FY27 can see working capital loans picking up again

FinTech BizNews Service

Mumbai, March 27, 2026: Credit flows accelerated sharply in FY26, rising 61% YTD to INR 25.1 tn, and coming close to deposit mobilisation of INR 26.1 tn, which grew 21% YTD. While credit demand across retail, MSME and infrastructure have remained firm, fresh deposit mobilization shows a slackening pace since FY24, according to a special research report by Yes Bank's Economic Knowledge Banking.

The slower banking sector deposit growth could have been a consequence of lower net financial savings of the housing sector. The C/D ratio is at 82.4%, its highest since FY15, signaling tighter liquidity. With buffers thinning and the funding gap narrowing, banks have also been relying more on CDs, pushing up funding costs and partially negating the easier monetary policy stance. In absolute terms, incremental credit growth in FY26 is close to incremental deposit growth, leading to a C/D ratio at a decade high of 82.4.

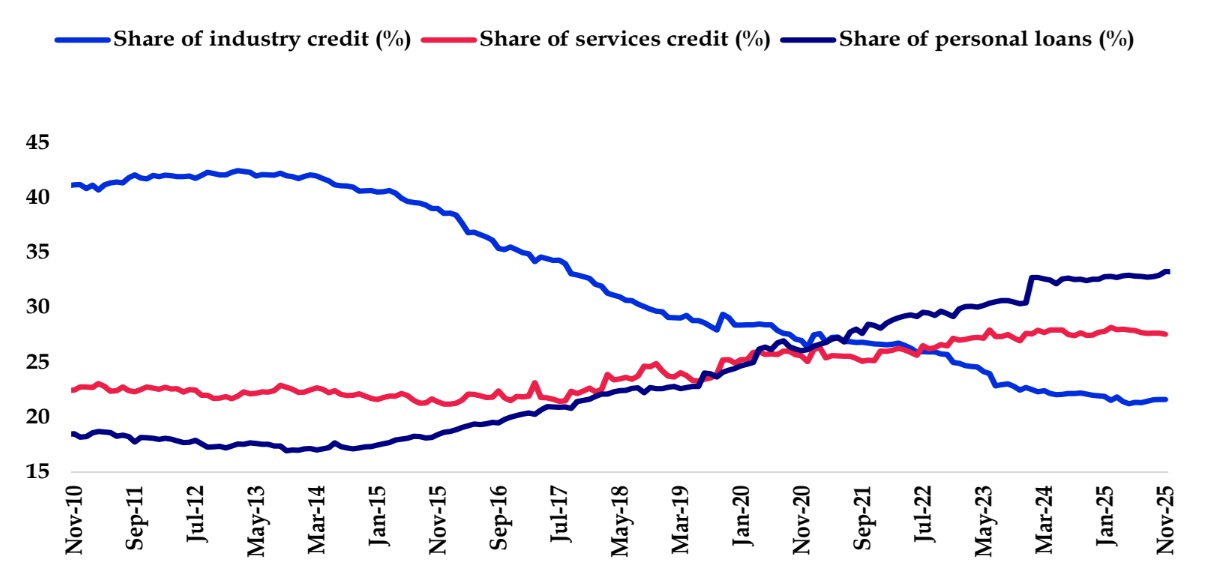

Sectoral deployment data for FY26 shows that credit momentum is led by personal loans, followed by the services sector, with industry credit also firming after a muted FY25. The share of personal loans has risen from 29% to 33% in recent years, supported by GST rationalisation and tax relief that strengthened household income. Within personal loan segment, vehicle loans have overtaken housing loans as the main growth driver since Q3FY26, and both secured and unsecured loans have recovered after a soft H1FY26, with a clear rotation toward secured products as unsecured loan growth moderated. Industry credit has firmed in FY26, led by MSMEs that now comprise almost one-third of industrial credit and continued to be the strongest contributor to industrial loan growth in FY26. Micro and small enterprises added INR 2.38 tn, while medium enterprises added INR 630 bn, supported by Union Budget push towards credit guarantee for the segment and new enhanced definition of MSMEs. Infrastructure lending has picked up with support from government’s capex push, even as construction credit remains subdued amid a slower private-capex recovery. Having said, corporate lending patterns indicate an increase in the growth of the project finance in Q3FY26 while working capital has contracted. This data needs to be watched to figure out if there are tentative signs of private investment demand. However, sustainability of the same may be questionable if the West Asia crisis continues and energy prices remain elevated.

While monetary easing by the RBI, liquidity push and GST rationalization enabled a stronger credit growth in FY26, the outlook for FY27 appears challenging. Domestic growth can weaken due to the West Asia conflict – higher oil prices and lower exports to the region. Domestic growth can weaken due to fading of the GST benefits, while higher food inflation also dent real wages and may dampen discretionary spending. There can be an upside pull for working capital loan from higher inventory costs on account of higher input prices, while a downward pull for working capital may come from lower domestic economic activity. Overall, we expect the credit growth to slow in FY27. On the domestic deposit side, there can be an upside due to lower discretionary spend. If the above materializes, there can be a natural softening of the C/D ratio, that has now moved significantly on the higher side.

FY27 can see working capital loans

picking up again due to higher inventory

costs emerging out of higher global

commodity prices, supply chain

disruptions, etc.

• However, a negative pull can also emerge

due to slowing economic activity due to

the West Asis crisis

• Pull from project finance could also be

lagging as companies may put investment

activities on hold due to expectations of

slowing consumption demand

• Overall, credit growth can weaken from

the current 14%+ pace of FY26