AI will undoubtedly have a massive positive impact on productivity, but could also result in large-scale job disruption.

FinTech BizNews Service

Mumbai, November 7, 2025: The latest Kotak Institutional Equities - Strategy Note focuses on “AI”, authored by Sanjeev Prasad, MD & Co-Head.

HI thoughts on AI (bubble, trouble?)

We try to make sense of the purported AI bubble through an HI (an admittedly inferior) framework. Recent fall in AI stocks and global markets may or may not be the AI bubble’s end. However, AI companies’ large implied revenue and profit pools, as per their current market caps, are hard to reconcile with the limited (or even reduced) ability of humans to pay for such services

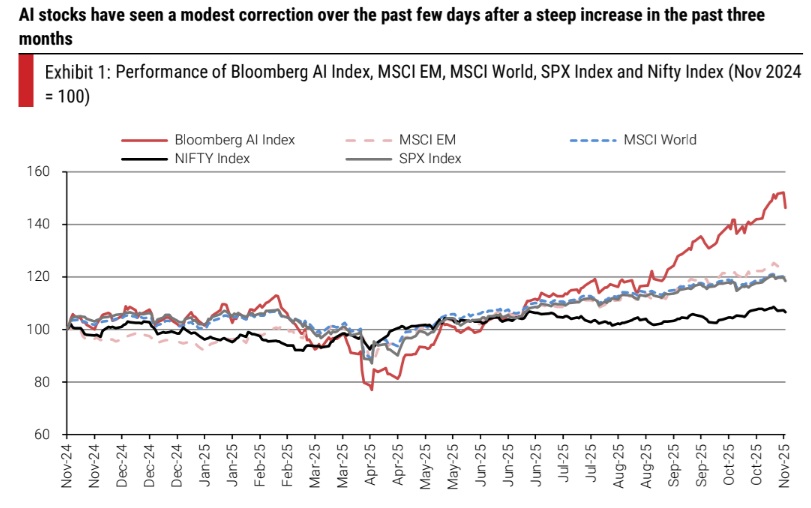

Bubble or not?

The correction in global markets and AI stocks in the past few days may or may not mark the end of the AI bubble (good, bad or ugly, only time will tell). Nonetheless, the sharp increase in the market capitalization of all sorts of AI plays (excluding certain Korean fried chicken restaurants and equipment makers) in various ‘AI-heavy’ markets would imply mind-boggling AI-related revenue and profit pools for AI companies.

Trouble for sure—consumers are workers and workers are consumers

AI will undoubtedly have a massive positive impact on productivity, but could also result in large-scale job disruption. Optimists may look at the previous technological cycle and the huge employment and productivity gains from such cycles as economies evolved from agriculture to manufacturing to services (in terms of share of jobs). Pessimists may worry about a dystopian future with machines replacing humans in mental (services) and physical (manufacturing) jobs. A simple fact of any economy is that it works on the exchange of goods and services between humans—they are both consumers and workers at the same time. A higher share of such ‘exchange’ between machines may leave workers without jobs (income) and companies without consumers (revenues).

India as an anti-AI play

The subdued performance of the Indian market over the past year on an absolute basis and relative to major DMs and EMs reflects (1) high valuations of most sectors and stocks, (2) large earnings downgrades in the past 12-15 months, although earnings seem to be stabilizing now with a decent outlook for FY2027 (see Exhibits 15-18) and (3) the lack of AI plays in India.

The incomprehensible math of AI to HI

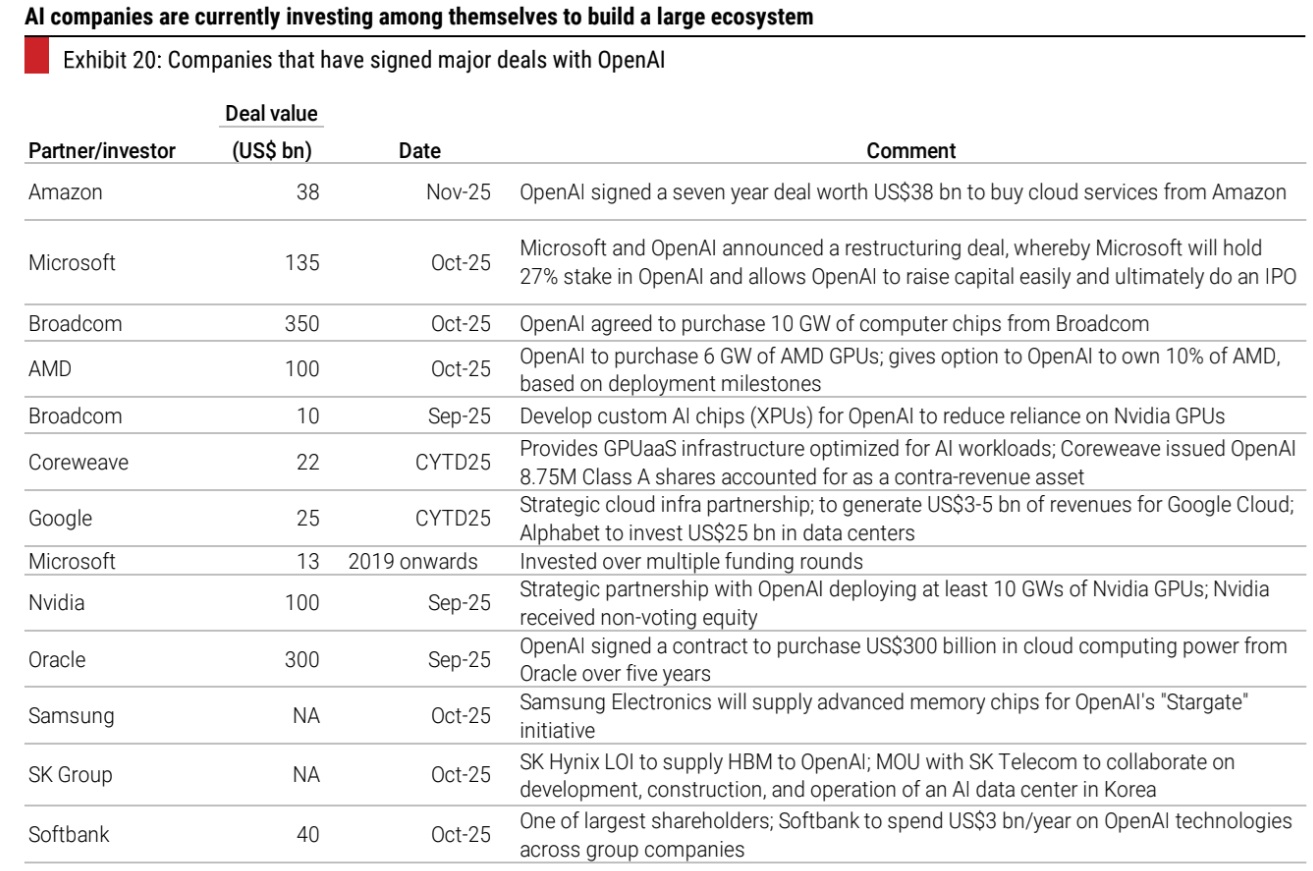

A simple back-of-the-envelope calculation of OpenAI, which is central to the AI theme, with its US$1-1.5 tn of committed investments, shows the mind-boggling implied revenue and profit pools of AI players. A 10% CRoCI on US$1-1.5 tn of investment would imply US$100-150 bn of cash return (annually). OpenAI could achieve US$200-250 bn of annual revenues if 800 mn-1 bn users were to pay US$20 per month fees. At present, OpenAI has around 40 mn paying subscribers out of its 800 mn subscribers. It expects to reach US$100 bn of revenues by 2027. We would note that there are several such competing AI services; the world has around 8 bn people and many may not require or may not be able to pay the US$20 monthly fee for any AI service.