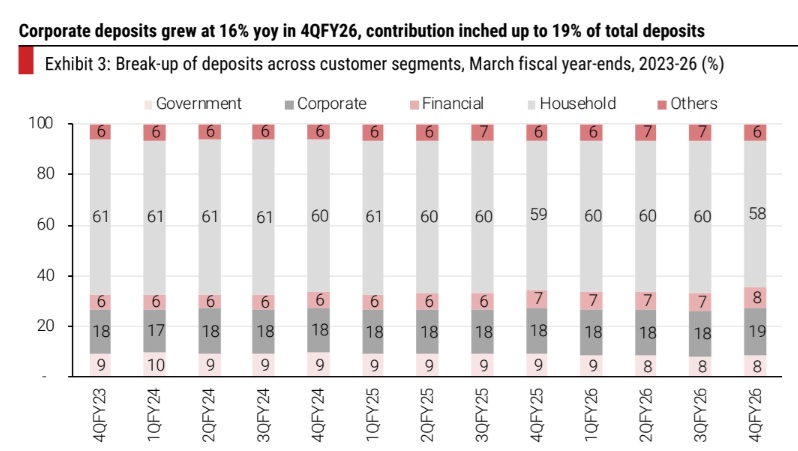

Share of household deposits declined in 4QFY26 primarily on increase in corporate share of deposits; Deposit Growth Trails Loan Demand, Intensifying Competition For Funds; Rising Share Of Non-Operational Bulk Deposits Carries Adverse LCR Implications

FinTech BizNews Service

Mumbai, 5 June 2026: The latest Kotak Institutional Equities report on Banks provide useful insights.

Corporate deposits lead growth, retail remains modest

Deposit growth remained steady (11% yoy) in 4QFY26, led by private banks (13% versus public banks’ 10%). Corporate and financial deposits drove growth (16% and 27% yoy). CASA and term deposits showed modest recovery. However, rising reliance on bulk deposits and repricing pressures signal tighter funding conditions. The NIM outlook is constrained by deposit competition (improving granular deposit) and rate cycle.

Corporate and financial deposits grow strong, driven by private banks

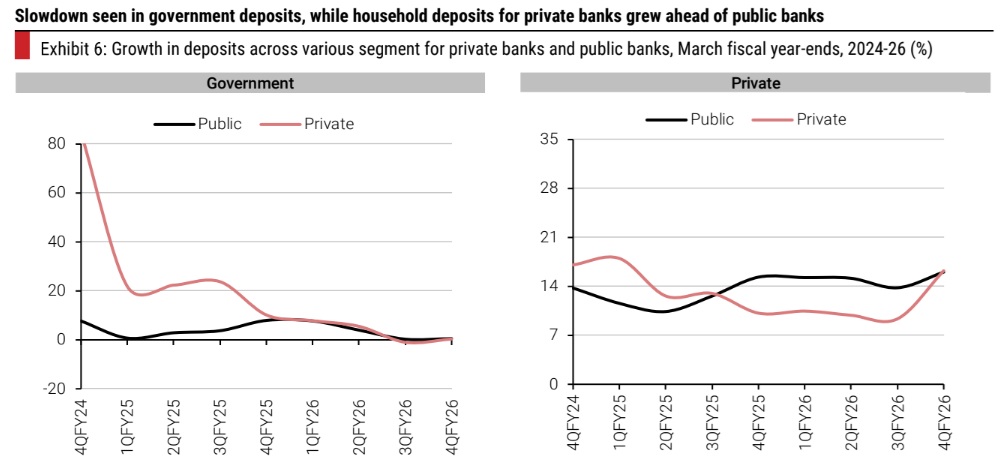

4QFY26 saw 50 bps qoq decline in deposit market share for public banks, with their share now at 60:40. Deposit growth for the sector was at 11% yoy, with private banks (at 13% yoy) ahead of PSU banks (at 10% yoy). The share of household deposits declined by 200 bps qoq to 58% as corporate deposits posted strong growth of 16% yoy, with their contribution at 20%. Growth across depositor segments was mixed, with sluggish government balances, while corporate and financial deposits grew strongly at 16% yoy and 27% yoy, and household deposits posted a steady growth of 10% yoy. Household deposits grew higher for private banks at 12% yoy, compared to PSU banks at 9% yoy. Larger shares of growth in private deposits have been garnered by private banks. The deposit growth in metro, semi-urban and rural areas, is showing signs of recovery. Shares of individual and non-individual reflected higher growth of non-individual deposits, driven by higher growth in corporate deposits.

Key trends in term deposits and CASA deposits

Savings and term deposit growth showed signs of recovery at 10% yoy and 12% yoy, respectively. CASA and term deposits had similar drivers of growth as corporate and financial deposits increased, while the share of households declined. 80% of term deposits mobilized are from metro and urban markets, within which individual term deposits have 70% contribution from the same regions, with share of semi-urban inching up. The significant shares of term deposits have repriced, with individual deposits showing similar trends. However, non-individual term deposits, with two-thirds of 5-6%, were repriced 100 bps higher qoq as competition for deposits intensifies and banks have resorted to bulk deposit mobilization.

NIM outlook is skewed on deposit growth and rate cycle

The tailwind from deposit repricing is largely behind, and the focus shifts to navigating a plausible shallow rate hike cycle amid global headwinds and cost-push inflation. Lenders that rely heavily on EBLR are in a better position because they can reprice their asset sides to support near-term margins, but the main issue is still on the liability side, where deposit growth continues to trail loan demand and intensifying competition for funds. The tilt toward wholesale and non-individual deposits to bridge this gap addressed near-term funding needs, but a rising share of non-operational bulk deposits carries adverse LCR implications. Sustaining margin gains will ultimately hinge on growing the retail deposit franchise without conceding meaningfully on the cost of funds.