The rapid return of depreciation pressures points to the need for more sustained policy support in periods of heightened global uncertainty

Mumbai, 31 May 2026:

FinTech BizNews Service: The State Bank of India’s Economic Research Department has come out with a research report , with focus on the upcoming MPC Meeting on June 3-5, 2026. The special report has been authored by Dr. Soumya Kanti Ghosh, Group Chief Economic Adviser, State Bank of India.

Smouldering ruins of West Asia conflict, in consonance with Second and Third order impacts and an indecisive currency need counter cultural measures and intent reinforcing the ‘Whatever It Takes’ credo for all stakeholders.

June Policy Meet.....RBI to maintain Status Quo against volatile backdrop..

❑ Going by the Growth-inflation spiral, we expect CPI trajectory (as of now) may indicate more than 5.0% inflation for the next 3 quarters (current quarter at ~4.0 to 4.1%)....FY27 projections currently at 5% with risks tilted to upside though well under RBI’s target range

❑ We expect Q4FY26 real GDP growth of closer to 7.2% and FY26 GDP growth is likely to be at 7.5%... Our nowcasted full year FY2027 GDP growth rate of 6.6%, however, with the continued geopolitical uncertainties, the numbers will be revised as more data comes in ... Our call is along ‘Hold the rates’ with a data driven future dependency.. However, an inflation targeting central bank can always use interest rate tools like operation twist that addresses market microstructure

❑ Despite strong macro fundamentals Rupee is depreciating much more vis-à-vis other currencies. Therefore, there is a need for augmented intervention by the RBI.... Also, India‘s FX reserves are optimally sufficient to combat the unidirectional slide of rupee, while aiming to curb excess/undesired volatility concomitantly as the prime aim...There is a clear felt need for a comprehensive BOP package!

❑ In FY2027 so far, SCBs credit continued to grow at 16.2% as of 15 May 2026 and we expect, will remain robust during the H1FY27 and will decline in H2 with high base effect. The full year, credit growth is expected at 13-14% in FY2027

❑ With no trust woven in ongoing ‘peace’ talks in West Asia, the risk premium can remain detached from the underlying going forward, taking a toll on Crude prices that could be trading above ~90 for major parts of the CY26.. Mathematically, excise duty on diesel and petrol need to be reduced by ~Rs 5 to cover the OMC loss completely from the current levels, otherwise domestic fuel prices need to be further increased by Rs 6 from current levels

Global economic growth to slow in 2026, Outlook is clouded

❑ IMF in its latest WEO has revised downward world growth forecast by 20 bps to 3.1% for 2026 and 3.2% for 2027, driven by escalating Middle East conflicts causing supply chain disruptions

❑ Contrary to the global trend, the IMF slightly increased India's growth projection to 6.5% for 2026-27, driven by strong domestic demand

❑ Latest update may swing the projections further as the West Asia conflict stretches endlessly with little trust in sustainable moats of peace being touted by both parties

Global Financial Stability resilient but risks ahead

Equities Sold Off amid the Conflict in the Middle East Bond Yields React More to Bond Auctions. K-Shaped Emerging Market Net Capital Flows Favoring Bonds (Not Foreign Direct Investment or Equities)

Global equity prices have declined by 8% since Feb Sharp rise in global sovereign bond yields

Capital flows heavily skewed towards debt inflows and carry trades rather than more stable foreign direct investment

Crude Oil May Remain ~$95 per barrel in 2026 as per IEA..

❑ As per US EIA, Iraq, Saudi Arabia, Kuwait, the UAE, Qatar, and Bahrain collectively shut in 10.5 million barrels per day (b/d) of crude oil production in April 2026

❑ Subsequently, (a) the Brent crude oil spot price averaged $117 per barrel (b) in April, $46/b higher than the average in February. This monthly average price is also the highest since June 2022, following Russia’s invasion of Ukraine

❑ EIA estimate that global oil inventories will fall by an average of 8.5 million b/d in Q2 2026, pushing Brent crude oil prices to an average of around $106/b in May and June

❑ Once the traffic through the Strait of Hormuz gradually begins to resume in June and shut-in oil production gradually returns, EIA assume oil prices will begin to fall, decreasing to an average of $89/b by Q4 2026 as global oil inventory withdrawals lessen

❑ EIA assess that most shut-in oil production will be fully restored by January 2027 and that global oil inventories will again start building, helping oil prices gradually lower to an average of $79/b in 2027

The Many Pitfalls of Rs Depreciation

The Role Central Bank needs to Play: MPC needs to debate the role of exchange rate as a policy anchor beyond its mandate of pure inflation targeting

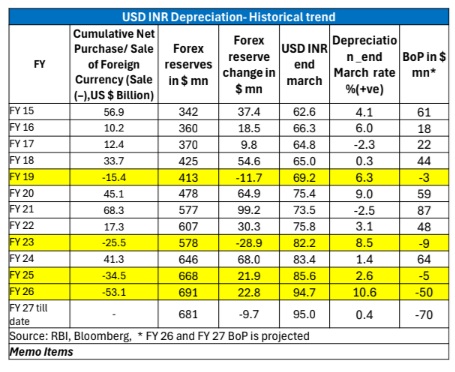

Rupee depreciation till date has been reckless

❑ Rupee has witnessed plethora of crises, but this time is really different (or difficult)

❑ The speed of rupee depreciation has been reckless, and rupee took only 152 days to depreciate by Rs 5 per dollar (from Rs 90 to Rs 95). The Rupee reached 96.83 against USD on 20th May’26

Dent on FX Reserves

Cumulative decline in FX reserves at $47 bn since 27 Feb’26 ($15 bn in last 15 days) Though India still has sufficient FX reserves (~$680 billion)

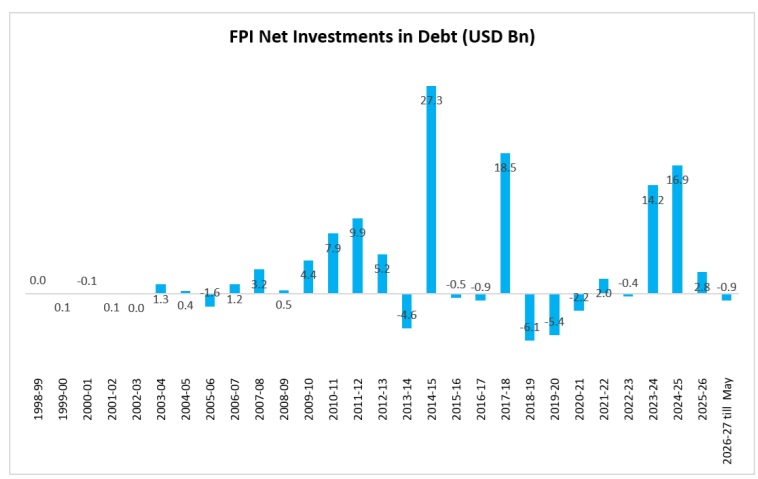

Highest FII outflow since 1991

❑ India has seen significant FII equity outflows since the outbreak of West Asia war, building upon the earlier exodus. Net Equity outflows amounted to $22.7 bn from India (from the onset of war)

❑ Among its peers, only South Korea witnessed higher net equity outflows (but, in the 4 quarters before that, FPIs had poured in $52 bn in local markets, fueling a rally that helped them book substantial profits at higher index levels). Brazil has even registered net equity inflows during the period

❑ FY27 YTD outflow is at $10.6 bn

RBI’s interventions and the fleeting strength of Rupee...

❑ We believe RBI’s wholehearted/ large-scale intervention ideally helps Rupee to stabilize. For instance, on 22nd May RBI’s strong intervention helped Rupee to appreciate and close at Rs 95.69 while the Rupee opened at Rs 95.34 the following day. Similar pattern were observed on 2nd April as well as 16th March’26.

❑ However, in contrast, RBI’s mild intervention may have resulted in rupee opening on a weaker note. For example, on 25th March, RBI’s somehow mild intervention helped Rupee close in below the threshold level of 93 but the next day it immediately breached the 94 mark

❑ Thus the rapid return of depreciation pressures points to the need for more sustained policy support in periods of heightened global uncertainty

❑ As in the past, as a part of conscious strategy, RBI can always intervene in at unstipulated times taking the market by complete surprise. This has happened in the past and can continue to be a toolkit of RBI broader intervention strategy....

On May 24th , US President said that the agreement with Iran is “largely negotiated” which included opening of Hormuz strait thereby helping Rupee to open at an appreciating note on 25th May

RBI’s intervention to arrest the falling Rupee might have been inadequate

❑ The present Rupee depreciation is indeed higher when seen against India’s macroeconomic fundamentals and clearly when compared with other currencies against the $ strength

❑ India‘s FX reserves are optimally sufficient to combat the unidirectional slide of rupee, and it can be used strategically to arrest the downward vortex through strategically timed interventions while aiming to curb excess/undesired volatility concomitantly as the prime aim

❑ There is a need for a comprehensive BOP package! The comprehensive BOP package can comprise of capital controls, liquidity modulation and nudging

Can an inflation targeting central bank also use rates to defend currency?

❑ Ideally NO!! But in the current unprecedented situation, the RBI must take measures to defend the Rupee especially in a situation like this when domestic macro fundamentals are strong

❑ ....So should there be repo rate hike? NO! The RBI must use short term rates and nudging to manage the pressure on Rupee

❑ In Jul’2013, to address exchange rate volatility, RBI had hiked MSF by 200 bps to 10.25% and recalibrated the

corridor 300 bps above the policy repo rate of 7.25%, while keeping reverse repo rate unchanged at 6.25%

❑ Empirical studies indicate that the wider the corridor, the greater the interbank turnover, the leaner the central

bank’s balance sheet (i.e. the lower the average recourse to standing facilities) and the greater short-term interest rate volatility.. The RBI could use measures like operation twist where short term rates could rise at the expense of long-term rates

❑ For instance, Bank of Indonesia has recently hiked the rates even though it is an inflation targeting regime just to defend Indonesian Rupiah.

Liquidity should be modulated; RBI should focus on correcting market microstructure through measures like operation twist

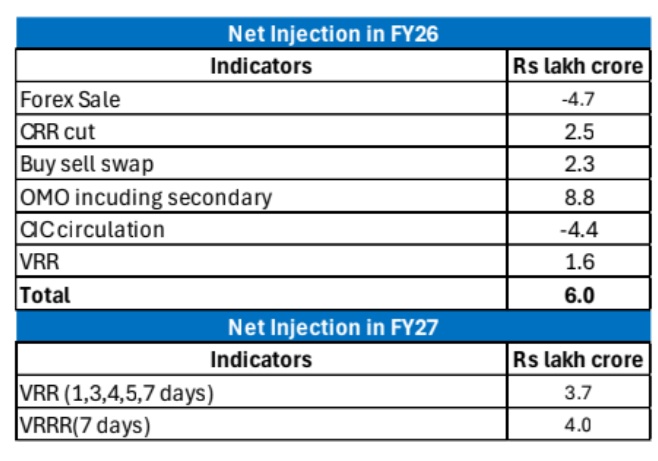

❑ Banking system liquidity surplus narrowed sharply to nearly Rs 0.6 lakh crore from around Rs 3 lakh crore in April, reflecting tighter funding conditions

❑ Average Government surplus cash balance increased to Rs 1.4 lakh crore in May 26 Vs Rs 0.8 Lakh crore in Apr 26

❑ Average Core liquidity narrowed to Rs 3 lakh crore in May from Rs 4.5 lakh crore in Apr

❑ With RBI dividend transfer of Rs 2.9 Lakh crore, we expect a surplus core liquidity of Rs 3.0 to 4 lakh crore by end Jun 26

RUPEE IS UNDERVALUED !!!

The current Rupee value is not in synchronization with India’s domestic macro fundamentals! The Rupee must therefore appreciate from its current levels to reach it long term fair value implied by REER...We believe rupee has clearly overshot the fair value .........

Need to correct REER & NEER Data

❑ There is a need to revisit NEER & REER data for adequate reflection of Rupee strength, in sync with country’s trade proliferation and FTAs that should anchor higher export numbers post normalization of geopolitical conflicts. NEER declined from 91 (FY25) to 85 (FY26) due to global factors such as capital outflows, and oil-driven external pressures...

❑ Rupee appears to have depreciated more in bilateral USD terms compared to NEER, reflecting that USD/INR movements do not fully reflect broader trade-weighted external value adjustments for now. REER declined more than NEER, indicating stronger real depreciation driven by inflation differentials

Framework: Exchange Rate Overshooting

Comparison of INR vs peers : Indexed to 100

Indian Rupee has depreciated against most of the other currencies, including South African Rand, Malaysian Ringgit, Brazilian Real, Chinese Yuan and Japanese Yen

❑ However, it has appreciated modestly against Thai Baht and Indonesian Rupiah since the outbreak of war(27.02.2026)

❑ This points to a temporary risk-premium / flow-pressure component over and above general dollar strength.

REER Implied rate versus USD/INR level

If the rupee’s REER were to return to a chosen anchor, what USDINR level would be consistent with that, holding relative prices and the currency basket broadly unchanged?

If REER normalizes to 100, USDINR would be around 87.1. If REER normalizes only partially to 95, USDINR would be around 91.7. Therefore, the current spot level is much above the REER-implied anchor, suggesting significant scope for rupee appreciation

Petrol/diesel price hike will add to inflationary pressures

❑ Petrol/diesel price has been increased four times in May by OMCs

to ward off the impact of higher crude prices and reduce their losses

❑ Cumulative price increase in petrol/diesel is Rs 7.40 to Rs 7.50 per litre

❑ The daily loss OMC’s which was Rs 1000 per day earlier has now been reduced to Rs 600 per day after the price hike

❑ Accordingly, the overall annual loss has been estimated as Rs 2393 bn

❑ Thus, so far the price hike has covered around 56% of the estimated annual loss

❑ This hike in fuel price is expected to add 35-40 bps in domestic inflation

❑ Our estimates show that excise duty on diesel and petrol need to be reduced by Rs 5 to cover the OMC loss completely from the current levels

Making imported inflation a cause of worry...CPI FY27 numbers could have an upward bias..

Till Apr’26, imported inflation was benign as impact of high global oil prices had not transferred to Indian consumer through petrol/diesel prices

❑ However, now the prices of petrol/diesel has increased by Rs 7.50 per litre and this along-with incessant rupee depreciation may lead to higher imported inflation in May’26

❑ We expect May’s imported inflation (100 items, weight: 21.84%) will be 7.30% as compared to 6.34% recorded in Apr’26, a monthly jump of almost 100 bps

❑ Consequently, we now expect CPI trajectory (as of now) may indicate more than 5.0% inflation for the next 3 quarters (current quarter at 4.0 to 4.1%).... FY27 projections currently at 5% with risks tilted to upside though well under RBI’s target range

Estimates for Q4FY26 GDP stands at 7.2%.... FY27 numbers indicate 6.6% growth

❑ Though, the Indian economy has maintained strong growth momentum but with the with the continued geopolitical uncertainties, we expect Q4FY26 real GDP growth of closer to 7.2% and FY26 GDP growth is likely to be at 7.5%

❑ Our nowcasted full year FY2027 GDP growth rate of 6.6%, however, with the continued geopolitical uncertainties, the numbers will be revised as more data comes in

Double Whammy of Monsoon 2026: Delayed and Weak !!!

❑ India Meteorological Department (IMD), in its updated LRF (29 May) said that the southwest monsoon seasonal rainfall over the country as a whole is likely to be 90% of the Long Period Average

(LPA) with a model error of ±4%, indicating that below normal rainfall is most likely to occur over the country as a whole during the monsoon season (first time in three years)

❑ Though IMD had forecast a marginally early monsoon onset (26 May + 4 days), its extended range forecast now shows largely dry conditions over Kerala between May 28 and June 4 and only a very marginal improvement during June 4 to June 11

❑ Past trend also indicates that when there is Strong El Nino conditions monsoon generally arrived in June only Monsoon 2026: Spatial Distribution indicates below normal for MOST of the India

❑ The southwest monsoon seasonal rainfall is most likely to be normal over Northeast India (94-106% of LPA) and below normal over Central & South Peninsular India (<94% of LPA) and Northwest India (<92% of LPA)

❑ The southwest monsoon seasonal rainfall over the Monsoon Core Zone (MCZ) consisting of most of the rainfed agriculture areas in the country is most likely to be below normal (<94% of LPA)

❑ This indicates that the major foodgrain producing states are going to receive below normal rainfall this year

Sufficient reservoir storage level

❑ While at present India has sufficient storage at important reservoirs, the situation may alter as the monsoon progresses