MSME CREDIT GROWTH IN FY26 TO CROSS RS 6 LAKH CRORES.... 5.5 TIMES HIGHER THAN CUMULATIVE 16 YEAR AVERAGE..

FinTech BizNews Service

Mumbai, November 29, 2025: The India story appears to take new, bigger and bolder dimensions. All with alluring connotations. With 8.0% real GDP growth in H1 FY26, the overall growth for full fiscal would be approximately 7.6% (Assuming 7.5%-7.7% in Q3 and 7% in Q4); predicts a Research Report of the State Bank of India’s Economic Research Department. The report has been authored by Dr. Soumya Kanti Ghosh, Group Chief Economic Adviser, State Bank of India.

GDP EXPANDS BY 8.2% IN FY26

India’s economy grew 6-quarter high by 8.2% in Q2

FY26 as compared to 5.6% growth recorded in Q2

FY25. The GVA grew by 8.1%.

Nominal GDP grew by 8.7% in Q2 FY26 higher than

the 8.3% growth occurred in Q2 FY25. The gap be-

tween real and nominal GDP, which was as large as

12 percentage points in Q1 FY23, dropped sharply to

0.5 percentage points in Q2 FY26.

Core GVA (Overall GVA ex Agriculture and Public Fi-

nance) registered a growth of 8.5% yoy in Q2 FY26

compared to a lower 5.6% yoy in Q2 FY25.

Agriculture sector grew by 3.5% while industry sector

witnessed a high growth of 7.7% compared to 3.8%

in Q2FY25.

India's manufacturing sector showed impressive

growth in Q2FY26, growing by 9.1% YoY, compared

to a mere growth of 2.2% in Q2FY25.

Services sector shows stellar performance alongside

manufacturing and grew by 9.2% due to 10.2% in

‘Financial, real estate & professional service’ sector’

and 9.7% growth in ‘ trade, hotels, transport, com-

munication, etc.’ sector.

With 8.0% real GDP growth in H1 FY26, the overall

growth for full fiscal would be approximately 7.6%

(Assuming 7.5%-7.7% in Q3 and 7% in Q4)

GDP DEFLATOR

GDP deflator declined to 0.5% yoy in Q2 FY26 com-

pared to 2.5% yoy in Q2 FY25. Growth in GDP defla-

tor for agriculture has declined to -1.7% yoy in Q2

from -0.5% yoy in the previous quarter.

For industry GDP deflator increased to 0.7% yoy

compared to 0.6% yoy in Q2 FY25, with manufactur-

ing registering higher deflator growth.

Meanwhile, growth in services deflator moderated to

1.2% yoy in Q2 from 2.8% yoy in Q2 FY25.

EXPENDITURE SIDE STORY

The Q2 demand is a story anchored in private

consumption that registered a growth of 7.9%,

capital formation registered a growth of 7.3%. The

exports also registered growth of 5.6%, which is a

sequential slowdown but improvement on yoy basis

indicating mixed pictures on external demand.

However, H1 figures show exports held up during

FY26 despite the headwinds. Front loading of exports

against the backdrop of US tariffs supported higher

exports growth.

The expenditure side trends show robust demand

trend supported by two factors. First, a broad

deceleration in prices is reflected in contractionary

trends in GDP deflators and second good

performance in labour intensive sectors such as

agriculture, manufacturing, construction and services

such as personal and financial services. The growth in

change in stock also suggests strong demand trends.

Other components such as valuables have continued

to contract. Valuables contracted by 22.7% yoy owing

to higher base as Q2 FY25 registered sharp growth

owing to high investment demand for gold due to

rising prices. The sharp growth in imports was riven

by capital goods, rare earth and chemicals imports

that were absorbed in capital formation during the

year.

The overall trends suggest that GDP growth is

domestic driven, supported by services exports and

driven by low inflation and value-add expansion in

labour intensive sector.

LINKAGE BETWEEN NOMINAL GDP & EARNINGS

GROWTH

To test the linkage between GDP and earning growth

we have taken nominal GDP YoY Growth and Nifty50

index YoY growth data for the period Q1FY13 to

Q2FY26. Till Q1FY23, both move in the same direc-

tion but there after indicate a divergence in trend.

To test statistically, we have calculated the correla-

tion between GDP and Nift50 Returns. The results

indicate that there is a positive correlation between

both for the period Q1FY13-Q2FY26 and Q1FY21-

Q2FY26. While there is a negative correlation during

the recent period Q1FY23-Q2FY26.

Thus, positive correlation between Nifty returns and

GDP growth, meaning that as the Indian economy's

GDP grows, the Nifty index tends to rise as well. How-

ever, the link is not always perfectly synchronized in

the short term, as market performance is influenced

by many factors beyond GDP, such as investor senti-

ment, corporate earnings, and global economic con-

ditions. In the long term, however, market growth

and earnings tend to converge, suggesting that

strong economic growth can lead to sustained mar-

ket returns.

FLOW OF CREDIT TO COMMERCIAL SECTOR

Indian banking system are now positioned as a sound

and well capitalised sector to support growth. In the

current year, the credit growth of SCBs is slowly pick-

ing up and grew by 11.3% YoY, (last year 11.8%) for

the fortnight ended 31 Oct’2025, while deposits

growth remains at 9.7% (last year: 11.7%).

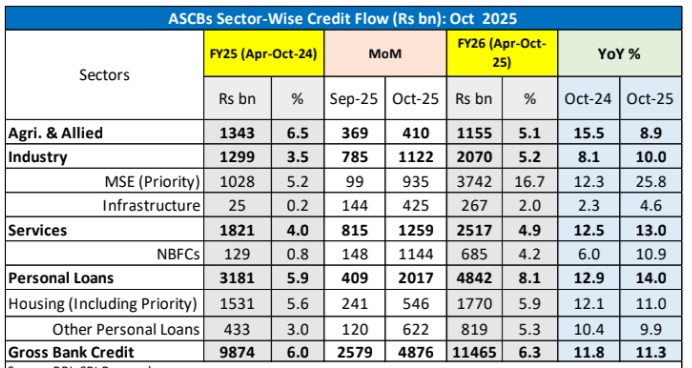

The sector-wise incremental credit growth for Octo-

ber 2025, indicate that credit growth has increased

across the sectors, except Agri & Allied sector. Agri &

Allied sector grew by 8.9% (Last year: 15.5%), indus-

try by 10.0% (Last year: 8.1%), Services by 13.0%

(Last year: 12.5%) and personal loans by 14.0% (Last

year 12.9%).

Credit to ‘Micro and Small’ and ‘Medium’ industries

continued to expand in double-digits. Among major

industries, outstanding credit to ‘all engineering’,

‘infrastructure’, ‘construction’, ‘textiles’ and

‘vehicles, vehicle parts and transport equipment’ rec-

orded buoyant y-o-y growth. Loans against gold jew-

ellery increased by 128.5% YoY to Rs 3.37 lakh crore.

By looking at the trend growth, deposits may grow by

10-11% and credit by 11-12% for SCBs during FY26.

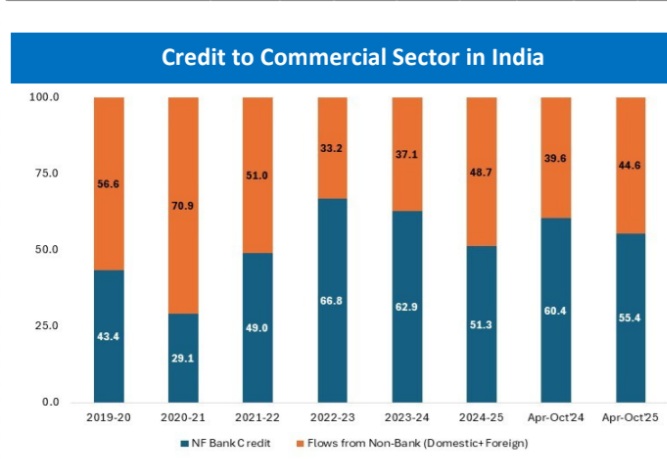

The resource flows to commercial sector indicate

that the share of bank funding hold ~55% during Apr-

Oct’25, compared to 60% in Apr-Oct’24, which is

mainly due to the Rs 2.2 lakh crore flows from

‘Corporate Bonds by Non-Financial Entities’, com-

pared to last year Rs 39,201 crore during Apr-

Oct’2024.

In our earlier estimate, granger causality test results

confirmed that there is one way causal relationship

between GDP and ASCB credit, with increase in credit

leading to higher GDP. So, with the increase in credit

during Q3FY26, amid GST rationalisation, we expect

GDP growth will be 7.5-7.7% and 7.0-7.1% in

Q4FY26.

CORPORATE RESULT Q2FY26 - EBIDTA GREW NEAR

DOUBLE DIGIT, FROM NEGATIVE A YEAR AGO

Around 4000 Corporate in the listed space reported

revenue growth of 6.8% while EBIDTA and profit after

tax (PAT) growth of around 7.7% and 33% respective-

ly in Q2FY26 as compared to Q2FY25.

Further, Corporate ex BFSI represented by more than

3500 listed entities reported revenue and EBIDTA

growth of 6.8% and 9.6% respectively, in Q2FY25 as

compared to -1.5% growth in Q2FY25.

Major sectors that contributed to the growth include

Aerospace and Defence, Automobiles, Capital goods,

Cement, Diamond, Gem and Jewellery, Fertilisers,

Non-Ferro Metals, Steel, etc. Overall EBIDTA margin

also improved by 41 bps i.e. from 14.4% in Q2FY25 to

14.81% in Q2FY26. Q2FY26 result was mainly driven

by strong performance in commodity-oriented sec-

tors and improved consumption supported by tax

and GST rationalisation.

New investment announcements also improved by

around 80% in first half of FY26 to Rs 35.8 trillion

powered by private investment announcements

which contributes more than 70% of the new an-

nouncements. Capacity utilisation remained strong at\

74.1 in June’25 though it moderated from 77.7 in

Mar’25.