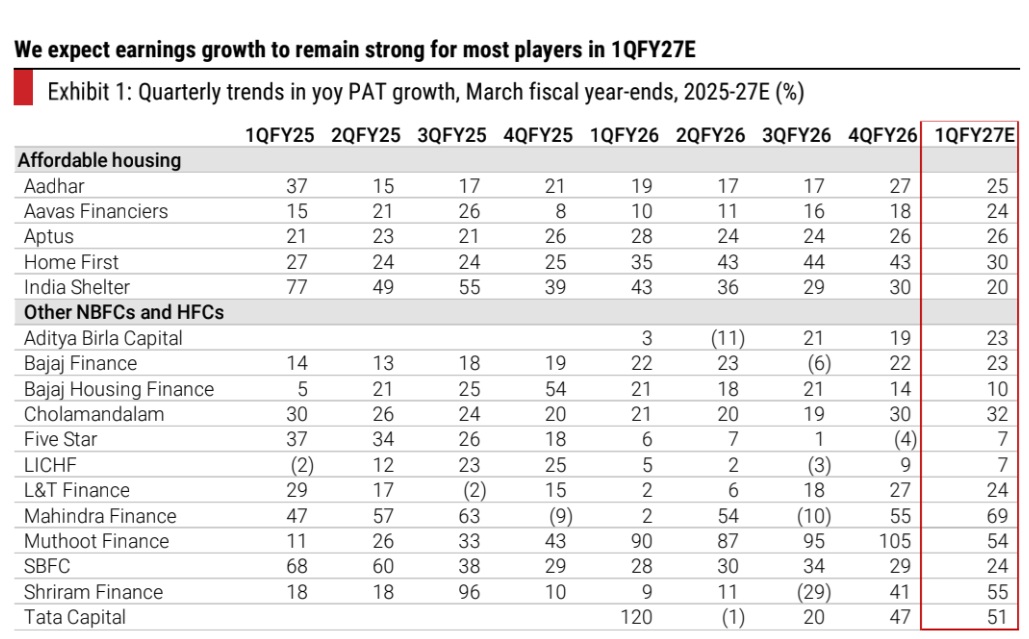

We expect most non-banks under coverage to deliver strong earnings with 22-58% core PBT growth/12-69% earnings growth in 1QFY27E, driven by healthy growth prints, stable asset quality defying seasonal weakness and yoy NIM expansion on a base of higher borrowing costs last year. With improving liquidity and easing overhang on fuel prices, we expect positive commentary and an upgrade in guidance.

All caps on a roll

While escalation of the West Asia war and fears of inflation dominated investors’ mindshare for most of 1QFY27, we expect NBFCs, large caps and mid-caps, diversified and monoline, to deliver a strong quarter. Channel checks and business releases to date suggest exceptionally strong demand/growth during the quarter across most segments—personal loans, vehicles, MSME, affordable housing, MFIs, etc.; even CVs have seen mom improvements toward the end of the quarter.

NIM—positive for the quarter

Most NBFCs will likely report healthy NIM expansion (9-80 bps yoy; some compression in Bajaj Housing, Five Star and SBFC), accelerating NII growth over AUM growth. Notably, borrowing cost has likely declined by 22-90 bps yoy for most players over the last four quarters; the benefit of lower exit cost of borrowings is driving NIM expansion in 1QFY27. Yields have contracted 5-80 bps yoy but likely inched up qoq for most NBFCs, except affordable HFCs that recently cut benchmark rates. While the incremental cost of funds was up toward the end of the year, the same softened by June 2026, with a rally in bond markets. Going forward, increase in MCLR by banks (5-10 bps in select buckets) will weigh on margins. With comfortable liquidity, we expect competitive intensity to remain intense, which will put pressure on asset yields. Fee income growth has been strong, partially fueled by strong disbursements and insurance fees; the impact of impending insurance commission guidance also needs to be monitored.

Asset quality strong

We pen down a stable/yoy decline in credit cost for most players. Collections in 1Q typically tend to be seasonally weak. This year, 1Q trends are similar to 4Q, with marginal seasonal weakness. Notably, many NBFCs have also created buffers in 4Q. Against this backdrop, we expect 5-35 bps yoy reduction in credit costs for most players, further boosting earnings.

Retain positive stance

We expect NBFCs to raise guidance on growth, which was mixed last quarter due to the overhang of the West Asia war; most diversified NBFCs are firmly above 20% loan growth; expect guidance to inch up to ~25% for the larger pack. Affordable HFCs, with encouraging incremental growth trends, will likely be more assertive about growth. Concerns of a weak monsoon and food inflation will be the only outliers. . We retain positive stance on NBFCs with scope of upgrade in a strong economic environment even as stock rally in large names is reducing the upsides. We like Bajaj twins and ABCL the most, Aptus, Aadhar and Home First in the mid-caps.

Strong growth across segments

Affordable HFCs, ailing due to slowdown over the last two years, have reported early signs of improvement in 4QFY26 and we expect a pickup in momentum in FY2027E. Personal/unsecured loan is firmly back on track driving growth and supporting margins of multi-product NBFCs such as ABCL, Bajaj and Tata Capital under coverage. Vehicle OEMs have reported healthy (15-20%) volume growth across most segments and a stronger exit month, reflecting a promising 2Q; this will augur well for vehicles finance NBFCs; MMFS disbursements growth accelerated to 21% from ~11-12% last year. Gold loans, a tad tempered by changing processes (due to new regulations) and fall in gold prices, is holding on well.